Valero Energy VLO is a leading refining player with a robust network of 14 refineries located across the United States, Canada and Peru. The company has a combined high-complexity throughput capacity of 3 million barrels per day, which distinguishes it from other independent refiners. Valero Energy’s refineries have a combined Nelson Complexity Index of 11.5, implying that they can process a wide variety of feedstock and convert it into higher-value products.

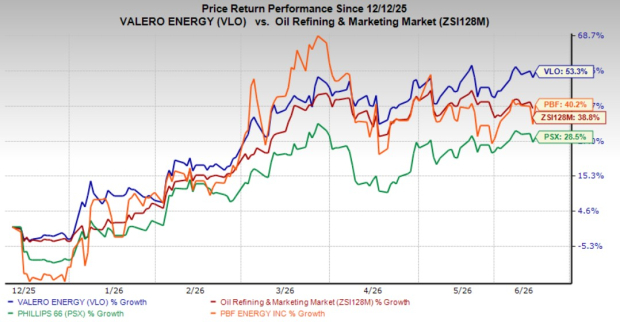

Over the past six months, VLO stock has gained 53.3%, outperforming the industry’s 38.8% growth. Its peers, Phillips 66 PSX and PBF Energy PBF, have grown 28.5% and 40.2%, respectively. While price performance indicates a stock's attractiveness to some extent, it would be wiser to closely examine the company’s current business environment before offering any investment advice.

VLO’s Complex Coastal Refinery Network & Operational Flexibility Aids

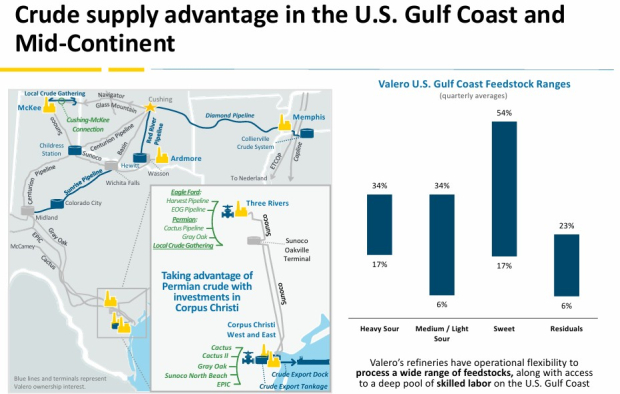

Valero Energy presents a favorable investment case, particularly due to its high-complexity coastal refinery network and the operational flexibility of its refineries. Notably, its advantaged Gulf Coast refining footprint benefits from crude availability and exposure to export markets.

Management stated that during the first quarter, VLO’s Gulf Coast presence enabled it to take advantage of discounted heavy sour crude feedstocks, particularly following increased Venezuelan supply. With the onset of the conflict in the Middle East, these market dynamics became even more pronounced, as certain heavy crude grades, including Canadian heavy crude, began trading at deeper discounts. The company also added that it continues to optimize its crude slate at the Gulf Coast, enabling it to improve refining economics and support better margins.

The heavy sour discounts act as a tailwind for Valero’s business, particularly in the second quarter. Its highly complex refining system is capable of processing heavy sour grades into high-value refined products efficiently. Additionally, the flexibility of Valero’s refinery systems allows it to shift product yields between light products and distillates based on market signals to capture higher margins during volatile times. These factors enable the company to lower its input costs while capturing better refining margins by adjusting its refining mix.

Image Source: Valero Energy Corporation

Valero’s Shareholder Returns Framework and Balance Sheet Strength

Valero combines strong free cash flow generation with a disciplined capital allocation approach. The refining player returned $938 million to shareholders in the first quarter of 2026, implying a 59% payout ratio. Additionally, the company announced a 6% increase in its quarterly cash dividend to reward shareholders. Over the longer term, management has consistently delivered on its commitment to return cash to investors, achieving an average payout ratio of roughly 70% between 2015 and 2025. VLO also highlighted that its outstanding shares have declined by nearly 42% since 2014 through opportunistic share repurchases.

Valero’s capital return program is supported by its strong balance sheet. The company’s debt-to-capitalization ratio, net of cash, stood at 18% at the end of the first quarter. Furthermore, its cash and cash equivalents, combined with the liquidity available under its bank facilities, totaled approximately $11 billion at the end of the March quarter. VLO’s healthy financial position also allows it to return excess cash to investors through share buybacks. The company’s financial strength supports dividend growth and opportunistic buybacks, allowing it to deliver long-term shareholder value.

Valuation Snapshot

The valuation snapshot indicates that investors are now willing to pay a premium for Valero Energy due to the company’s strong fundamentals. This is reflected in VLO’s trailing 12-month enterprise value to EBITDA (EV/EBITDA) of 7.84x compared with the broader industry average of 5.87x. However, it is currently trading cheaper compared to its peers, PSX and PBF, which are trading at 12.93x and 9.88x trailing 12-month EV/EBITDA, respectively.

Image Source: Zacks Investment Research

Time to Bet on the Stock or Wait?

Valero Energy is expected to benefit from its Gulf Coast refinery network that allows it to take advantage of discounted heavy sour barrels. Further, the operational flexibility of its refineries enables it to convert cheaper feedstock into high-value products, thereby supporting profitability.

Given the current business environment and its disciplined shareholder return framework, investors should consider buying the VLO stock, sporting a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.7% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Valero Energy Corporation (VLO): Free Stock Analysis Report

Phillips 66 (PSX): Free Stock Analysis Report

PBF Energy Inc. (PBF): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).