Once again, GameStop (GME) is making headlines. This time, a shareholder lawsuit is seeking to delay the crucial July 7 vote on CEO Ryan Cohen's massive compensation package. The court filing accuses the company of a "bait-and-switch," alleging that GameStop changed voting rules and issued a misleading proxy statement.

July 7 is the date shareholders are scheduled to vote on Cohen's pay package, which could ultimately lead to a $35 billion incentive award. However, one investor is attempting to halt that process before the vote takes place.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

The dispute is about more than executive compensation. It raises questions regarding corporate governance, disclosure practices, and the amount of influence Cohen should wield over a company that is still working to prove its turnaround strategy success.

The timing is also notable. GameStop is coming off one of its strongest quarters in years and sitting on a massive cash position. So, investors are weighing strong financial performance against growing governance questions. That combination could keep GameStop shares in focus throughout the summer.

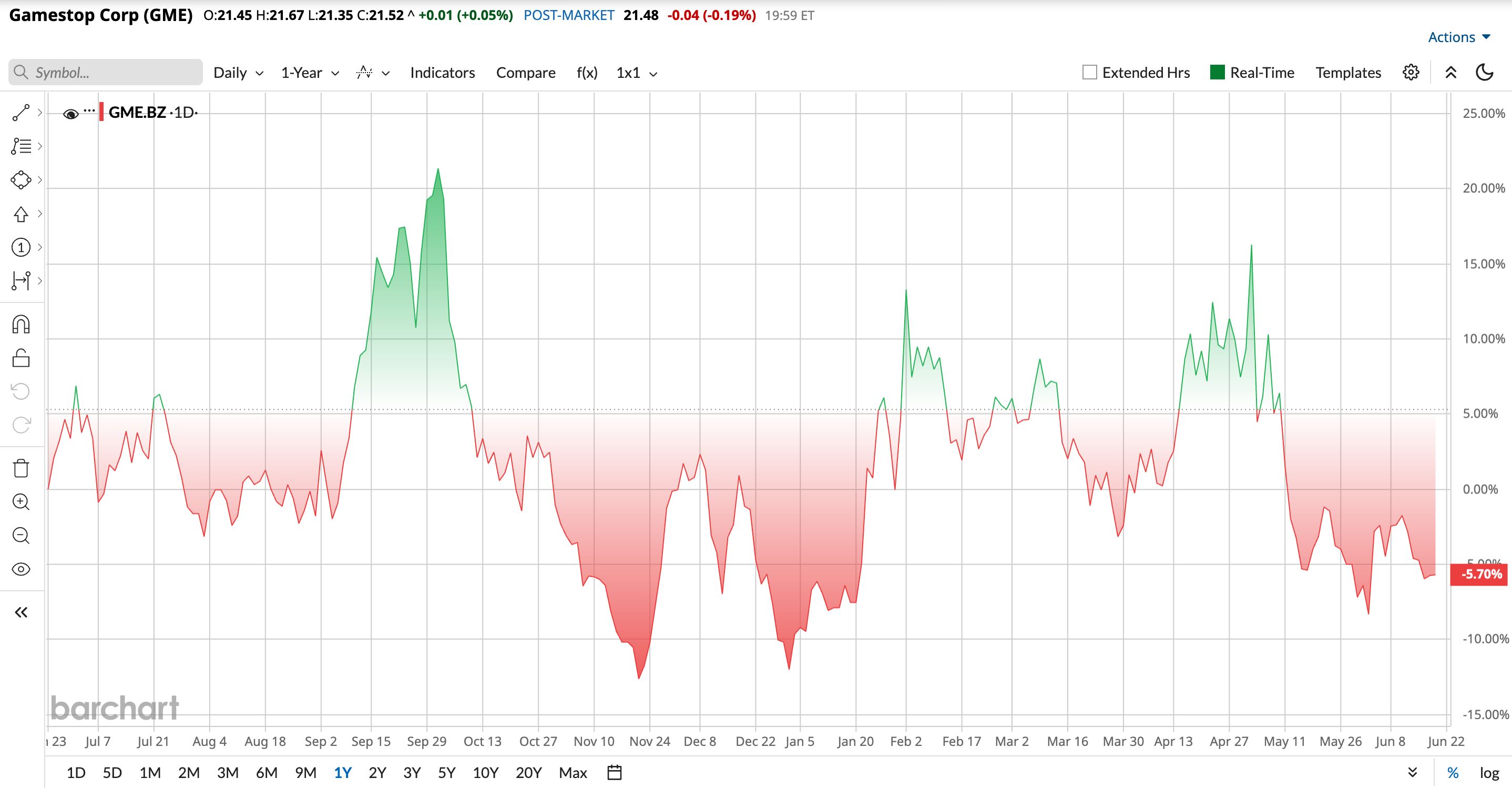

GameStop Stock Has Stabilized in 2026

Despite the sharp ups and downs, the company has managed to gain 7.17% year-to-date (YTD). Investors have responded positively to improving profitability, aggressive capital allocation plans, and a stronger balance sheet.

Despite improved fundamentals, GameStop is not exactly cheap.

The stock currently trades at 19.74 times forward price-to-earnings, compared to a sector median of 15.91 times. Its enterprise value to free cash flow ratio is 7.7.5 times, modestly above the sector median of roughly 7 times.

