Alibaba (BABA) has lost nearly a quarter of its market capitalization this year and is drifting towards its 52-week lows. The stock peaked in January amid the optimism over its artificial intelligence (AI) initiatives, but has since plunged. Let's analyze the reasons that have caused BABA stock to crash and whether the pullback is an opportunity to add more shares.

www.barchart.com

www.barchart.com Why Has Alibaba Stock Dropped?

Alibaba has been battling several challenges. Most recently, data from China’s National Bureau of Statistics showed that retail sales in the world’s second-biggest economy fell 0.6% in May. The metric fell short of estimates and marked the first time in three years that China’s retail sales fell. While Alibaba is seen as the leading AI play in China, much of the company’s revenues and profits are tied to its e-commerce platform, whose fortunes are intertwined with China's retail consumption.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

In order to spur sales, Chinese e-commerce companies have announced massive subsidies. However, last week, Chinese regulators rebuked platforms including Alibaba and JD.com (JD) for misleading shoppers as the actual subsidies were much lower than advertised. Notably, there has been a price war in the Chinese e-commerce ecosystem as companies have been aggressively offering discounts to lure buyers amid the economic slowdown. The instant commerce space, a segment that Alibaba sees as its next growth driver, has particularly seen players giving massive discounts, which have taken a toll on their profits and cash flows.

Alibaba’s profits have incidentally nosedived due to instant commerce losses and its burgeoning AI investments. In the March quarter, its adjusted EBITA plunged 84% year-over-year (YOY) to $740 million, while the firm barely reached break-even on the adjusted net profit level. The company posted an operating loss of $123 million and burned $2.5 billion in cash during the quarter, which it blamed on “investment in quick commerce, user acquisition of Qwen app and increase in our cloud infrastructure expenditure.” While cloud has been a bright spot and Alibaba's AI apps have gained traction in China, these have failed to mask the e-commerce slowdown and deteriorating profitability.

If the troubles at home weren’t enough, the Pentagon recently added Alibaba to its list of companies linked to the Chinese military. “Alibaba is a military-civil fusion contributor to the Chinese defense industrial base because it is affiliated with MIIT (Ministry of Industry and Information Technology),” as stated in the Pentagon release. While Alibaba expectedly denied these allegations, the company’s addition to the list dampened sentiments.

