FedEx Corporation FDX used its fourth-quarter fiscal 2026 call to press a forward-looking message. The company said premium revenue mix, network changes and structural cost actions are now producing stronger earnings power even as the reporting calendar shifts and FedEx Freight moves out of continuing operations.

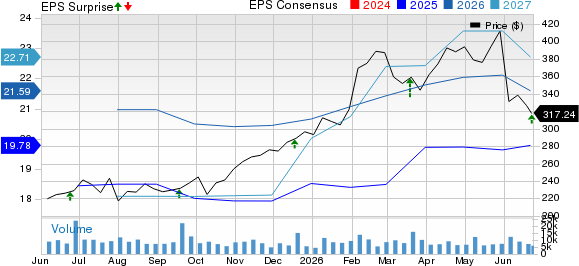

That framing mattered as FedEx posted adjusted earnings per share of $6.31, which beat the Zacks Consensus Estimate of $5.91, delivering a surprise of 6.8%. The company reported revenues of $25.01 billion, surpassing the Zacks Consensus Estimate of $24.18 billion by 3.4%.

FedEx Corporation Price, Consensus and EPS Surprise

FedEx Corporation price-consensus-eps-surprise-chart | FedEx Corporation Quote

FDX Resets the Story Around 2026

President and CEO Rajesh Subramaniam said the central takeaway from the fiscal fourth quarter was momentum, arguing that FedEx is now growing in higher-yielding parts of the market while pulling through transformation savings. He tied that progress to Network 2.0, Tricolor and European improvement efforts.

The company introduced a calendar 2026 outlook for continuing operations that calls for about 11% revenue growth and adjusted EPS of $16.90 to $18.10. Management also said the June-through-December transition period implies roughly 20% adjusted EPS growth year over year.

That guidance is now the lens that management wants investors to use. Claude Russ, enterprise vice president and interim CFO, said the midpoint assumes $5.8 billion of adjusted operating income and reflects continuing demand in premium B2B and high-value B2C services.

FedEx Leans Harder Into Premium Verticals

Chief customer officer Brie Carere described the quarter as further proof that FedEx’s commercial strategy is centered on revenue quality rather than broad volume chasing. She said B2B services drove most of the quarterly revenue growth, with health care, automotive, aerospace, and data center demand standing out.

That emphasis showed up in operating data. Federal Express segment revenues rose 14% in the quarter, with U.S. domestic package revenues up 13% and international export package revenues up 15%, while composite package yield climbed 11%. International domestic volume, however, fell 9% as the company continued to favor higher-yielding cross-border traffic in Europe.

Carere also highlighted nearly $10 billion in health care transportation revenues exiting fiscal 2026 and pointed to double-digit growth tied to AI and data center-related shipments. She presented that business as a broad ecosystem opportunity rather than a narrow vertical.

FDX Says Cost Actions Are Gaining Traction

Subramaniam said FedEx exceeded its fiscal 2026 goal of $1 billion in transformation-related savings, calling that a key proof point behind the quarter. Russ added that structural cost reductions continued to offset higher wage rates, purchased transportation and direct trade-related costs.

The quarter still showed some friction. Consolidated adjusted operating margin was 8.4%, down from 9.1% a year earlier, as fuel expense surged 66% and variable incentive compensation moved higher. Management stressed that fuel surcharge revenues largely offset the profit impact of higher fuel costs.

FedEx also continues to reshape its asset base. Fourth-quarter results included a $23 million impairment tied to the permanent retirement of 10 aircraft, part of a multiyear fleet reduction and modernization strategy meant to better align air capacity with demand.

FedEx Turns Stronger Cash Flow Into Flexibility

Russ used the call to underscore free cash flow as a major part of the equity story. FedEx generated $4.7 billion in adjusted free cash flow in fiscal 2026, while capital spending fell to $3.8 billion, or 4% of revenue, the lowest annual capital intensity in the company’s history.

The balance sheet also shifted with the FedEx Freight separation. Ending cash was $13.3 billion, including a $4.1 billion dividend tied to the spin-off, though management noted that about $800 million of that cash balance reflects IEEPA tariff refunds being held for customers.

Against that backdrop, FedEx said it plans to repurchase up to $1 billion of shares during the rest of calendar 2026 and has already lifted its dividend by 5%, adjusted for the spin-off. Russ said capital allocation will remain balanced as the company also funds pension obligations and strategic investments.

FDX Faces Detailed Questions on Margins and Cadence

Analysts pressed management on why fourth-quarter profit flow-through looked more muted than the transition-year outlook suggests. Russ told Wells Fargo and Bernstein analysts that variable compensation was a large near-term headwind and said seasonality should favor stronger profit concentration in the fourth-quarter results.

Questions also centered on stranded costs after the FedEx Freight separation. Russ said FedEx expects to remove about $100 million of those costs in calendar 2026 and does not expect stranded costs to remain a discussion point beyond the exit rate of 2027.

On the demand side, a Goldman Sachs analyst asked whether B2B strength reflected macro factors or execution in targeted verticals. Carere’s response leaned heavily toward execution, saying the gains were broad across the company’s four key verticals, with AI and data center wins adding to, rather than replacing, wider commercial momentum.

FedEx Leaves the Call Focused on Execution

The closing message from management was notably consistent. Subramaniam returned to the idea that FedEx is becoming more concentrated on premium B2B and high-value B2C traffic while using network and organizational changes to lower the cost to serve.

That posture came through in both prepared remarks and Q&A. Management sounded confident on pricing, network utilization, international share gains and free cash flow, while treating the fiscal-year transition, pilot contract costs and stranded costs as manageable items within a broader earnings expansion story.

Zacks Signals for FDX After the Quarter

FDX carries a Zacks Rank #3 (Hold), along with a Value Score of B, Growth Score of C, Momentum Score of C and VGM Score of B. Under Zacks’ framework, the rank remains the primary signal, while style scores help refine the outlook, with A and B grades generally indicating better expected near-term performance than lower grades.

The Value Score and VGM Score of B suggest relatively stronger broad style characteristics than its Growth and Momentum scores imply, but a Zacks Rank #3 points to a more balanced near-term setup than a top-ranked stock. That rank can also change as earnings estimate revisions adjust after the just-reported results. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

FedEx Corporation (FDX): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).