Fashion is fickle, just ask former Wall Street darling lululemon athletica inc. LULU. The athleisure power, which changed fashion for a period of time, is facing changing trends, increased competition, and other headwinds.

Lululemon’s earnings revisions went into a downward spiral starting in late 2024. Its earnings outlook took another turn for the worse after it reported its Q1 FY26 results on June 4.

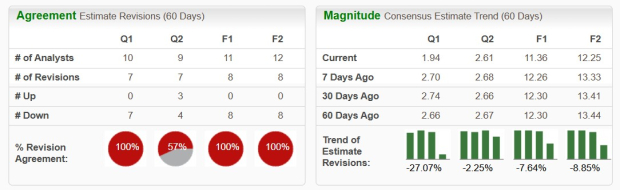

LULU’s most recent downward earnings revisions earn the athletic apparel maker a Zacks Rank #5 (Strong Sell). The stock has also tanked 50% in the last year.

Should Investors Stay Away from LULU Stock Right Now?

Lululemon is finally facing slowing growth in the U.S. and North America after a banner stretch of expansion that saw it average 23% revenue growth between 2018 and 2023. The rapid expansion of rivals Alo, Vuori, and countless other online-only startups is also contributing to LULU's slowing comparable store sales in its critical Americas region.

On top of that, broader fashion trends appear to be moving away from Lululemon’s core offerings. Even though LULU has actively expanded its business in an effort to adapt, Wall Street is unconvinced it is ready to turn things around.

Image Source: Zacks Investment Research

LULU grew its FY25 revenue by 5%, marking by far its lowest ever YoY sales expansion as a public company. Before that, 2024’s 10% revenue growth was its slowest year of growth.

The company’s Americas comparable sales decreased 3% in fiscal 2025. Lululemon followed up that rough performance in its most important market with a 5% YoY decline in Americas comps in the first quarter of FY26.

The company’s Q2 earnings estimate dropped roughly 27% since its report on June 4, with its FY26 estimate another 8% lower and FY27’s 9% off the pace. The recent downward revisions earn Lululemon a Zacks Rank #5 (Strong Sell), and extend its downward earnings spiral.

Lululemon is projected to grow its revenue by around 0.5% in FY26 and nearly 5% next year. Meanwhile, its adjusted earnings are expected to fall 14% YoY in FY26 and then jump 8% next year, based on current Zacks estimates.

Image Source: Zacks Investment Research

LULU’s 40% YTD dive is part of a ~75% drop from its early 2024 peaks. The fall has it trading where it was in various parts of 2018 and at its lowest ever forward earnings multiple at 9.4X forward 12-month EPS. This backdrop means that investors should likely keep Lululemon on their watchlists and possibly take a nibble at it when management shows Wall Street that a turnaround is on the horizon.

Until then, investors should likely look elsewhere for stocks to buy across the apparel industry and beyond.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

lululemon athletica inc. (LULU): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).