EV-making juggernaut Tesla (TSLA) has reported its second-quarter vehicle delivery and production numbers above expectations. The company delivered 480,126 vehicles during the quarter, representing a 25% year-over-year (YoY) increase, while analysts expected around 406,600 deliveries. Tesla produced 451,758 vehicles in Q2.

While markets did not reward the news, as TSLA stock dropped 7.5% intraday on July 2, this indicates a turnaround as Tesla tries to stage a comeback from consecutive annual declines in auto sales. High oil prices were a tailwind for Tesla during the quarter. However, with oil prices returning to pre-war levels, the second half might not show blockbuster numbers.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

To counter this, and due to heightened competition from Chinese and European automakers, Tesla has to sell lower-cost versions of its Model 3 and Model Y and has begun selling its Full Self-Driving (Supervised) driver assistance program in some markets. Tesla is also preparing to ramp up production of its Semi electric trucks, begin manufacturing its driverless Cybercab, and launch production of its Optimus humanoid robots.

Let's take a closer look at Tesla before its Q2 earnings release.

About Tesla Stock

Tesla is a leading force in the EV industry, helping define the market with its electric vehicles, battery technology, and charging network. Headquartered in Austin, Texas, the company is now drawing fresh attention through new vehicle plans, robotaxi ambitions, and continued expansion of its manufacturing and technology base. Its influence extends beyond car sales, shaping how the wider auto industry approaches electrification. The company has a massive market capitalization of $1.48 trillion.

Investors have become optimistic about Tesla’s growth story beyond just car sales. The market is pricing in the company’s push into robotaxis and autonomy as it expands into new cities, keeping the company’s long-term valuation tied to AI and robotics rather than only EVs. In addition, Tesla’s energy storage business has been seen as an important growth offset as the automotive side faces margin pressure and fading regulatory credits. Over the past 52 weeks, the stock has gained 39%.

However, TSLA stock has dropped 9% year-to-date (YTD) due to weaker core auto fundamentals, especially softer sales in key markets, pricing pressure, and rising competition. The shares had reached a 52-week high of $498.83 in December 2025 but are down 18% from that level.

www.barchart.com

www.barchart.com Tesla still has a gigantic valuation. On a forward-adjusted basis, its price-to-earnings (non-GAAP) ratio of 185.71x is considerably higher than the industry average of 16.22x.

Tesla’s Q1 Earnings Showcased Growth

Tesla’s Q1 automotive revenues increased by 16% YoY to $16.23 billion, while total revenues also climbed by 16% to $22.39 billion, as vehicle deliveries increased by 6% from the prior-year period. The company’s non-GAAP EPS increased by a robust 52% YoY to $0.41. In Q1, Tesla’s active FSD subscriptions also increased by 51% to 1.28 million.

Analysts believe Tesla can further improve its bottom line. For the current year, Tesla’s EPS (on a diluted basis) is expected to grow 10.1% YoY to $1.20, followed by a 40% increase to $1.68 for the next year. For the second quarter (to be reported on July 22, after the market closes), analysts expect the company’s EPS to remain flat at $0.27.

What Do Analysts Think About TSLA Stock?

This month, Wall Street analysts have kept their expectations about Tesla quite tempered. Truist Securities analysts kept their “Hold” rating on TSLA stock and raised the price target to $430, citing the company’s AI initiatives and robotaxi ambitions, though uncertainty around FSD timelines still exists.

Analysts from Freedom Broker raised the price target on the stock from $400 to $420 while maintaining a “Hold” rating. The firm cited the company’s Q2 delivery numbers in raising this price target.

