Intel Corporation (INTC) has been one of the market’s biggest turnaround stories in 2026. The stock has surged sharply this year as investors warmed to its foundry ambitions, growing AI exposure, and a broader recovery narrative.

Now, Intel said it will work with Foxconn (FITGF) to develop and deploy next-generation AI infrastructure and intelligent computing platforms, a step that could deepen its role in data centers, edge computing, and emerging AI systems.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

The Intel and Foxconn tie-up spans everything from rack-scale AI hardware to cooling, interconnects, and custom silicon. For Intel, the deal suggests a broader push to stay relevant in high-growth AI markets while expanding beyond its traditional chip business.

The key question now is whether Intel can turn this partnership into a meaningful growth engine and strengthen its competitive position in the AI race.

INTC Stock Has Had a Monster Year

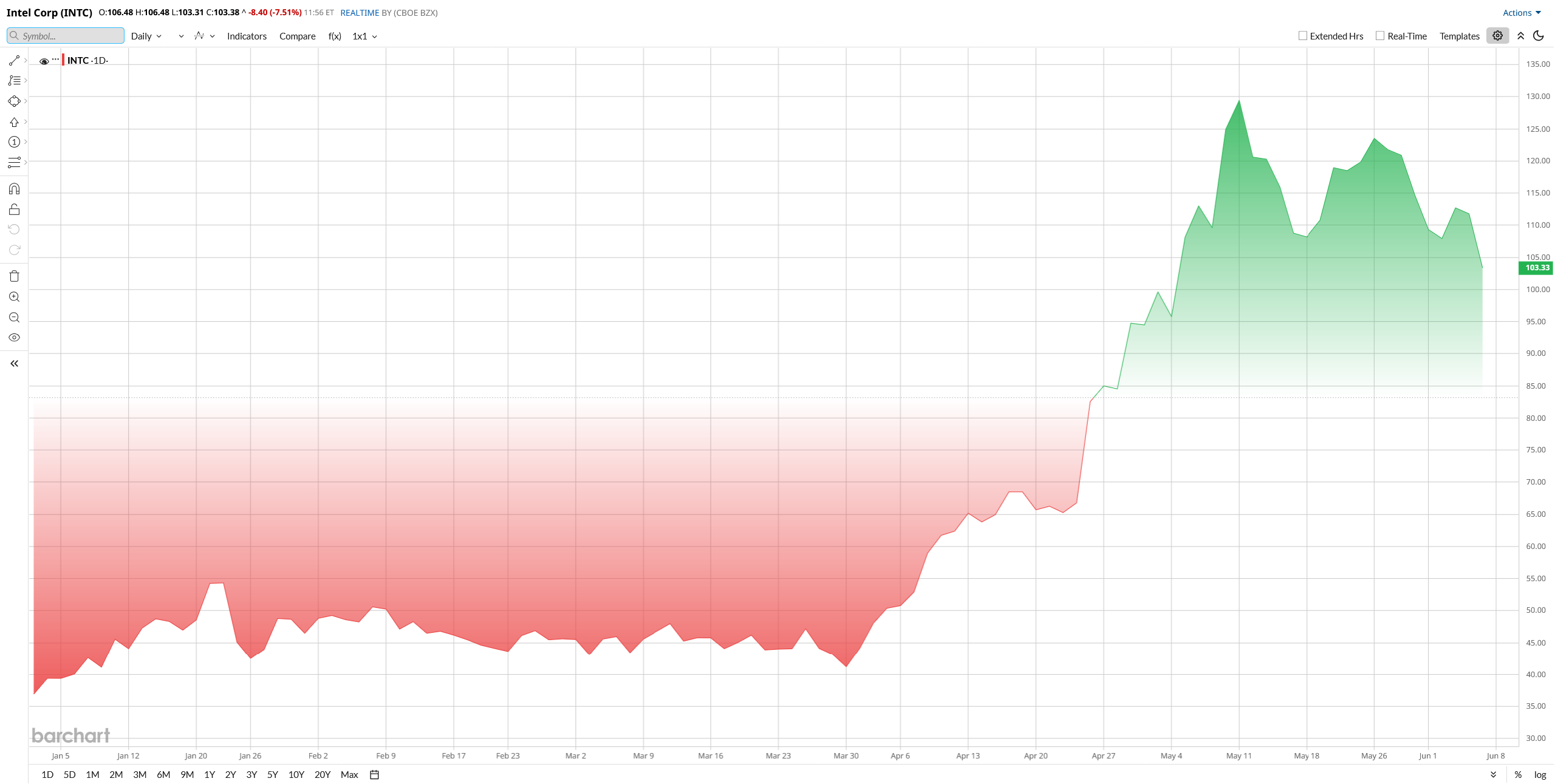

Despite a slip of about 8% in morning trading today, Intel shares have ripped higher this year, more than tripling year-to-date (YTD) in 2026 and roughly 420% over the past 12 months. The stock has climbed to around $103, well above its 50-day moving average of $95 and its 200-day moving average of $72. That kind of technical setup signals strong momentum, but it also shows how much good news is already baked into the share price.

A lot of the rally has come from the market buying into Intel’s turnaround. Investors have increasingly focused on its foundry push, hopes for a more competitive AI chip strategy, and the idea that geopolitical tensions could support domestic chip manufacturing in the U.S.

The Foxconn deal only added to that narrative. Intel said it will work with Foxconn on custom AI inference chips, which matters because Foxconn is deeply embedded in server manufacturing for major AI players. That gives Intel a potential path deeper into the data center supply chain.

