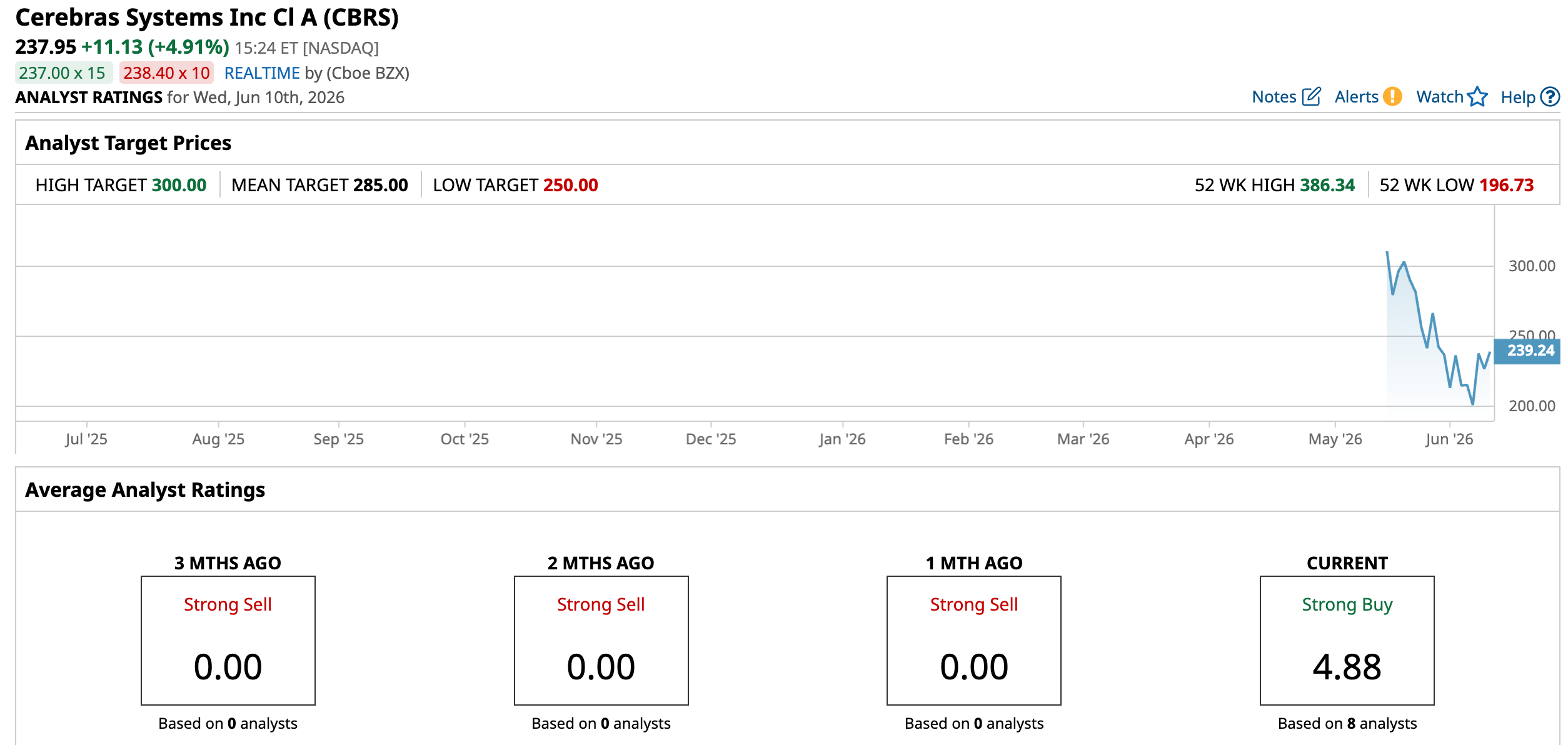

Cerebras Systems (CBRS) has barely been public for a few weeks, but Wall Street is already starting to place some big bets on its future. Shares of the AI chipmaker surged more than 18.3% this Monday after its post-IPO quiet period expired, unleashing a wave of analyst coverage. Several prominent brokerage firms initiated coverage with bullish ratings, arguing that Cerebras could emerge as one of the most serious challengers to Nvidia (NVDA) in the rapidly expanding AI infrastructure market.

Among them Mizuho believes the ‘fast-inference’ segment – the fastest-growing segment in which Cerebras leads – could grow into a $550 billion annual recurring revenue opportunity by 2030. That projection matters because fast inference is exactly where Cerebras has built its competitive edge. A proprietary hardware and software stack anchored by the Wafer Scale Engine with massive on-die SRAM creates a strong moat.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

With Wall Street forecasting massive growth in fast inference, and major partnerships already helping drive adoption, Cerebras finds itself at the center of one of the most promising corners of the artificial intelligence market. So, is this $550 billion opportunity a reason to buy CRBS stock today?

