US markets are closed Friday for the Juneteenth holiday, making Thursday the last trading day of the week.

Financial markets saw action/reaction to the expected Fed fund rate announcement Wednesday and imaginary peace deal between the US and Iran.

Don’t Miss a Day: From crude oil to coffee, sign up free for Barchart’s best-in-class commodity analysis.

Grains could focus on weather and technical patterns, though the debate continues as to whether either of these matter these days.

Morning Summary: For those of you who might’ve forgotten markets are closed in the US Friday due to another holiday – Juneteenth. Given this, today – Thursday – could be viewed as Friday, and it is shaping up to be a fun-filled session. After US stock indexes came under increased pressure following Fed Chairman Warsh’s post-FOMC meeting press conference Wednesday afternoon, the Indices sector (US stock index futures) led the commodity complex higher overnight through early Thursday morning. Why? Well, the lead headline pre-dawn talks of the US president and his Iranian counterpart signing a memorandum “aimed to end war”. Not that it was an actual peace “deal”, but rather a memorandum saying the two sides could work on making peace at some point. In other words, nothing new. Still, the Energies sector was deep in the red, outdistanced only by Metals. Out in the Barn, the week has been defined by the ebb and flow of commercial buying in the three major markets. Due to the holiday, USDA’s June 1 Cattle on Feed report will be released Thursday afternoon rather than Friday. However, packers could still wait until late tomorrow to set the cash market. Last, but certainly not least, the US dollar ($DXY) had firmed against global currencies Thursday morning.

Corn: The corn market was under pressure to start the last trading day of the week. The July issue (ZCN26) registered 20,500 contracts changing hands overnight as it slipped as much as 3.75 cents and was sitting within sight of its session low at this writing. Recall July closed 7.25 cents higher Wednesday with the September issue (ZCU26) up 7.0 cents. The National Corn Index came in last night 8.0 cents higher for the day, putting national average basis calculations at 30.25 cents under July and 38.75 cents under September futures. For comparison, the previous 5-year low weekly closes for this week are 21.75 cents under July and 19.5 cents under September, meaning despite its recent firming the basis market remains weak. As for new-crop, the December issue (ZCZ26) was down 3.0 cents at this writing after dipping as much as 3.75 cents overnight. Thursday’s weather forecast calls for more rain across the US Southeast, while parts of the Midwest miss out for a change. The latest 6-to-10-day forecast (June 23 to 27) didn’t change much with below normal temperatures and above normal precipitation expected for much of the eastern two-thirds of the US. Technically, Dec26 is in position to complete a bullish reversal pattern on its weekly chart.

