The Campbell's Company CPB used its fiscal third-quarter 2026 earnings call to outline how it plans to navigate a more challenging operating environment heading into fiscal 2027. While management highlighted encouraging trends in Meals & Beverages and signs of stabilization in parts of Snacks, the discussion was dominated by inflation concerns, productivity initiatives and portfolio simplification efforts.

Executives repeatedly emphasized that the focus is shifting toward protecting margins, strengthening core brands and improving operational efficiency as external cost pressures intensify. The call offered investors a clearer view of management’s priorities beyond the reported quarter.

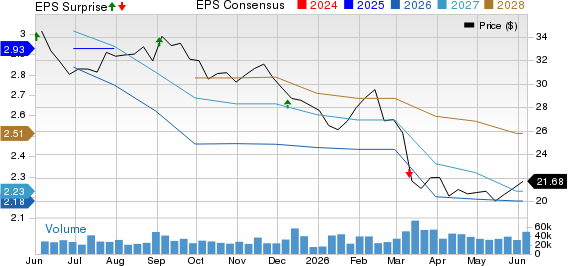

For the third quarter, Campbell’s reported adjusted earnings per share of $0.50, exceeding the Zacks Consensus Estimate of $0.48 by 4.17%. Revenues of $2.37 billion fell short of the Zacks Consensus Estimate of $2.39 billion, delivering a negative surprise of 0.86%.

The Campbell's Company Price, Consensus and EPS Surprise

The Campbell's Company price-consensus-eps-surprise-chart | The Campbell's Company Quote

CPB Faces Rising Inflation Headwinds

Chief financial officer Todd Cunfer said the company had initially expected approximately 3% inflation for fiscal 2027 before recent geopolitical developments altered the outlook.

According to management, elevated oil prices and supply-chain disruptions tied to the Middle East conflict could add another 2% to 3% of inflation, potentially pushing overall cost inflation into the 5% to 6% range.

Beyond energy, Campbell’s is monitoring higher freight expenses, diesel costs, aluminum prices and fertilizer-related impacts that could affect agricultural inputs across its supply chain.

Campbell's Plans Aggressive Cost Actions

Management made clear that productivity will play a central role in offsetting those pressures.

Cunfer highlighted the company's previously announced $100 million SG&A reduction initiative and said Campbell’s intends to accelerate as many savings opportunities as possible into fiscal 2027. The company has already launched an early retirement program to support those efforts.

In addition to cost reductions, executives pointed to revenue growth management initiatives and trade-spending optimization as important levers. Management indicated that pricing remains available if necessary but would be considered only after other mitigation measures are exhausted.

Snacks Overhaul Centers on Simplification

Several analyst questions focused on the future of the Snacks segment, where performance has remained uneven.

Chief executive officer Mick Beekhuizen said simplification is becoming a key strategic priority. The company plans to concentrate resources on core brands and core consumers while reducing complexity across its portfolio.

Management is also evaluating lower-volume SKU tails within several brands. Beekhuizen said eliminating unnecessary complexity could improve manufacturing efficiency, streamline operations and free resources for higher-priority growth opportunities.

CPB Sees Momentum in Core Brands

Despite broader challenges, management highlighted progress in several important businesses.

Goldfish continues to stabilize following focused investments aimed at families with children. Beekhuizen described the brand as a critical growth and profit driver and said Campbell’s intends to continue supporting its recovery.

Fresh bakery operations have also improved. Cunfer noted that better on-shelf availability is allowing the company to restore promotional activity after supply-related disruptions weighed on performance earlier in the year.

Campbell's Benefits From At-Home Cooking Trends

The strongest business momentum remains within Meals & Beverages.

Beekhuizen said consumers continue to prepare meals at home at elevated rates, supporting demand for cooking soups, sauces and premium brands such as Rao’s and Pacific. Management expects those trends to remain favorable moving forward.

The company also sees opportunity in innovation. New condensed sauce products are being developed to build on consumer demand for convenient meal preparation and broader flavor variety, extending Campbell’s presence within home cooking occasions.

Analysts Press on Leverage and Capital Allocation

A Barclays analyst asked management how rising costs could affect capital allocation priorities and shareholder returns.

Cunfer reiterated that maintaining an investment-grade credit rating remains a top objective. Management is prioritizing leverage reduction through stronger earnings, working-capital improvements and disciplined capital expenditures.

The company also confirmed that mergers and acquisitions are not currently being considered. While the dividend remains important, Campbell’s indicated it has no plans to increase the payout in the near term. Executives additionally said hybrid debt issuance remains under evaluation as a potential balance-sheet management tool.

CPB Focuses on Margin Recovery

Analysts also questioned management about pricing strategy and promotional effectiveness as inflation accelerates.

Executives said the company is becoming more selective with trade spending, focusing on promotions that generate stronger returns. Cunfer noted that feature-and-display programs produce significantly better results than standalone temporary price reductions.

Management also highlighted improving revenue growth management capabilities and pointed to successful price-pack strategies within Goldfish as examples of how execution can drive profitability without relying entirely on broad price increases.

Campbell's Sets Priorities for Fiscal 2027

The overarching message from management was one of disciplined execution.

Leadership acknowledged that inflation and continued weakness in portions of the salty-snacks portfolio create meaningful challenges heading into fiscal 2027. However, executives consistently emphasized productivity, simplification and focused brand investment as the primary responses.

The company appears intent on strengthening margins, improving operational efficiency and supporting its largest franchises while navigating what management expects to be a more volatile cost environment.

Zacks Rank and Style Scores Signal

CPB currently carries a Zacks Rank #5 (Strong Sell). The Zacks Rank is driven primarily by earnings estimate revisions and is designed to identify stocks with the strongest potential performance over the next one to three months.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The stock also holds a Value Score of A, Growth Score of C, Momentum Score of B and VGM Score of B. Under the Zacks methodology, stronger Style Scores can complement stock selection, but the Zacks Rank remains the most important indicator. As analysts revise estimates following the latest earnings report, both the rank and style profile may change.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

The Campbell's Company (CPB): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).