AstraZeneca AZN stock has declined 7.4% in the past three months despite reporting strong first-quarter 2026 results. A key driver of the decline was a pipeline setback. In April, an FDA advisory committee voted against recommending AstraZeneca’s breast cancer drug candidate camizestrant. Subsequently, in May, the FDA announced it would delay its decision on the camizestrant NDA, adding further uncertainty around the program.

However, one-off pipeline setbacks like these should not form the basis of an investment decision. Let’s understand AZN’s strengths and weaknesses to better analyze how to play the stock amid the latest price decline.

AZN’s Strong Portfolio of Blockbuster Drugs

AstraZeneca boasts a diversified geographical footprint as well as a product portfolio with several blockbuster medicines.

The company now has 16 blockbuster medicines, including Tagrisso, Fasenra, Farxiga, Imfinzi, Lynparza (partnered with Merck [MRK]), Soliris and Ultomiris in its portfolio, with sales (product sales and alliance revenues) exceeding $1 billion. These drugs drove AstraZeneca’s 8% top-line growth and 5% core EPS at CER in the first quarter of 2026, backed by increasing demand trends. Almost every new product that has been launched in recent years has done well.

Newer drugs like Wainua, Airsupra, Saphnelo, Datroway (partnered with Daiichi Sankyo) and Truqap also contributed to top-line growth. A key new drug, Baxfendy (baxdrostat), was approved for treatment-resistant hypertension in the United States in May 2026.

AZN Enjoys Strong Position in the Oncology Space

Oncology is AstraZeneca’s biggest segment. The segment contributes roughly 44% of total product sales and continues to be the company’s primary growth driver.

AstraZeneca’s oncology sales were $6.8 billion in the first quarter of 2026, up 16% at constant exchange rate (CER). The strong oncology performance was driven by robust demand for drugs like Tagrisso, MRK-partnered Lynparza, Imfinzi, Calquence and Enhertu (in partnership with Daiichi Sankyo).

Key new cancer drugs in AstraZeneca’s portfolio are Truqap for HR-positive, HER2-negative (HR+ HER2-) breast cancer, and Datroway, co-developed with partner Daiichi, also for HR+ HER2- breast cancer and EGFR-mutant non-small cell lung cancer (NSCLC). These drugs are also contributing to sales growth. Truqap has seen rapid uptake in the U.S. market since launch, with the ex-U.S. market expected to be a key contributor in future quarters. Datroway is seeing strong launch uptake trends.

AstraZeneca is working to strengthen its oncology product portfolio through label expansions of existing products and to advance its oncology pipeline candidates. AstraZeneca also possesses one of the deepest late-stage oncology pipelines in the industry. A key pipeline candidate, camizestrant, an oral SERD, is under review in the United States, the EU and some other countries for HR+ HER2- metastatic breast cancer.

Several Headwinds Hurting AZN’s Top Line

AstraZeneca faces its share of challenges. The loss of exclusivity of mature brands like Brilinta, Pulmicort and Soliris is hurting sales. Generic versions of one of the company's major drug, Farxiga, have been launched in the United Kingdom and some emerging markets. Farxiga lost exclusivity in the United States in April 2026 and its revenues are expected to decline in the United States, Japan and China in 2026.

China, though an important market for AstraZeneca, remains a somewhat uncertain market due to pricing pressure from volume-based procurement (VBP) programs and ongoing legal and compliance investigations involving the company’s former China head, Leon Wang. VBP-associated stock compensation costs hurt sales of Farxiga, Lynparza and roxadustat in China in the first quarter.

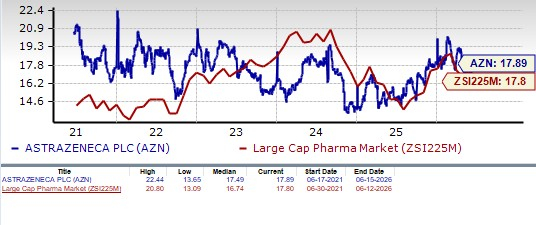

AZN Stock’s Price, Valuation & Estimates

AstraZeneca’s stock has declined 3.6% so far this year against an increase of 5.4% for the industry.

AZN Stock Underperforms Industry

From a valuation standpoint, AstraZeneca is slightly expensive. Going by the price/earnings ratio, the company’s shares currently trade at 17.89 forward earnings, slightly higher than 17.80 for the industry. AZN’s stock is also trading above its 5-year mean of 17.49. The stock is, however, cheaper than other large drugmakers like Eli Lilly LLY and J&J JNJ.

AZN Stock Valuation

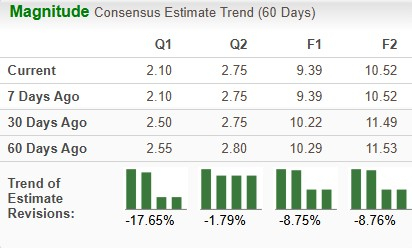

The Zacks Consensus Estimate for 2026 earnings has declined from $10.29 per share to $9.39 per share over the past 60 days. For 2027, earnings estimates have declined from $11.53 per share to $10.52 per share over the same timeframe.

AZN Estimate Movement

Stay Invested in AZN Stock

AstraZeneca’s stock has declined this year, accompanied by downward revisions to earnings estimates. Despite the pullback, the shares still trade at a relatively rich valuation. In addition, several of the company’s established medicines are facing patent expirations and pricing pressures, creating uncertainty about whether revenues from these mature products can be replaced quickly enough by newer launches and pipeline candidates.

However, despite the headwinds, AZN expects continued revenue and earnings growth in 2026. It expects total revenues to grow by a mid-to-high single-digit percentage at CER in 2026, while core EPS is expected to increase by a low double-digit percentage at CER.

The company has also set itself some visible targets for the next few years. It expects to generate $80 billion in total revenues by 2030. By the said time frame, AstraZeneca plans to launch 20 new medicines, with around half of these already launched/approved. It believes that many of these new medicines will have the potential to generate more than $5 billion in peak-year revenues. The company is also on track to achieve a mid-30s percentage core operating margin by 2026.

AstraZeneca’s pipeline is also strong, with pivotal data readouts lined up for 2026.

Considering AZN’s growth prospects, one should stay invested in this Zacks Rank #3 (Hold) stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

AstraZeneca PLC (AZN): Free Stock Analysis Report

Johnson & Johnson (JNJ): Free Stock Analysis Report

Merck & Co., Inc. (MRK): Free Stock Analysis Report

Eli Lilly and Company (LLY): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).