The artificial intelligence (AI) infrastructure trade has shifted from pure-play semiconductors to other AI-powered data center infrastructures. This includes AI-powered memory and storage devices as well as servers and racks, photonics and optical network manufacturers, electrical grid equipment, advanced cooling systems, and specialized semiconductor packaging to name a few.

Moreover, agentic AI is expanding the scope of AI infrastructure providers in the physical layer across industries. As a result, the generative AI-based graphical processing unit (GPU) developer NVIDIA Corp. NVDA, which was the poster boy of AI trade in the past four years, lost some of its charm in 2026.

Instead, investor’s focus has shifted to those companies that develops the above-mentioned AI-powered data center infrastructure products. Here, we recommend two such stocks that have skyrocketed this year with more than 200% returns. Yet, their solid outlook and current Zacks top rank indicate more firepower in the future.

The companies are: Micron Technology Inc. MU and Dell Technologies Inc. DELL. Each of our picks currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The chart below shows the price performance of the three stocks mentioned above year to date.

Image Source: Zacks Investment Research

Micron Technology Inc.

Micron has been benefiting tremendously from the enormous application of AI in day-to-day life, which has pushed up the demand for memory chips. The four major hyperscalers raised their AI capital expenditure budget to $750 billion for 2026. This figure is set to cross $1 trillion next year and is likely to rise further beyond 2027.

This has resulted in more AI semiconductor sales implying the need for multiple AI memory chips to operate. Flash memory technologies like DRAM and NAND are used in AI chips, enabling them to perform optimally.

This has pushed up the demand for AI-enabled memory chips. In their last earnings reports, all four major hyperscalers highlighted a shortage of memory and storage chips, resulting in soaring prices of these products. As a result, MU benefits significantly.

New Tech Trends to Drive MU’s Prospects

Micron has meaningful exposure to AI, cloud data centers, industrial IoT and autonomous vehicles, all of which require increasingly advanced memory solutions. As AI adoption accelerates, demand for DRAM and NAND products continues to rise.

MU has invested heavily in next-generation memory technologies, positioning itself to meet the growing performance and efficiency requirements of AI systems. A particularly important growth driver is high-bandwidth memory (“HBM”), which has become essential for advanced AI workloads. Micron Technology’s HBM3E and HBM4 products are seeing exceptionally strong demand because they offer the speed and efficiency required by modern AI systems.

MU’s position in the AI ecosystem continues to strengthen. NVIDIA identified Micron as a key HBM supplier for its GeForce RTX 50 Blackwell GPUs, reinforcing its importance within the AI supply chain. Demand for HBM4 is also benefiting from next-generation AI infrastructure deployments, including NVIDIA’s Vera Rubin platform.

Strong Guidance

Micron anticipates revenues of $35.5 billion (+/-$750 million) in the fiscal third quarter of 2026. MU projects a non-GAAP gross margin of approximately 81%. Operating expenses on a non-GAAP basis are estimated to be approximately $1.4 billion. Adjusted EPS is anticipated to be $19.15 (+/- 40 cents).

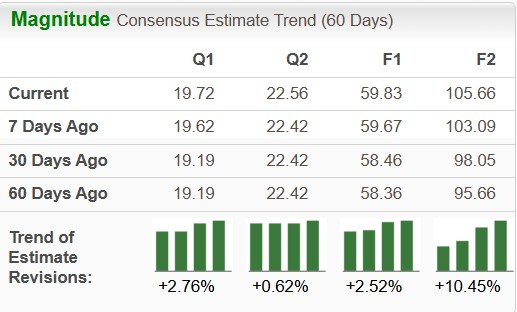

Solid Estimate Revisions & Attractive Valuation

Micron Technology has an expected revenue and earnings growth rate of more than 100% each, for the current year (ending August 2026). The Zacks Consensus Estimate for the current year’s earnings has improved 0.3% over the last seven days.

Despite a robust rally, the MU stock still looks attractive. It trades at a forward 12-month price-to-earnings (P/E) multiple of 15.87, which is significantly lower than the industry average of 27.05. This discount adds to the appeal for long-term investors.

Image Source: Zacks Investment Research

Dell Technologies Inc.

Dell reported blockbuster results for the first quarter of fiscal 2027 primarily driven by a stunning 757% increase in server sales powered by AI chips. In May 2026, FORTUNE BUSINESS INSIGHTS estimated that “the global AI server market size was valued at $194.62 billion in 2025.

The market is projected to grow from $262.22 billion in 2026 to $2,847.32 billion by 2034, exhibiting a CAGR of 34.73% during the forecast period.” The astonishing growth potential of the global AI-optimized server market is noteworthy.

Innovative Products

Dell Technologies is benefiting from strong demand for AI-optimized servers driven by the ongoing digital transformation and heightened interest in generative AI applications. Its PowerEdge XE9680 AI-optimized server is much in demand.

DELL’s advanced AI-optimized servers including the PowerEdge XE9780 and 9780L platforms supporting up to 256 NVIDIA HGX B300 GPUs per rack, the XE9712 with NVIDIA GB300 NVL72, and the XE7745 supporting NVIDIA RTX Pro 6000 Blackwell GPUs, are noteworthy.

In fiscal fourth-quarter 2026, DELL launched the PowerEdge XE9712 supporting NVIDIA's NVL72 GB200. It launched the Dell Infrastructure Rack Sobel system, IR7000 and 5000 in both 21-inch and 19-inch versions, providing up to 96 GPUs in a rack and 786 GPUs in a scalable unit. The strong demand trend bodes well for the company’s long-term prospects.

Strong Guidance

For the second quarter of fiscal 2027, DELL expects revenues between $44 billion and $45 billion, with non-GAAP earnings of $4.80 (plus or minus 10 cents). For fiscal 2027, Dell Technologies expects revenues between $165 billion and $169 billion and guided to non-GAAP earnings of $17.90 per share (+/- 25 cents).

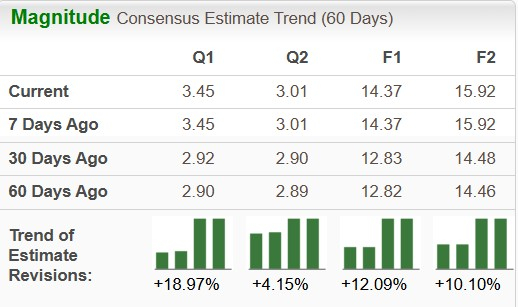

Solid Estimate Revisions & Reasonable Valuation

Dell Technology has an expected revenue and earnings growth rate of 47.4% and 39.5%, for the current year (ending January 2027). The Zacks Consensus Estimate for the current year’s earnings has improved 12% over the last 30 days.

Despite a robust rally, the DELL stock still looks reasonably priced. It trades at a forward 12-month price-to-earnings (P/E) multiple of 27.90, in line with the industry average.

Image Source: Zacks Investment Research

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Dell Technologies Inc. (DELL): Free Stock Analysis Report

Micron Technology, Inc. (MU): Free Stock Analysis Report

NVIDIA Corporation (NVDA): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).