Alibaba Stock Forecast

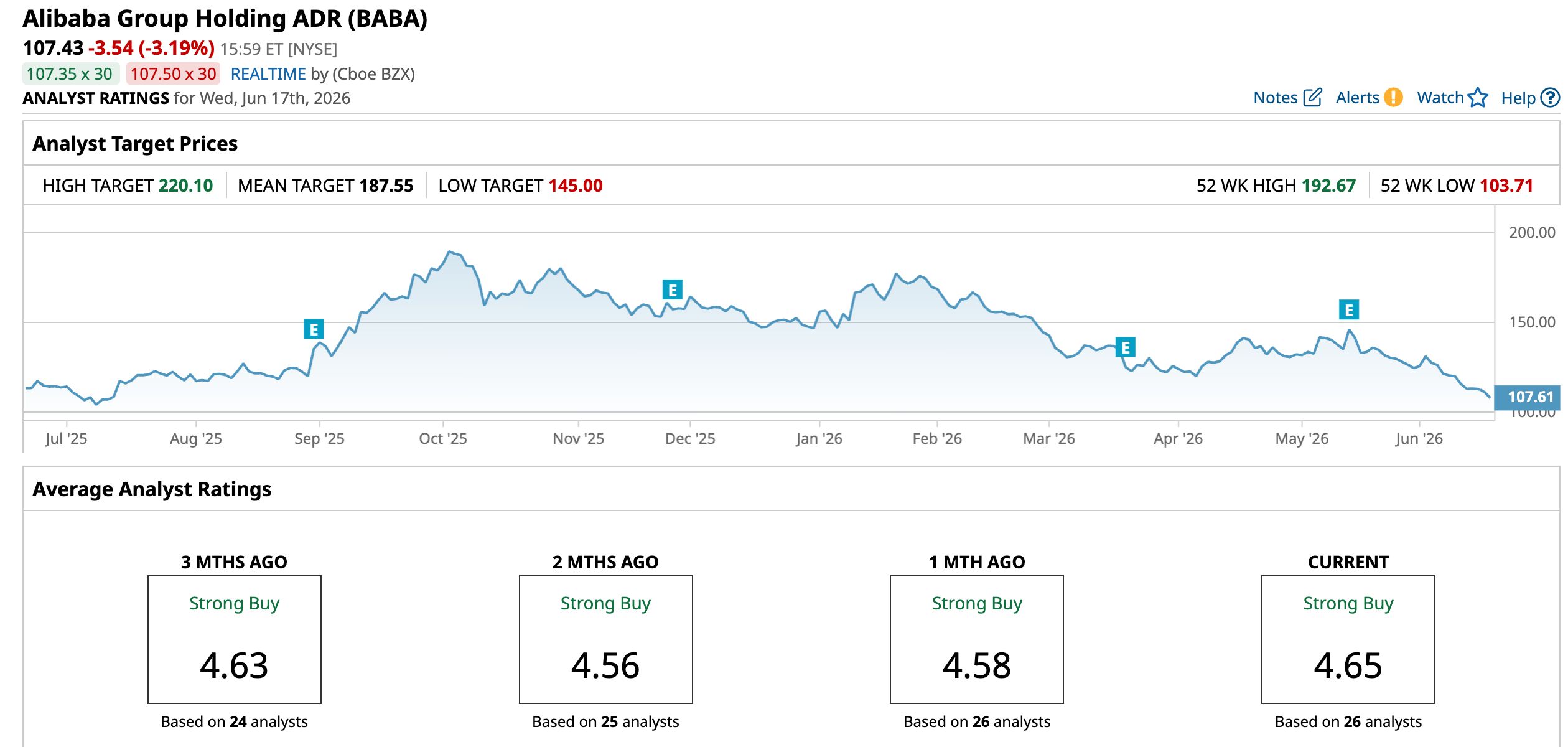

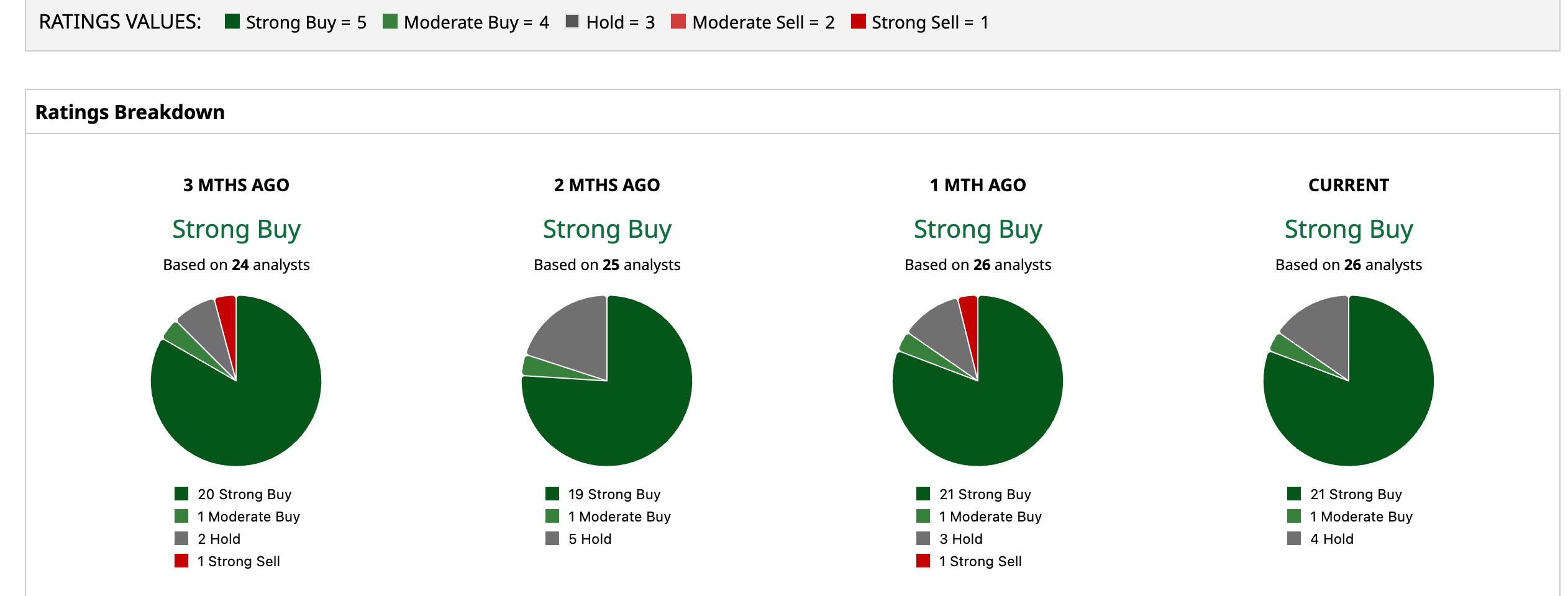

While Alibaba has been out of favor with markets for the last few months, the sell-side analyst community is bullish, and brokerages have gradually raised the stock’s target price, including following the fiscal Q4 2026 earnings release in May. The stock has a consensus rating of “Strong Buy” from the 26 analysts polled by Barchart, and its mean target price of $187.55 is 74.6% higher than the current stock price.

On a related note, Michael Burry recently boosted his Alibaba stake. The “Big Short” investor sees Alibaba as the “most advanced” AI company in China and is constructive on its buybacks.

Should You Buy Alibaba Stock?

While Alibaba’s profitability was under pressure in the last fiscal year, analysts expect the company’s earnings per share (EPS) to rise 109% in the current fiscal year and 40% in the next. This gives us a forward price-to-earnings (P/E) multiple of 16.68 times and a fiscal 2028 P/E of only 11.7 times.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com As a note of caution, while the multiples look attractive, they are based upon analyst earnings estimates, which are not static and subject to regular revisions - both on the upside as well as the downside. However, I believe Alibaba’s profits should increase considerably over the next couple of years as the unit economics of its instant commerce improve and its AI investments start paying off.

Alibaba expects the combined cloud and AI revenues over the next five years to reach $100 billion. Notably, AI, particularly chips, is a high-focus area for the Chinese government as it pushes for domestic production of AI chips and reduces reliance on imports from U.S. giants like Nvidia (NVDA).

Key triggers for BABA in the near term include a possible stimulus from the Chinese government to arrest the slowdown. Over the medium term, listing of its chip unit T-head and fintech subsidiary Ant Financial would help unlock shareholder value.

Overall, I believe that the worst is nearly over for Alibaba, and we should see a recovery in this beaten-down Chinese tech giant sooner rather than later. The stock's valuations look too compelling to ignore now, particularly for patient investors.

On the date of publication, Mohit Oberoi had a position in: BABA , NVDA . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

SpaceX Is Buying Cursor for $60 Billion. What That Means for SPCX Stock. Dear Walmart Stock Fans, Mark Your Calendars for June 22 A Short Squeeze Could Be Brewing in La-Z-Boy Stock Investors Should Be Highly Skeptical About Elon Musk’s Revenue Targets for SpaceX