With a market cap of $24.3 billion, Dollar General Corporation (DG) is a leading discount retailer in the United States, offering a wide range of low-priced merchandise across the southern, southwestern, midwestern, and eastern regions. It provides products in four main categories - consumables, seasonal items, home products, and apparel—featuring both national brands and private labels.

Companies valued at $10 billion or more are generally classified as “large-cap” stocks, and Dollar General fits this criterion perfectly. Headquartered in Goodlettsville, Tennessee, Dollar General continues to serve customers with everyday essentials at affordable prices.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

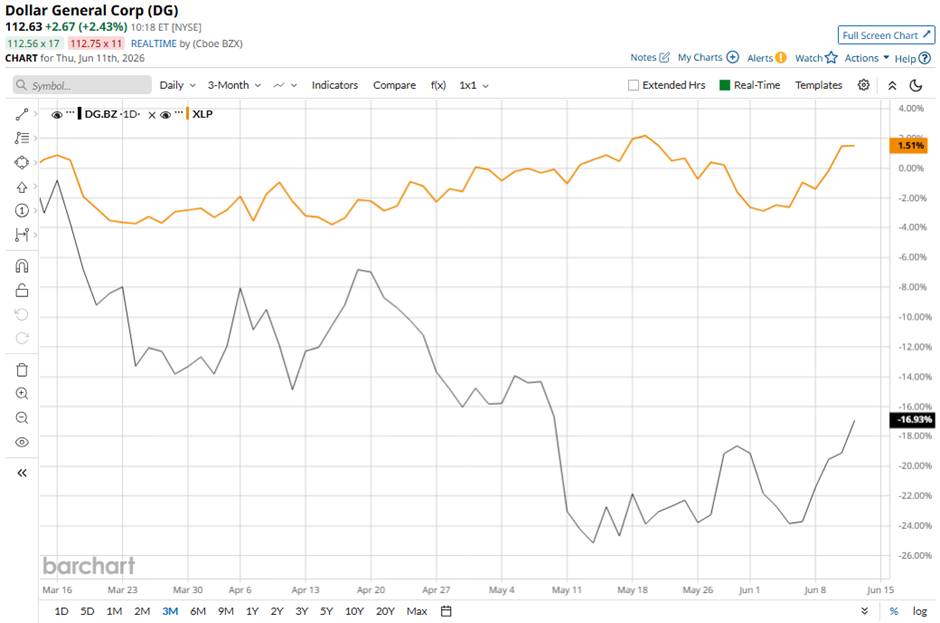

The discount retailer's stock has pulled back 28.8% from its 52-week high of $158.23. Shares of Dollar General have fallen 22.6% over the past three months, lagging behind the broader State Street Consumer Staples Select Sector SPDR ETF’s (XLP) marginal gain over the same time frame.

www.barchart.com

www.barchart.com DG stock has decreased 15.6% on a YTD basis, underperforming XLP’s nearly 10% increase. Longer term, shares of Dollar General have risen marginally over the past 52 weeks, compared to XLP’s 4.8% return over the same time frame.

Despite a few fluctuations, the stock has been trading below its 50-day and 200-day moving averages since last year.

www.barchart.com

www.barchart.com Dollar General shares fell 3.3% on Jun. 2 as management warned that its core low- and middle-income customers remain under pressure from higher gasoline prices, inflation, and SNAP benefit reductions, leading the company to maintain its annual same-store sales growth forecast of only 2.2% - 2.7%. The company noted that rural shoppers are cutting back on travel and limiting shopping trips due to elevated fuel costs that are expected to persist.

While Q1 2026 net sales increased 3.4% to $10.79 billion and EPS rose 12.4% to $2, beating estimates, concerns about weakening customer demand outweighed the improved fiscal 2026 EPS outlook of $7.20 - $7.45.

In comparison, rival Walmart Inc. (WMT) has exceeded DG stock. WMT stock has increased 8.2% on a YTD basis and 25.9% over the past 52 weeks.

Despite DG’s weak performance over the past year, analysts are moderately optimistic about its prospects. The stock has a consensus rating of “Moderate Buy” from the 28 analysts covering it, and the mean price target of $132.62 is a premium of 17.7% to current levels.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

FuelCell Energy Missed on Q2 Revenue. Investors Are Betting That AI Data Centers Will Save the Day. This AI Infrastructure Stock Is Up 650% This Year. Wall Street Still Sees More Upside. Cathie Wood Is Buying the Dip in Broadcom Stock Micron Got a Major Vote of Confidence From Nvidia’s Jensen Huang on AI Returns. I Still Wouldn’t Chase MU Stock Here.