Atlanta, Georgia-based Assurant, Inc. (AIZ), founded in 1892, has built a global business around protection in everyday life. With a market capitalization of about $13.6 billion, the company operates across North America, Latin America, Europe, and Asia-Pacific, focusing on homes, vehicles, and connected devices.

Its Global Lifestyle segment supports mobile devices, consumer electronics, appliances, and auto-related services, while also offering select financial and insurance products. Meanwhile, Global Housing anchors the portfolio with homeowners, renters, flood, and manufactured housing insurance. Formerly known as Fortis, Assurant adopted its current name in 2004, reflecting a sharper focus on modern risk protection.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

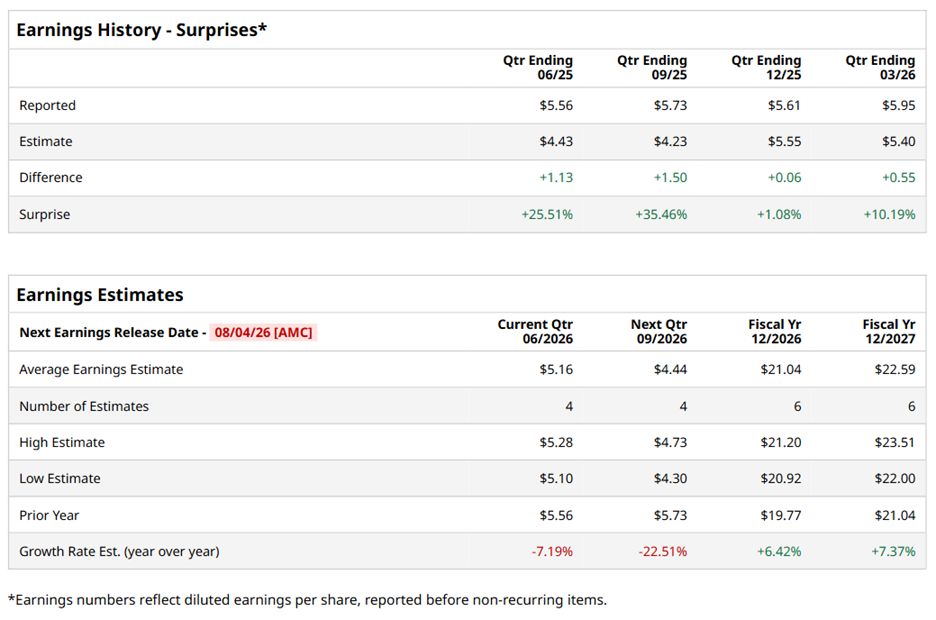

The lifestyle and housing solutions specialist is expected to announce its second-quarter 2025 earnings report on Tuesday, Aug. 4, 2026, after the market closes. Analysts estimate earnings of $5.16 per share, a 7.2% decline from $5.56 per share reported in the year-ago quarter. However, the company has an impressive earnings surprise history. It has surpassed analysts’ earnings estimates in each of the past four quarters.

For fiscal 2026, analysts expect EPS to rise 6.4% from $19.77 reported in fiscal 2025 to $21.04, and then rise by another 7.4% year over year (YOY) to $22.59 in fiscal 2027.

www.barchart.com

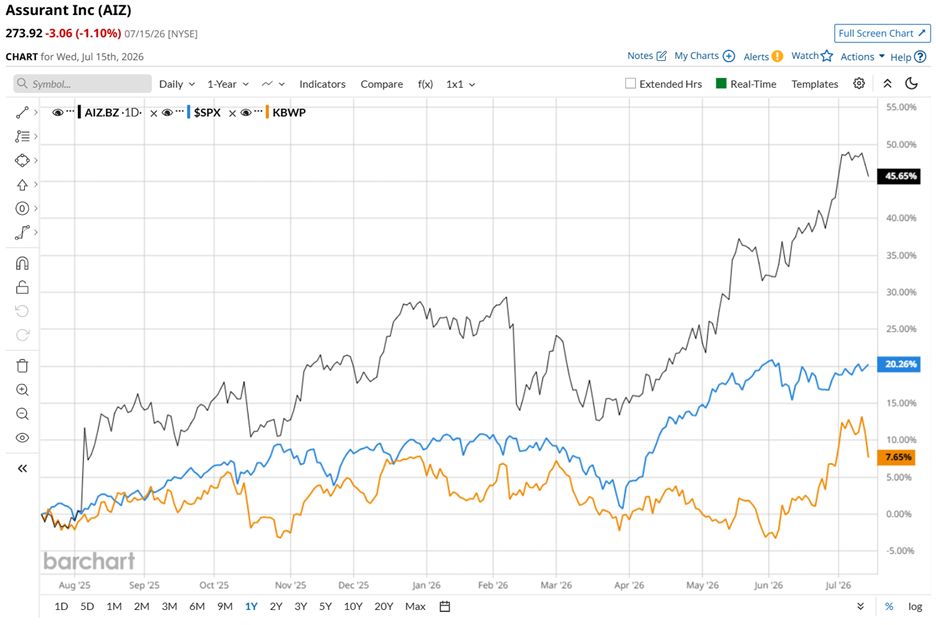

www.barchart.comAIZ’s performance has been impressive. The stock has surged 47.8% over the past 52 weeks, outperforming the S&P 500 Index’s ($SPX) 21.3% rise and also the Invesco KBW Property & Casualty Insurance ETF’s (KBWP) 9.6% increase over the same time frame.

www.barchart.com

www.barchart.comMuch of AIZ stock’s momentum has been fueled by strong execution. Investors cheered the company’s first-quarter results after adjusted earnings came in at $5.95 per share, well above Wall Street’s estimate, while revenue grew 11.3% YOY to $3.4 billion. The upbeat report was followed by a stronger full-year profit outlook and a continued focus on rewarding shareholders, sending the stock 3.5% higher on the day of the earnings release. Add to that a dividend track record spanning more than two decades, and it is easy to see why investors have remained confident in the name.

Analysts, overall, remain upbeat on the stock, assigning it an overall “Strong Buy” rating. Among the nine analysts covering the stock, six are recommending a “Strong Buy,” one advises a “Moderate Buy,” and the remaining two suggest a “Hold.”

AIZ’s average analyst price target of $292.29 suggests the stock has upside potential of 6.7%. The Street-high target of $310 implies AIZ could rally as much as 13.2% from here.

On the date of publication, Sristi Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

2 Reasons to Feel Bullish on GOOGL Stock Ahead of Alphabet’s Q2 Earnings Stocks Slip Before the Open as Chipmakers Extend Slide, U.S. Retail Sales Data and Earnings on Tap This Dividend Stock Trading Near Multi-Year Lows Is a Risky Buy With Significant Upside Potential AEHR Stock Skyrockets After Q2 Earnings Beat-and-Raise