Intel’s Valuation Looks Stretched

The problem is valuation. Intel is no longer priced like a struggling chipmaker. It is priced like a company that must execute almost perfectly from here.

The stock trades at about 105 times forward earnings, compared with a sector median of around 28 times. Its price-to-sales ratio is about 9 times, versus roughly 5 times for the sector. Those are rich numbers for a company that is still in the middle of a costly turnaround.

That does not mean Intel cannot keep climbing. It can. But the current valuation leaves very little room for disappointment. Investors are paying up for future earnings growth that still has to show up in a meaningful way.

www.barchart.com

www.barchart.com Latest Quarterly Results Show Progress, but Also Pain

Intel’s Q1 earnings gave investors a mixed picture. Revenue came in at $13.58 billion, up 7% from a year earlier. That is not explosive growth, but it does show the business is stabilizing. The strongest part of the report was the Data Center and AI segment, which rose 22% year-over-year (YoY) to $5.1 billion. That marked the sixth straight quarter of beating expectations in that business.

Still, the bottom line was ugly. Intel posted a net loss of $2.8 billion, pressured by more than $4 billion in restructuring charges. On a non-GAAP basis, the company reported adjusted earnings of 29 cents per share.

Free cash flow was negative $2 billion, as Intel continued pouring money into factories and manufacturing expansion. That is not surprising, but it does matter. The company ended the quarter with $32.8 billion in cash and equivalents, which gives it some breathing room, though not unlimited flexibility.

Management also guided for second-quarter revenue of $12.8 billion to $13.2 billion. For the full year, analysts are looking for revenue between $58 billion and $65 billion, with earnings per share around $1.09. That forecast helps explain why the stock is trading at such a steep multiple. The market is looking ahead, not backward.

Intel Is Doing More Than Just the Foxconn Deal

The Foxconn announcement is not happening in a vacuum. Intel has been stacking up other strategic wins in 2026.

The company expanded its partnership with Alphabet's (GOOG) (GOOGL) Google on custom ASIC chips, another sign that Intel is trying to carve out a real role in specialized AI hardware. Nvidia (NVDA) also chose Intel’s Xeon 6 processors for its Rubin AI systems, which gave Intel an important credibility boost in the data center market.

There is also growing speculation around Intel’s foundry platform. Tesla (TSLA) has reportedly shown interest in Intel’s 14A process for its Terafab project, although no formal deal has been announced. Even so, the fact that Intel keeps getting mentioned in major AI and manufacturing conversations suggests the company is becoming relevant again in places where it had been left behind.

That is the real story here. Intel is not just trying to sell more chips. It is trying to prove that it belongs in the next generation of AI infrastructure, both as a designer and a manufacturer.

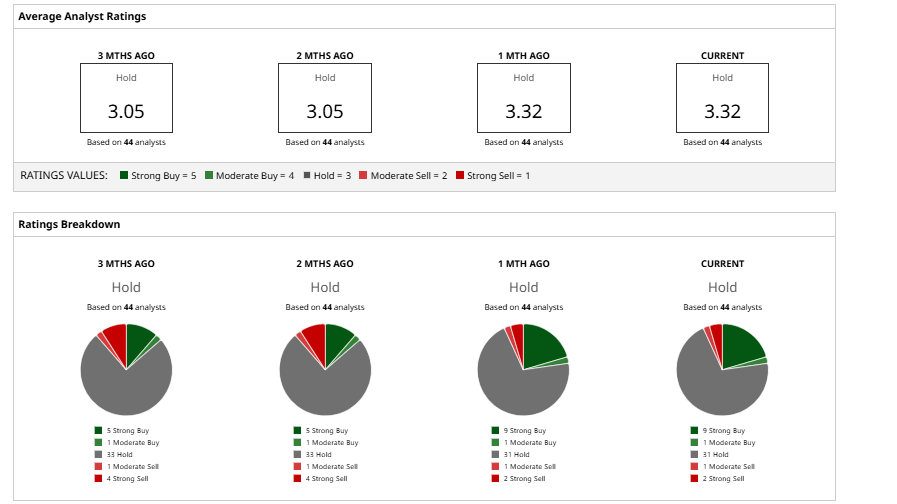

What Do Analysts Think of INTC Stock

Wall Street is still split on Intel, and that makes sense given how much of the turnaround story is already priced into the stock.

Morgan Stanley kept an “Equal Weight” rating and a $73 price target, saying the Foxconn partnership is a positive step but does not fully address Intel's long-term foundry profitability challenge. Bank of America is more cautious, carrying an “Underperform” rating and a $56 target, arguing that competitive pressure could weigh on Intel's consumer business.

UBS remains “Neutral” with a $65 target, saying INTC stock's recent run has outpaced the company's underlying fundamentals. So while analysts see progress in Intel's manufacturing and AI efforts, there is still plenty of debate about how much upside remains from here.

According to Barchart data, INTC stock's consensus stands at “Hold,” with an average price target of about $90.58. That implies modest downside from current levels.

The bottom line is that Intel is making smart moves, and the Foxconn partnership could matter. But the stock has already run far enough that investors now need proof, not just hope.

www.barchart.com

www.barchart.com On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Dear Micron Stock Fans, Mark Your Calendars for June 24 TTM Technologies Stock Is Up 450% in a Year and Could Still Run Higher Intel Just Landed a Major Foxconn AI Win. INTC Stock Needs Proof, Not Hope, to Climb Further. CELH Stock Alert: What to Know as Celsius Faces Child Safety Investigation