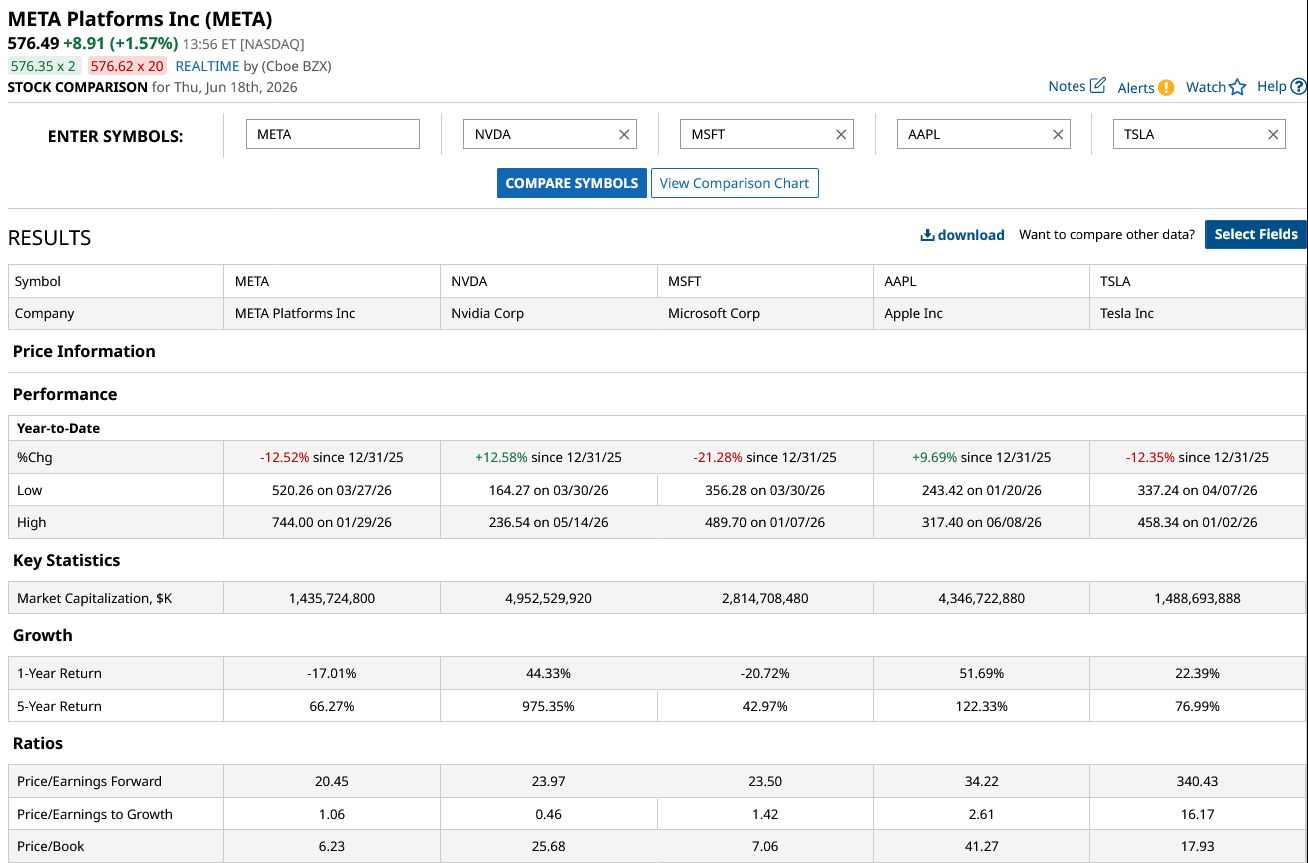

Meta Platforms (META) stock is down nearly 28% from its 52-week high and has looked frail over the last three months. While the year started well for Meta, it soon came under pressure amid both macro and company-specific issues. Let’s examine what’s wrong with Meta, which is the second-worst-performing Magnificent 7 stock this year after Microsoft (MSFT).

www.barchart.com

www.barchart.com What’s Wrong with Meta Platforms?

