Artificial intelligence (AI) has been acting as a rising trade for numerous ancillary industries. Nowhere is that more visible than in memory names. With shares of South Korean chip giant SK Hynix (SKHYV) set to commence trading today, and the prevailing elevated prices, the excitement around the memory trade is palpable.

Now, Wedbush has weighed in by raising the price target on Sandisk (SNDK), which specializes in NAND products. The firm sees Sandisk reporting revenues of $8.89 billion in its fiscal Q4. This is higher than both the company's own estimate of $8 billion (midpoint) and the consensus estimate of $8.31 billion. The firm's earnings estimate for the company at $37.64 also exceeds that of the company's estimated earnings of $31.5 per share (midpoint) and the consensus estimate of $33.88 per share.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Justifying the rationale behind the optimism, analyst Matt Bryon wrote in a note to clients, "With our conversations suggesting industry pricing lifted in the high double digits, we believe the company significantly underestimated likely pricing gains with its initial guide. Our new numbers rather assume blended bit ASPs step up roughly 30% q/q, a result we still view as conservative in light of 1) industry trends and 2) Sandisk's willingness to lift pricing, even with Sandisk coming off exceptional ASP growth (triple digit Q/Q) in FQ3."

Thus, Wedbush raised its price target for the stock to $2,000 from $1,200, implying about 8% upside from current levels.

About Sandisk

Founded in 1988 with the current Micron (MU) CEO Sanjay Mehrotra in its founding team, Sandisk is one of the world's leading flash memory companies and a pioneer in NAND storage technology. The company designs and manufactures NAND flash memory, solid-state drives (SSDs), embedded storage, removable memory cards, USB flash drives, and enterprise storage solutions for consumer electronics, personal computers, smartphones, automotive systems, and AI data centers.

Valued at a market cap of $255.8 billion, SNDK stock has catapulted by 699% already this year.

So, as can be seen from the share price action, memory is hot right now. However, are the flows in Sandisk hot as well, or do they really warrant long-term, sustainable flows to its stock? Let's find out.

www.barchart.com

www.barchart.com There In a Flash

Sandisk's expertise in NAND products is well known. In fact, in my last piece on the company, I had anointed it as the NAND king. A primary component of that is its joint venture with Kioxia, one of the world's largest manufacturers of NAND flash memory.

Flash Ventures, the joint venture between Sandisk and Kioxia, ensures that Sandisk has a steady supply of memory wafers from Kioxia's fabs. Moreover, the costs, whether it is the setting up of the fabs or research and development, are shared between the two companies, protecting Sandisk from the heavy capex required to set up and maintain such fabs.

However, the optimism around Sandisk is not just built on a demand-supply play; there is more to it.

First up is High Bandwidth Flash (HBF). Developed in collaboration with SK Hynix, HBF uses a stacked structure similar to High Bandwidth Memory (HBM) to deliver significantly higher capacity (up to 4TB) and bandwidth, making it well-suited for AI inference workloads where large coefficients are streamed into a GPU.

Notably, HBF borrows the vertical stacking and packaging playbook from High Bandwidth Memory, or HBM, and applies it to 3D NAND. The clever part is a parallel sub-array architecture, where the flash core is split into many independent blocks that each get their own read and write channels. That is what lets HBF push bandwidth toward figures that Sandisk pegs above 1.6 TB per second, roughly an order of magnitude beyond a standard SSD, while landing within about 2.2% of the performance of unlimited capacity HBM in the company’s own inference tests.

In terms of capacity, a single HBF stack can reach around 512 GB, dwarfing the roughly 64 GB that HBM4 offers, because NAND is simply denser than DRAM. Further, Sandisk states an HBF device can store eight to sixteen times more data than HBM at broadly similar cost, which translates into a far lower price per gigabyte for AI inference workloads that are read-heavy rather than write-heavy.

Then there is the 332-layer BiCS10, Sandisk’s tenth-generation 3D flash. By stacking 332 layers and pairing that with lateral scaling and a smarter floor plan, BiCS10 reaches an industry-leading 1Tb TLC density above 29 Gb per square millimeter. Measured against the eighth-generation BiCS8 node currently in mass production, that is a 59% jump in bit density. On the performance side, the interface speed climbs to as much as 4.8 GB per second, a 33% gain over BiCS8, which conveniently supplies the NAND side bandwidth that upcoming PCIe Gen6 class enterprise SSDs will demand. Power efficiency improves as well, with Sandisk citing a 10% reduction in data input power and a 34% reduction in data output power, gains that compound meaningfully across the thousands of drives running in an AI data center.

Finally, at 332 layers, BiCS10 sits right at the leading edge, competitive with SK hynix’s 321-layer generation and, on areal density, ahead of even some 400-layer designs from rivals, which shows Sandisk is winning on efficiency rather than layer count alone.

Sandisk's Sensational Numbers

Sandisk's rebirth as a separate entity came along at the right time, when Western Digital (WDC) completely separated the business from itself last year.

Quarterly results have borne testimony to the strength, and the latest one for Q3 2026 was another reminder.

Sandisk delivered exceptional financial performance in the third quarter of 2026, underscoring sustained strong demand for its semiconductor products. Revenue surged 251% year-over-year (YoY) to $5.95 billion. The data center and edge segments, which represent major revenue drivers, posted dramatic increases of 645% and 295%, respectively, to $1.47 billion and $3.66 billion. Non-GAAP gross margins expanded sharply to 78.4% from 22.7% in the year-ago period.

Earnings per share reached $23.41, a significant improvement from a loss of $0.30 per share in the third quarter of 2025, marking another period of beating analyst expectations.