About Cerebras Stock

Founded in 2015 and based in Sunnyvale, California, Cerebras Systems is one of the newest players trying to reshape the AI hardware market. The company is best known for its Wafer-Scale Engine (WSE), a massive chip built from an entire silicon wafer, designed to run AI models faster and more efficiently than traditional processors.

Its CS-2 and CS-3 systems help power AI training and inference for cloud providers, research labs, enterprises, and government-backed AI projects. With operations spanning multiple regions and a market cap of $48.79 billion, Cerebras is emerging as a notable challenger in the fast-growing AI infrastructure race.

CBRS stock price trajectory since its IPO has been anything but boring. The AI chipmaker became public in May amid enormous enthusiasm for anything tied to AI, and investors were eager to get a piece of the story. That excitement was evident even before trading began. While Cerebras initially expected to price its IPO between $115 and $125 per share, demand proved far stronger than anticipated. The company ultimately sold 34.5 million shares, including the underwriters' option, at $185 each.

Once trading opened on May 14, investors piled in. CBRS stock surged nearly 68% on its debut, closing at $311.07 after reaching an intraday high of $386.34. For a brief moment, Cerebras became one of Wall Street's hottest AI trades.

But as often happens with high-profile IPOs, the initial euphoria eventually cooled. Over the following weeks, shares pulled back as investors digested the company’s valuation and broader sentiment across the AI sector became more measured. The stock gradually retreated toward the low-$200 range, where buyers began stepping back in.

More recently, sentiment has improved. Following the expiration of the company's post-IPO quiet period, a wave of bullish analyst initiations helped reignite investor interest. As Wall Street grows more optimistic about Cerebras’ fast-inference opportunity, shares have rebounded by the mid teens from recent lows.

www.barchart.com

www.barchart.com Cerebras’ Revenue Growth Is Starting to Match the Excitement

Cerebras’ wafer-scale AI chips garnered significant attention, but last financial numbers suggest the company can turn innovation into real business growth. According to its amended S-1 filing, Cerebras reported $510 million in revenue for 2025, up 76% year-over-year (YOY). Even more impressive, the company swung from a net loss of $481.6 million in 2024 to a net profit of $237.8 million in 2025. In a sector where many AI companies are still spending heavily and posting losses, that combination of strong growth and profitability stands out.

And the runway ahead looks substantial. As of December 2025, Cerebras reported remaining performance obligations (RPO) of $24.6 billion, essentially a backlog of contracted business waiting to be recognized as revenue. The company expects about 15% of that amount, or roughly $3.7 billion, to be recognized by the end of 2027. That’s before factoring in any new customers or future deals.

Cerebras also has the resources to pursue its growth plans. After accounting for IPO proceeds, the company reported a pro forma cash balance of approximately $5.7 billion, giving it plenty of flexibility to invest in infrastructure, expand capacity, and continue developing new products.

Its customer list adds another layer of confidence. Alongside OpenAI, Cerebras counts G42 and MBZUAI among its clients. And, the company has secured a partnership with Amazon that will bring Cerebras systems into AWS data centers, expanding its reach across the AI ecosystem.

The broader market opportunity remains massive. Dell'Oro Group expects data center infrastructure spending to reach $1.7 trillion by 2030. With its CS-3 systems gaining traction and a growing intellectual-property portfolio that includes 96 issued patents and 50 pending applications, Cerebras appears well-positioned to capture a meaningful share of the AI spending wave over the coming years.

Investors won’t have to wait long for the next quarterly update. Cerebras is scheduled to report first-quarter 2026 results on Tuesday, June 23 after the closing bell. Analysts tracking the company expect a loss of $0.14 per share for the quarter, with revenues coming in at around $180.8 million. While the company is still in growth mode, analysts are forecasting a loss of $1.20 per share for fiscal 2026 before a potential swing to profitability in 2027, with EPS projected to reach $0.88.

Mizuho Sees Massive Opportunities

For years, the AI race was all about building bigger and smarter models. Now, the focus is shifting to how quickly those models can deliver answers. Whether it is a chatbot responding to a customer, an AI agent completing a task, or an enterprise application processing data, speed is becoming a competitive advantage.

That is why Mizuho analyst Vijay Rakesh believes Cerebras could be sitting in a sweet spot. The brokerage firm recently launched coverage on the AI chipmaker with an “Outperform” rating and a $300 price target, arguing that the company is aligned with some of the most powerful trends and fastest-growing segments of AI – inference, which is the process of running trained AI models in real-world applications.

Mizuho expects AI spending to soar to roughly $2.8 trillion by 2030, expanding at a CAGR of 36%, as companies continue pouring money into AI infrastructure. But within that massive market, the firm sees “fast inference” as the standout opportunity. It projects the segment could grow into a roughly $550 billion market by the end of the decade, expanding at a CAGR of 291%.

Cerebras’ technology was built around solving the speed problem. Its Wafer Scale Engine and software stack are designed to deliver responses faster and more efficiently than traditional architectures. As demand for real-time AI applications accelerates, Mizuho believes that advantage could help fuel explosive revenue growth for Cerebras in the years ahead.