Investors are clearly willing to pay a premium for GameStop's large cash reserves and turnaround potential. However, the valuation also leaves less room for disappointment if growth slows.

www.barchart.com

www.barchart.com The Latest Quarter Showed Real Progress

GameStop's first quarter of fiscal 2026 delivered results that surprised many skeptics. Net sales increased 14% year-over-year (YOY) to $835.3 million, up from $732.4 million in the prior-year period. At the same time, selling, general, and administrative expenses declined to $201.6 million from $228.1 million. That combination helped operating income surge to a record first-quarter level of $143.3 million.

The biggest headline was profitability. Net income climbed to $389.6 million from $44.8 million a year earlier, while adjusted earnings per share improved to $0.30 from $0.09 last year.

Perhaps even more impressive was the balance sheet. Free cash flow totaled $333.1 million during the quarter. Cash, cash equivalents, and marketable securities reached approximately $8.4 billion. Total liquidity stood near $9.7 billion.

Management did not provide formal full-year guidance. However, executives emphasized that the company continues to evaluate acquisition opportunities and other investments that could strengthen long-term growth. Wall Street currently expects full-year earnings of roughly $0.62 per share.

GameStop Is Pursuing Bigger Opportunities

Beyond its core retail operations, GameStop has been active in several new initiatives during 2026.

The company recently launched Power Packs, a digital trading card platform designed to expand its presence in collectibles. Management has also approved a new $2 billion share repurchase authorization extending through 2029.

In addition, GameStop surprised the market with a non-binding proposal to acquire eBay (EBAY) for approximately $55.5 billion, highlighting the company's willingness to pursue transformative opportunities.

These moves show that Cohen is looking beyond traditional video game retailing and exploring ways to deploy the company's enormous cash position.

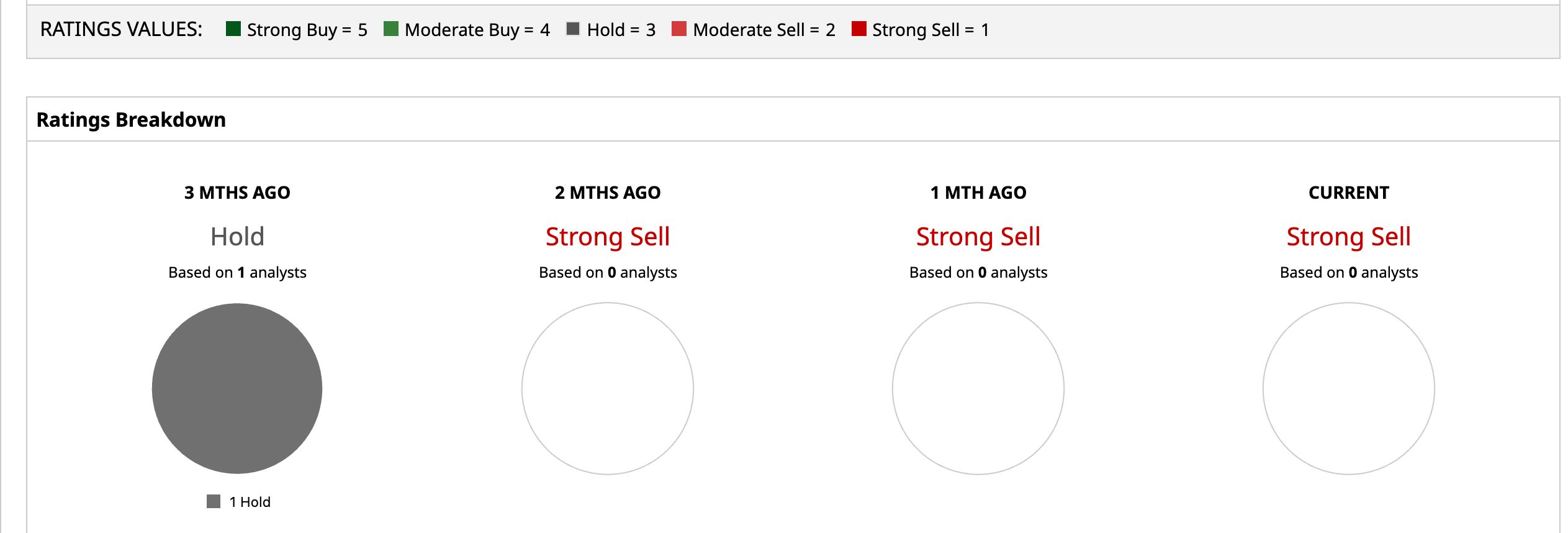

Wall Street Remains Cautious on GME Stock

While GameStop's financial performance has improved significantly, analysts remain cautious.

The average price target stands at $13.50, implying a meaningful of 37.3% downside from recent trading levels.

Wedbush recently maintained its cautious stance, arguing that GameStop's valuation remains difficult to justify despite stronger profitability. Other analysts have echoed similar concerns, pointing to limited long-term revenue growth visibility.

The case for GME is simple. Bulls see a cash-rich company generating profits and pursuing ambitious opportunities. Bears see a stock that still trades well above traditional valuation metrics.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Dear MicroStrategy Stock Fans, Mark Your Calendars for July 4 Applied Materials Is Now More Expensive Than Its Dot-Com Era Peak. AI Demand Justifies the AMAT Stock Valuation. Dear GameStop Stock Fans, Mark Your Calendars for July 7 Mark Cuban Says the Stock Market Makes Guys Like Elon Musk ‘Insanely Rich’ — But Eliminating Billionaires Would Trigger the ‘Worst Depression’ Ever Seen