Teva Pharmaceutical Industries Limited TEVA has, for long, been one of the world’s largest generic drug companies. However, Teva is gradually transitioning from a pure-play generics company to a more diversified biopharma company. Its biggest growth driver now is its higher-margin branded/innovative drugs rather than traditional generics.

The company's strategic transformation accelerated under its "Pivot to Growth" initiative. Management has focused on strengthening the branded drugs segment by investing in research and development, pursuing targeted acquisitions and partnerships, and expanding its commercial capabilities in specialty therapeutic areas. Rather than attempting to compete across numerous disease categories, Teva has concentrated on areas where it possesses scientific expertise and can establish meaningful market positions, including neuroscience, immunology and respiratory diseases.

The company is seeing continued market share growth of its newest branded drugs, Austedo, Ajovy and Uzedy. Collectively, sales of Austedo, Ajovy and Uzedy rose 41% year over year to $838 million in the first quarter of 2026.

Global sales of Austedo, one of the major pillars of Teva's branded business, rose 41% to $578 million in the first quarter, backed by strong prescription growth. The drug is approved for movement disorders associated with conditions such as tardive dyskinesia and Huntington's disease. Teva expects Austedo annual revenues to be more than $2.5 billion by 2027 and exceed $3 billion by 2030. The Austedo franchise got a boost from the launch of Austedo XR, a new once-daily formulation of Austedo. Teva launched Austedo in European markets in 2026, which should further contribute to growth.

Global revenues of its migraine drug, Ajovy, rose 35% (constant currency) year over year to $196.0 million in the first quarter. Although Teva is experiencing slightly slower growth of Ajovy in the U.S. market, it anticipates sales to benefit from continued patient growth and launches in additional countries in Europe and international markets. In 2026, Ajovy sales are expected to be in the range of $750 million to $790 million.

Another important branded asset is Uzedy, a long-acting injectable treatment for schizophrenia. Management believes Uzedy has substantial long-term potential because long-acting injectable antipsychotics are increasingly being adopted in psychiatric care. Sales of Uzedy rose 62% to $63 million in the first quarter, with total sales expected to be between $250 million and $280 million in 2026.

The company has also made decent progress with its branded pipeline, which includes olanzapine, a long-acting subcutaneous injectable (LAI) for treating schizophrenia and duvakitug, its anti-TL1A therapy for inflammatory bowel diseases (IBD), ulcerative colitis (UC) and Crohn’s disease (CD). Teva has partnered with Sanofi SNY for duvakitug to maximize the value of the asset. Teva and Sanofi will equally share the development costs globally. While olanzapine LAI is under review in the United States and the EU, Sanofi is conducting phase III studies on duvakitug.

In April, Teva announced a definitive agreement to acquire Emalex, including its lead asset, ecopipam. The acquisition closed in June. Ecopipam is a late-stage, first-in-class therapy for pediatric Tourette syndrome, which is a natural fit for Teva’s central nervous system franchise. Earlier this month, Teva filed a new drug application to the FDA seeking approval for ecopipam.

While generics remain an important part of Teva's business and continue to generate substantial revenues and cash flows, management's strategy over the past several years has increasingly centered on building a sustainable portfolio of innovative medicines that can drive higher growth and improve profitability. Branded medicines are expected to become increasingly important contributors to Teva's long-term growth because they generally offer significantly higher margins and longer periods of market exclusivity than generic products.

In 2022, only about 9% of Teva’s revenues came from its branded drugs, which has now increased to more than 20%. Teva anticipates generating more than $5 billion in revenues from its branded products by 2030.

If Teva continues to successfully commercialize its existing branded products and advance its pipeline, the company could evolve into a more diversified pharmaceutical company with a healthier balance between stable generics operations and higher-growth innovative medicines.

TEVA’s Price, Valuation & Estimate Discussion

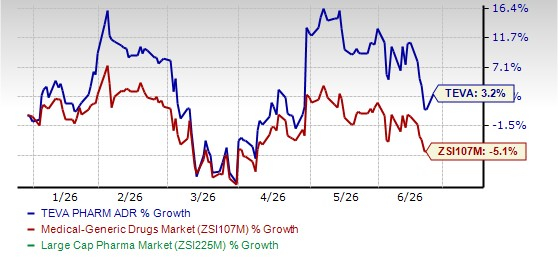

Teva stock has risen 3.2% so far this year against the industry’s 5.1% decrease.

The stock is trading at an attractive valuation relative to the industry. Going by the price/earnings ratio, the company shares currently trade at 11.82 on a forward 12-month basis, lower than 14.52 for the industry. However, the stock is trading above its 5-year mean of 4.65.

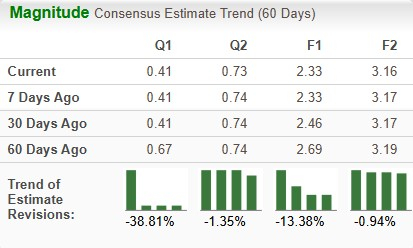

The Zacks Consensus Estimate for earnings has declined from $2.69 per share to $2.33 per share for 2026 over the past 60 days and from $3.19 per share to $3.16 per share for 2027.

TEVA’s Zacks Rank & Stocks to Consider

Teva has a Zacks Rank #3 (Hold).

Some better-ranked stocks in the biotech sector are Indivior Pharmaceuticals INDV and Immunocore IMCR, each currently sporting a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Over the past 60 days, earnings estimates for Indivior Pharmaceuticals have risen from $3.33 per share to $4.05 per share, while those for 2027 have increased from $3.66 per share to $4.27 per share. INDV shares have risen 6.8% year to date.

Indivior Pharmaceuticals’ earnings beat estimates in each of the trailing four quarters, with the average surprise being 65.44%.

Over the past 60 days, estimates for Immunocore’s 2026 bottom line have improved from a loss of 88 cents per share to earnings of 6 cents per share. For 2027, earnings estimates have increased from 24 cents per share to 87 cents per share over the same timeframe. IMCR shares have lost 15.4% year to date.

Immunocore’s earnings beat estimates in three of the trailing four quarters and missed in the remaining one, the average surprise being 46.66%.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Sanofi (SNY): Free Stock Analysis Report

Teva Pharmaceutical Industries Ltd. (TEVA): Free Stock Analysis Report

Immunocore Holdings PLC Sponsored ADR (IMCR): Free Stock Analysis Report

Indivior Pharmaceuticals Inc. (INDV): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).