On a macro level, the artificial intelligence (AI) trade has moved on from Mag 7 to memory and chip companies other than Nvidia (NVDA), which had been the predominant AI play until about a year back. Moreover, SpaceX’s (SPCX) listing squeezed in funds from other tech giants towards what is a purer play on Elon Musk than Tesla (TSLA).

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Meta’s regulatory troubles have also been at the forefront this year. The U.K. has joined ranks with Australia and will ban kids below the age of 16 from using social media by spring next year. Moreover, several European countries are at various stages of enforcing social media bans for kids. While the efficacy of these bans is debatable—the kids are a lot smarter these days—there are legal problems back home that Meta admits are a hanging sword.

In March, a Los Angeles jury found that Meta and YouTube were negligent in protecting children on their platforms—and deliberately structured their platforms to make them addictive. While the damages were a drop in the ocean for these behemoths, they did open the floodgates for more such litigation.

During the Q1 2026 earnings call, Meta CFO Susan Li said, “We continue to see scrutiny on youth-related issues and have additional trials scheduled for this year in the U.S., which may ultimately result in a material loss.”

Then there is the raging debate over Section 230, which provides immunity to platforms for the user-generated content that they host. No one really expects that protection to be axed as a whole, but there is a growing clamor for some restrictions on social media platforms, which, if it happens, could lead to higher compliance costs for these companies at the least and upend the business model in the worst case.

Meta Has Failed to Win Over Markets With Its AI Strategy

Coming to more company-specific issues, despite planning to spend up to $145 billion on capex this year, much of which would be towards building AI infrastructure, Meta has been struggling to convince markets that its AI strategy is on the right track. It does not help that, unlike other hyperscalers, it does not have a cloud business, which is booming and helps investors correlate the AI capex to growth.

Meta has laid off several employees, and at least internally, the management has admitted that it screwed up. In an internal note, Meta’s chief technology officer, Andrew Bosworth, admitted that the restructuring of the AI team was “atrocious” and “left entire teams in the lurch.” Previously, CEO Mark Zuckerberg also admitted to making “mistakes” as it restructured its workforce.

Meta has also been restructuring its business to develop AI agents that can do tasks currently performed by its employees, an initiative that hasn’t gone well with its workforce. The frequent layoffs and employee surveillance measures, which were subsequently scaled back following protests from employees, have further demoralized employees, something Bosworth also talked about in the memo.

Meanwhile, according to reports, Emily Dalton Smith, who was heading the company’s “AI for work” transformation, has quit the company. Smith, who had been with the company for over a decade, was responsible for its main internal enterprise AI assistant, Metamate, among others. Losing a top executive leading a key AI team further dampened sentiments towards Meta.

How to Play META Stock Now?

I have been bullish on Meta for the last few months, but the price action hasn’t aligned with my expectations. While it has announced new AI monetization initiatives, it hasn’t been able to win over markets.

