Vistance Networks, Inc. VISN is gradually emerging as a leading player in the networking infrastructure space following its transformation into a more focused broadband and enterprise networking firm. The company's streamlined portfolio, strengthened balance sheet and exposure to several secular technology trends position it well to capitalize on growing demand for next-generation connectivity solutions.

Let us take a closer look at the key factors driving Vistance's growth.

VISN Buoyed by Broadband Upgrade Cycle

One of the biggest opportunities for Vistance lies in the ongoing modernization of broadband networks. Through its Aurora Networks segment, the company provides critical access-network technologies that enable service providers to deliver faster and more reliable broadband services.

Demand for DOCSIS 4.0 equipment continues to gain momentum as cable operators invest in network upgrades to support higher speeds and increasing data consumption. Aurora has been benefiting from this trend, with strong customer demand for amplifiers, nodes and other access-network solutions. Given that broadband infrastructure upgrades are still in the early innings, Vistance appears well-positioned to benefit from a multi-year investment cycle.

Fiber Expansion, Wi-Fi 7 Traction Lend Support

Global telecom operators and governments continue to accelerate fiber deployments to meet rising bandwidth requirements. Aurora's portfolio includes fiber-access solutions that help service providers expand network reach and improve service quality. The company has already secured several fiber-related wins across international markets, highlighting the growing acceptance of its technology offerings. As fiber adoption continues to expand worldwide, Vistance should see increasing opportunities to capture a larger share of infrastructure spending.

In addition, the enterprise networking market is entering a new upgrade cycle driven by the adoption of Wi-Fi 7 technology. Vistance's Ruckus Networks business is a recognized provider of enterprise-grade wireless networking solutions serving industries such as education, healthcare, hospitality and large public venues.

Wi-Fi 7 delivers significantly improved speed, capacity and performance, making it an attractive upgrade for enterprises looking to support bandwidth-intensive applications, cloud workloads and artificial intelligence initiatives. As organizations modernize their networking infrastructure, Ruckus is expected to benefit from higher demand for wireless access points, switches and related solutions.

Vistance is also benefiting from the industry's shift toward cloud-managed networking. Its RuckusOne platform allows customers to centrally manage and optimize network operations through a cloud-based architecture.

Enhanced Financial Flexibility

Vistance has significantly improved its financial position following its portfolio transformation. The company currently operates with a healthier balance sheet and substantial liquidity, providing management with greater flexibility to invest in innovation, pursue strategic initiatives and return capital to shareholders. A stronger financial foundation also reduces risk and positions the company to navigate industry cycles more effectively.

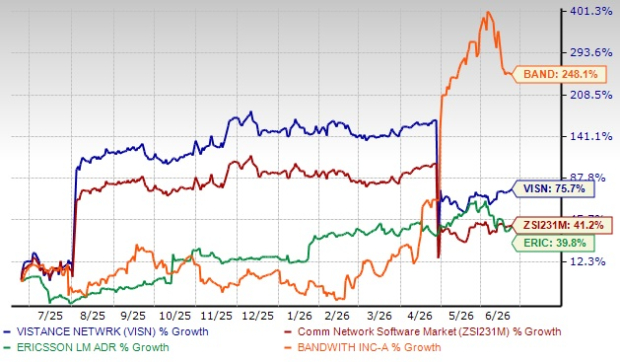

Price Performance

Vistance has surged 75.8% over the past year compared with the industry’s growth of 41.3%. It has outperformed peers like Ericsson ERIC but lagged Bandwidth Inc. BAND. While Ericsson is up 39.8%, Bandwidth soared 248.1% over this period.

One-Year Price Performance of VISN

Image Source: Zacks Investment Research

Moving Forward

Vistance is benefiting from several powerful industry trends, including broadband modernization, fiber deployments, Wi-Fi 7 adoption, cloud-managed networking and AI-driven network intelligence. Continued expansion of recurring software revenue should help support both top-line growth and profitability over time. A stronger balance sheet and improved profitability profile position it favorably for long-term value creation.

The firm delivered a trailing four-quarter average earnings surprise of 76.4%. Vistance currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Riding on a robust earnings surprise history and favorable Zacks Rank, Vistance appears primed for further stock price appreciation. Consequently, investors are likely to profit if they bet on this high-flying stock now.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Ericsson (ERIC): Free Stock Analysis Report

Vistance Networks, Inc. (VISN): Free Stock Analysis Report

Bandwidth Inc. (BAND): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).