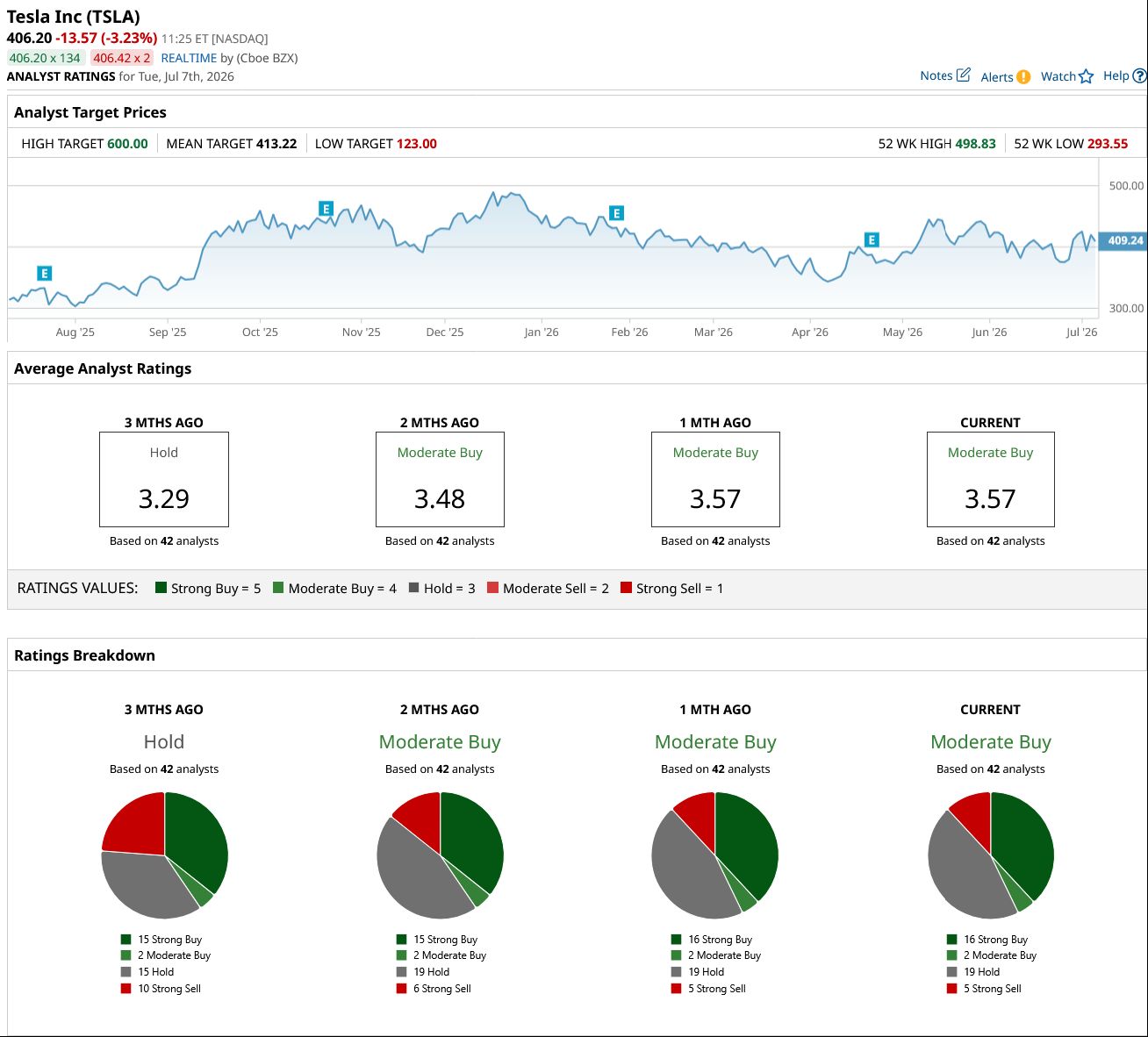

Wall Street analysts are generally taking a positive stance on TSLA stock now, with a consensus “Moderate Buy” rating overall. Of the 42 analysts rating the stock, 16 analysts gave a “Strong Buy” rating, two analysts gave a “Moderate Buy” rating, while 19 analysts are playing it safe with a “Hold” rating, and five analysts gave a “Strong Sell” rating. The consensus price target of $413.22 represents just a 2% upside from current levels. However, the Street-high price target of $600 indicates a 48% upside from current levels.

www.barchart.com

www.barchart.com On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

480,126 Reasons to Buy Tesla Stock Now for the Second Half of 2026 Facing Potential Smartphone Weakness and Tough Competition, Qualcomm Stock’s Outlook Is Not Particularly Strong Volatility Looks Dead. That Means This ETF Could Be Getting Ready to Soar. Down Nearly 30% from Its Recent All-Time High, Corning Stock Looks Like a Buy on the Dip