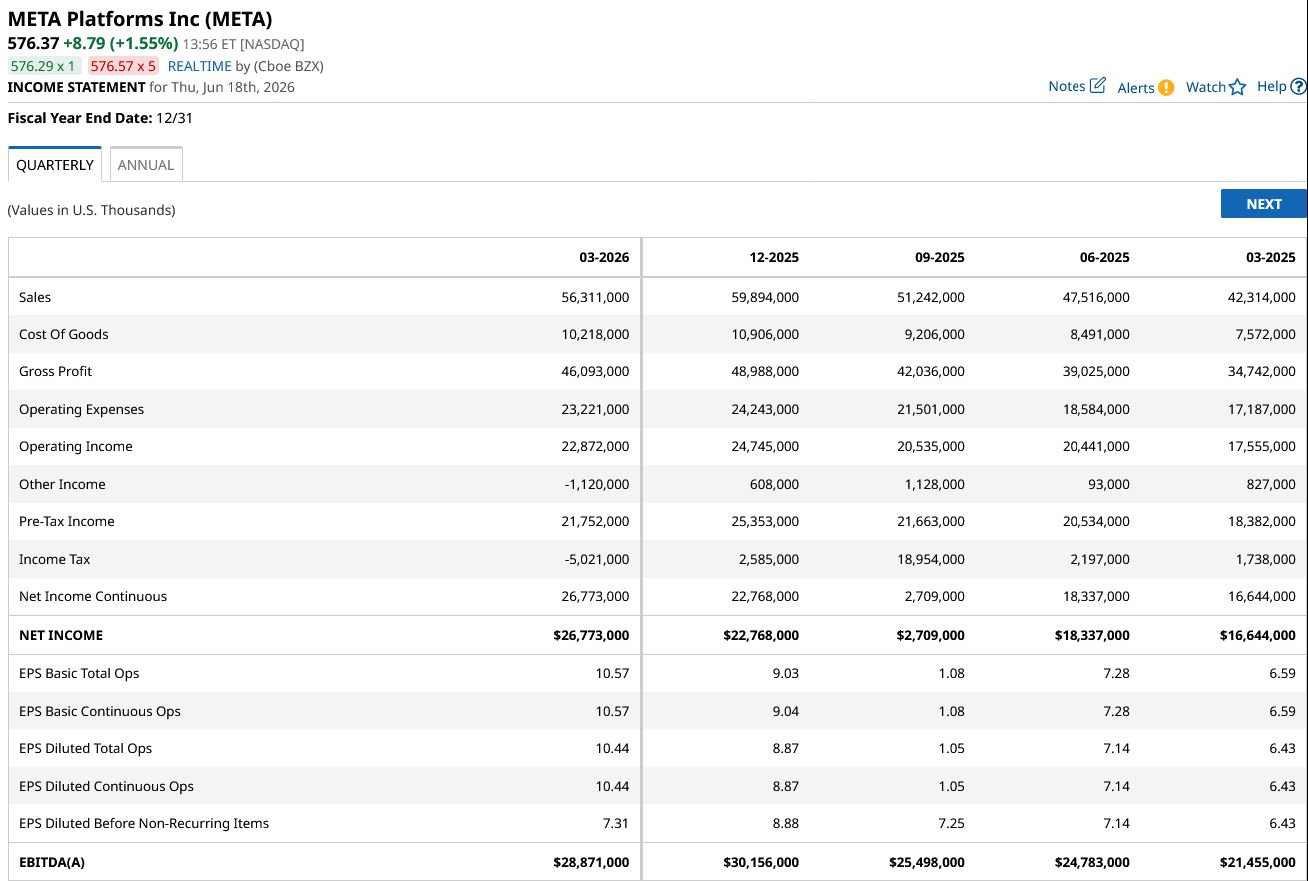

On a more optimistic note, despite all the talk of Meta not effectively monetizing its AI capex, its core ad business has been doing remarkably well. The company’s revenues rose by an impressive 33% year-over-year (YoY) in Q1 2026, the highest growth since 2021. AI-powered personalized ads have been a key driver of that growth. For context, only Nvidia (NVDA) reported a higher growth in the most recent quarter, even though the reporting period is not similar for the two companies.

The concerns over employee discontent and regulatory headwinds are for real, and Meta has been struggling to justify its burgeoning AI capex. I, meanwhile, continue to stay invested in META stock and hold it for the long term, given the company’s moat and near monopoly in the social media space. Meta’s profitability is expected to stay challenged this year, but things should improve in the coming years as revenue growth and restructuring initiatives would help buoy the bottom line. Patience would be the key here, and while the stock is still prone to more downside in the short term, it should deliver the goods for those willing to ignore the short-term noise.

www.barchart.com

www.barchart.com On the date of publication, Mohit Oberoi had a position in: META , MSFT , TSLA , NVDA . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Nothing Seems to Be Going Right for Meta Platforms. How to Play META Stock Here. Hormuz Status, MU Earnings and Other Key Things to Watch this Week Why This Analyst Thinks Nano Nuclear Energy Stock Can Gain 78% from Here BABA Stock: The Physical AI Race Heats Up as Alibaba Releases New AI Models for Robots