Cash generation was robust as net cash from operating activities climbed to $3.04 billion from just $26 million in the prior year quarter. Overall, Sandisk closed the period with $3.74 billion in cash and no short-term debt on its balance sheet, and a remaining performance obligations, or RPO, value of about $42 billion.

For the fourth quarter, the company guided for revenue between $7.75 billion and $8.25 billion, along with earnings per share in the range of $30 to $33. Analyst estimates stand at $8.15 billion for revenue and approximately $33 per share.

Following the substantial run-up in its stock price, some observers might expect Sandisk to appear richly valued. However, current metrics suggest otherwise. For instance, the forward P/E ratio of 26.01 times remains reasonable when measured against sector medians. However, there is a substantial gap between the forward P/S and P/CF of 12.94 and 29.81 and the sector medians of 3.35 and 18.87, respectively.

Analyst Opinion on SNDK Stock

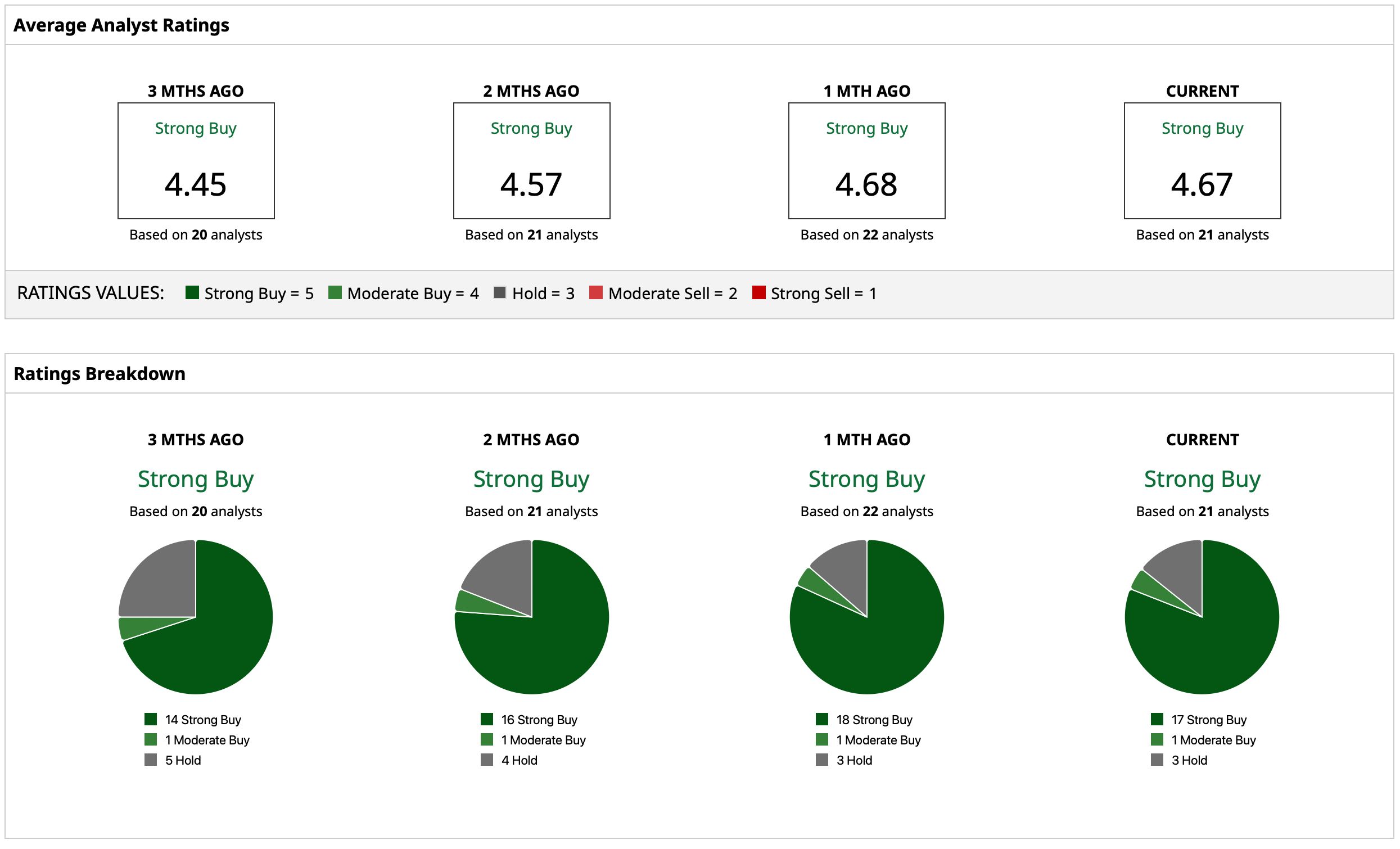

Thus, analysts have deemed SNDK stock to be a consensus “Strong Buy,” with a mean target price of $2,194.42. This denotes a potential upside of 15% from current levels. Out of 21 analysts covering the stock, 17 have a “Strong Buy” rating, one has a “Moderate Buy” rating, and three have a “Hold” rating.

www.barchart.com

www.barchart.com On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Unusual Options Activity in This 1 Stock Highlights a Bet on Big Volatility with Capped Downside and Unlimited Upside As SK Hynix Debuts on the Nasdaq, Wedbush Is Still Betting on More Upside for Sandisk Stock Too China Is Quickly Becoming Nvidia Stock’s Biggest Long-Term Risk. Here’s Why. Here Is Why Meta’s ‘Iris’ Chip Could Help the Company Finally Break Free From Nvidia’s Shadow