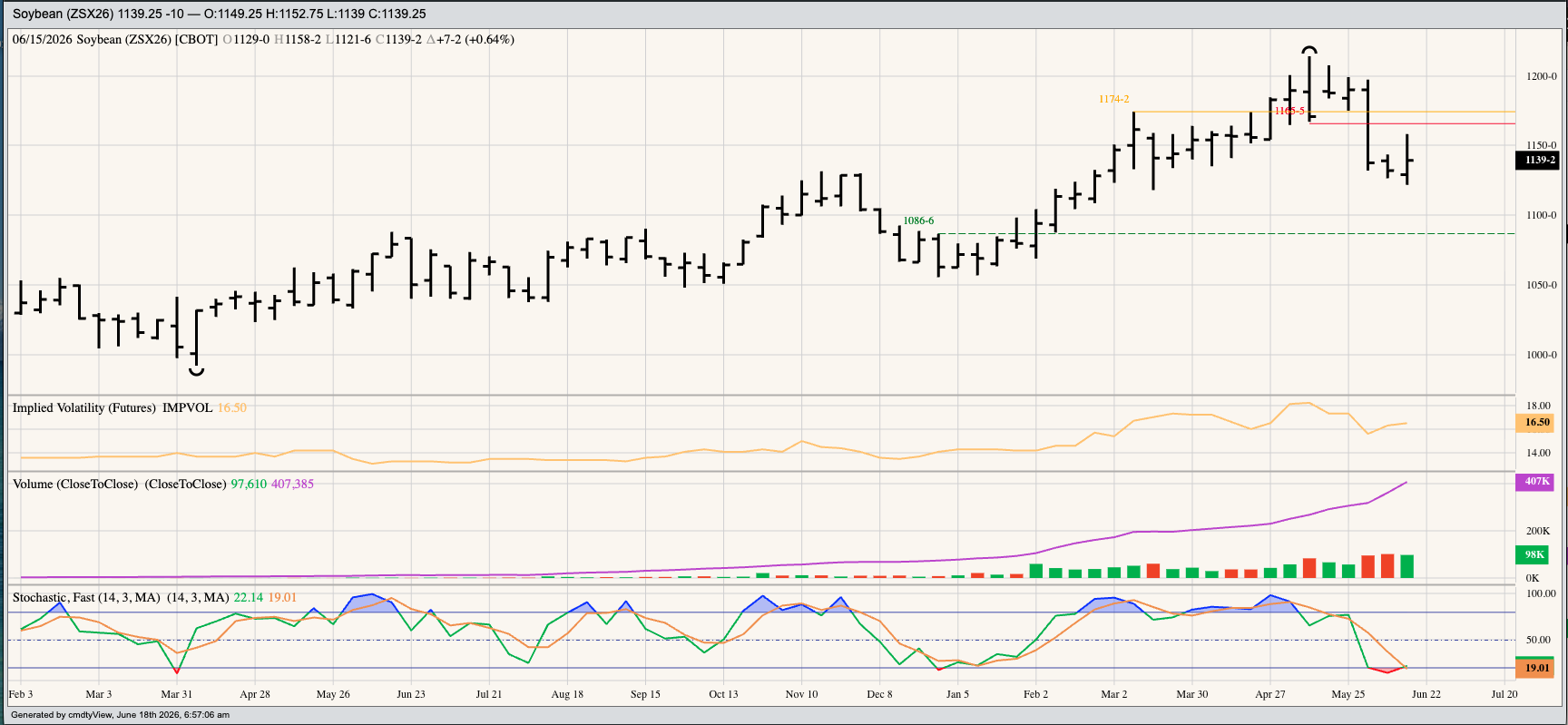

Soybeans: The oilseed sub-sector was in the red across the board, once again led by a sharp selloff in soybean oil. Here we see the July issue (ZLN26) down 1.4 cents (2.0%) after losing as much as 1.6 cents overnight. Some of this was due to the renewed selling in distillates (diesel fuel) where the spot-month contract (HOQ26) lost as much as 10.9 cents (3.4%) overnight and was sitting 8.7 cents (2.7%) in the red at this writing. Recall bean oil led the way lower Wednesday as well, driven in part by increased commercial selling. A glance at the quote screen shows this group continuing to put pressure on the market, though it’s difficult to read much into overnight spreads given the variability in trade volume. Over in soybeans we see the July issue down 8.75 cents after sliding as much as 9.75 cents through pre-dawn Thursday. However, trade volume was only 7,000 contracts with most of the activity in new-crop November (ZSX26). Here we see 15,300 contracts changing hands overnight while the issue lost as much as 9.0 cents and was sitting 7.5 cents in the red. Similar to Dec corn, Nov soybeans are in position to complete a bullish technical pattern on its weekly chart.

Wheat: The wheat sub-sector was mostly higher early Thursday morning. I’ll start with the outlier – the SRW market – as it also showed the largest trade volume overnight. The September issue (ZWU26) was down 1.5 cents after slipping as much as 3.0 cents overnight while registering 16,500 contracts changing hands. It’s interesting to note that was more than Nov soybeans and Dec corn registered through the pre-dawn hours. Keep in mind the September SRW issue has had a big week, closing in the green each session and sitting 24.25 cents higher than last Friday’s settlement. Like Dec corn and Nov soybeans, this has the September issue in position for a bullish technical reversal pattern at today’s close. Over in HRW the September issue (KEU26) was up 1.25 cents for the day 20.25 cents for the week. The HRW market has seen increased commercial support this week, noted in both basis and futures spreads, a reflection of the expanding harvest across Kansas showing poor yields. As is usually the case, the commercial side did not rush to judgement until combines started moving across the US Southern Plains. Heading into Thursday’s session the September-December futures spread covered 41.5% calculated full commercial carry as compared to last Friday’s settlement covering 40%.

On the date of publication, Darin Newsom did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Why is Thursday Friday, Technically? The New World Screwworm Is Still Center Stage for Cattle Prices. Depending on the Day, It’s Either Bullish or Bearish. Grain Market Update: Are Corn, Wheat, and Soybeans Finally Carving Out a Summer Bottom? Are US Cattle Screwed - Again?