Are Other Analysts Bullish on Cerebras Stock?

Mizuho is far from the only brokerage firm that sees big potential in Cerebras. In fact, since the company’s post-IPO quiet period expired, analysts have lined up with a remarkably bullish view of the AI chipmaker's prospects. The most optimistic voice so far has come from Citi analyst Atif Malik, who initiated coverage with a “Buy” rating and a price target of $340.

Meanwhile, Morgan Stanley's Joseph Moore also came away impressed, describing Cerebras as a rare opportunity for investors to gain exposure to an AI processor company with a first-mover advantage against NVIDIA in certain segments of the market. Moore initiated coverage with an “Overweight” rating and a $250 price target.

Rosenblatt Securities focused on the company’s rapidly growing business momentum. The brokerage firm pointed to Cerebras’ partnerships with OpenAI and AWS as key catalysts, noting that annual revenue climbed from just $25 million in 2022 to roughly $510 million in 2025. With revenue projected to reach $6.8 billion by 2028, analyst Kevin Cassidy initiated with a “Buy” rating and a $300 target.

UBS analyst Timothy Arcuri echoed that optimism, calling Cerebras a pure-play fast inference company with a growing backlog. He believes the company’s Wafer Scale Engine gives it a meaningful performance advantage in select premium AI workloads, supporting UBS’ “Buy” rating and $300 price target.

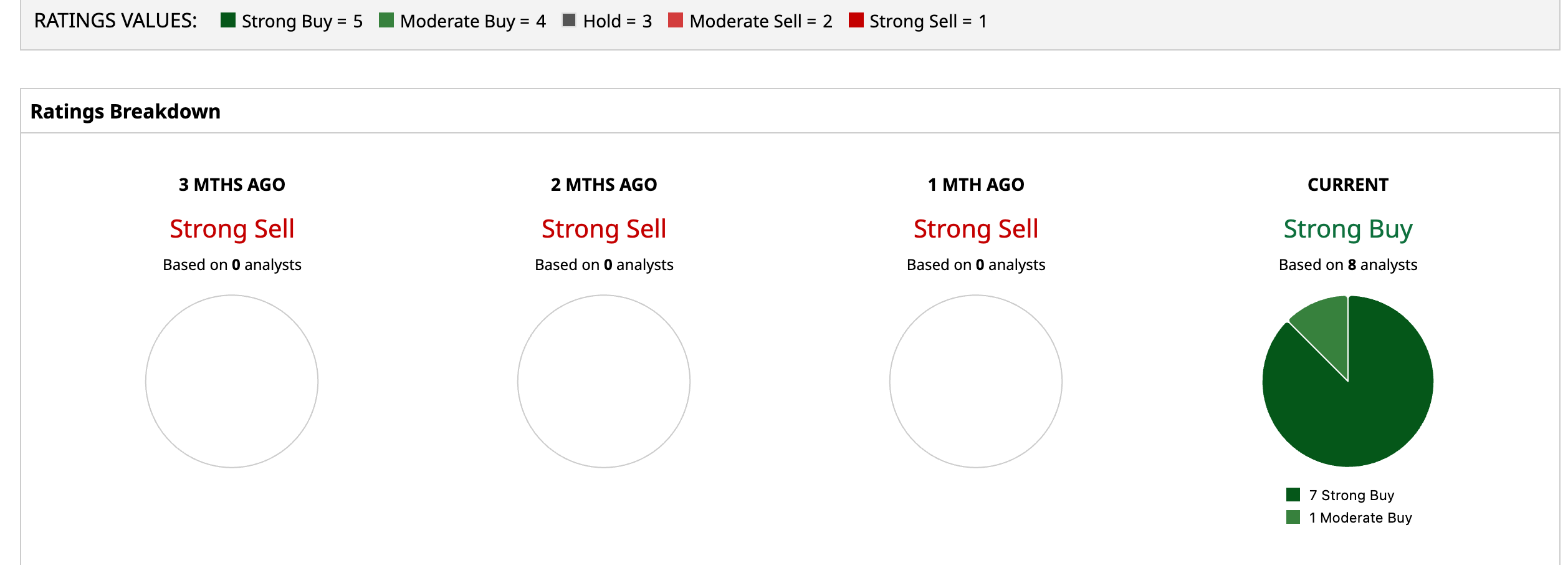

Wall Street is overwhelmingly bullish on CBRS. The stock carries a consensus “Strong Buy” rating, with seven of eight analysts covering the stock recommending a “Strong Buy” and the remaining one analyst assigning a “Moderate Buy” rating.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Wedbush Says Nvidia Blackwell Demand Spikes Amid Tight Tech Supply A $550 Billion Reason to Buy Cerebras Stock SpaceX IPO Demand Is Huge. That May Be The Warning. Dear Marvell Technology Stock Fans, Mark Your Calendars for June 22