TD SYNNEX Corporation SNX reported a record second quarter of fiscal 2026, driven by broad-based strength across its Distribution and Hyve Solutions segments, as well as accelerating demand tied to AI infrastructure. Management framed the quarter as a continuation of consistent execution across its global ecosystem.

Executives emphasized that rising complexity in technology spending, particularly around AI build-outs and infrastructure modernization, is reinforcing demand rather than weakening it. The earnings call centered on sustained growth momentum, margin discipline and expanding hyperscaler relationships, which are reshaping the company’s long-term profile.

SNX AI & Hyperscaler Momentum Reframes Growth

Chief executive officer (CEO) Patrick Zammit described AI-driven infrastructure investment as a central growth catalyst, highlighting demand across hyperscale data centers, enterprise modernization and AI-capable devices. He noted that AI-related activity is increasingly embedded across both Distribution and Hyve, expanding addressable demand.

Hyve Solutions was positioned as the most direct beneficiary of hyperscaler expansion. Zammit pointed to multiple program wins across all five U.S.-based hyperscalers, with additional ramps expected in late fiscal 2026 or early fiscal 2027.

Management also highlighted strategic alignment with major vendors, including HPE, which has selected TD SYNNEX as one of only two global distribution partners across networking, cloud and AI portfolios. This positioning reinforces the company’s role in consolidating global channel execution.

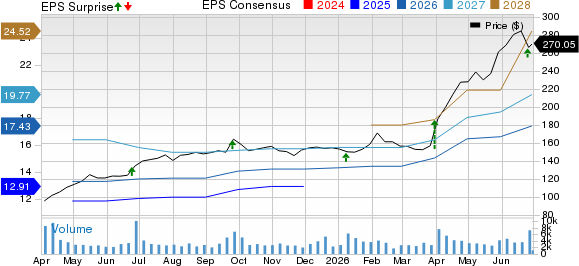

Non-GAAP EPS came in at $4.85, topping the Zacks Consensus Estimate of $4.07 by 19.2%. Revenues were $19.57 billion, beating the $16.84 billion Zacks Consensus Estimate by 16.2%.

TD SYNNEX Corporation Price, Consensus and EPS Surprise

TD SYNNEX Corporation price-consensus-eps-surprise-chart | TD SYNNEX Corporation Quote

SNX Distribution Strength Broadens Across Portfolio

Distribution delivered another strong quarter, with non-GAAP gross billings rising 22% year over year to $23.4 billion, supported by strength across regions and product categories. Management attributed the gains to both portfolio mix and execution in higher-growth technology areas.

CEO Zammit emphasized broad-based demand across endpoints, infrastructure and advanced solutions, noting that AI is increasingly influencing product mix and pricing dynamics. He also pointed to continued strength in SMB and strategic accounts, where share gains are contributing to incremental growth.

Chief financial officer David Jordan added that Distribution margins benefited modestly from strategic inventory positioning, though he characterized these effects as temporary rather than structural. Operating leverage remained a key focus, as earnings growth outpaced billings expansion.

Hyve Capacity Build & Margin Dynamics

Hyve posted gross billings of $5.5 billion, up 117% year over year, reflecting strong hyperscaler demand and new program ramps. Management said manufacturing accounted for roughly two-thirds of the segment, underscoring the shift toward large-scale infrastructure builds.

The company is expanding manufacturing capacity by more than 1 million square feet in the United States to support anticipated demand ramps. Zammit stressed that investments are being made ahead of customer deployments rather than based on speculative demand assumptions.

Margins in Hyve declined year over year due to mix effects, particularly from accelerated manufacturing and supply-chain variability across programs. Jordan noted that margins can vary by workload, with AI server builds carrying different profitability profiles than networking or storage systems.

SNX Inventory Strategy & Pricing Pass Through

Management detailed a proactive inventory strategy designed to support supply assurance amid tightening component markets. Jordan said that inventory levels rose as TD SYNNEX positioned itself ahead of price increases and supply constraints, particularly in memory and CPU components.

Zammit added that strategic inventory positioning helped smooth pricing impacts for customers while supporting vendor relationships. He emphasized that the company’s cost-plus model allows price increases to be passed through, preserving structural margin integrity.

However, management acknowledged that some inventory-related margin benefits are expected to fade over time. The focus remains on maintaining balance between working capital efficiency and supply chain stability rather than optimizing short-term gains.

SNX Analyst Focuses on Supply & Demand Risks

Analysts focused heavily on whether rising component costs could suppress demand or alter purchasing behavior. Zammit responded that no meaningful demand destruction has been observed, even as price increases begin to flow through the channel.

Questions from Bank of America and other firms centered on PC elasticity and supply constraints. Management acknowledged that PCs are the most sensitive category but noted that enterprise refresh cycles and B2B demand continue to offset pricing pressure.

Supply availability, particularly in memory and CPUs, was identified as a potential risk in the second half. However, executives indicated that Hyve customers are generally well-positioned, driven by secured supply agreements with vendors.

SNX Outlook Points to Continued Expansion

For the third quarter of fiscal 2026, TD SYNNEX expects non-GAAP gross billings of approximately $27.7 billion at the midpoint, with revenues of about $18.6 billion and non-GAAP EPS of $4.50. Management noted that Hyve's contributions from newly onboarded customers are expected to ramp later in fiscal 2026 or early fiscal 2027.

Jordan highlighted that operating leverage remains a central objective, with earnings expected to continue growing faster than top-line billings over time. Cash flow remains temporarily pressured due to working capital investments tied to Hyve's expansion.

Overall guidance assumptions reflect continued demand strength in AI-related infrastructure, stable enterprise IT spending and manageable supply constraints across key hardware categories.

SNX Strategic Execution & Capital Deployment Focus

Management’s overarching message centered on disciplined execution while scaling into AI-driven demand cycles. Zammit emphasized that both Distribution and Hyve are positioned to capture structural growth trends rather than cyclical spikes.

Capital allocation remains focused on capacity expansion, working capital efficiency and shareholder returns through dividends and buybacks. Executives stressed that investments are tied to committed programs, particularly those involving hyperscaler relationships.

The tone throughout the call reflected confidence in demand durability, balanced by caution around supply volatility and execution complexity as Hyve scales rapidly across global infrastructure programs.

SNX’s Zacks Rank & Style Scores Signals

TD SYNNEX currently carries a Zacks Rank #1 (Strong Buy), reflecting the most favorable tier of the Zacks ranking system, which prioritizes positive earnings estimate revisions. The framework highlights the importance of analyst sentiment shifts in driving near-term stock performance. You can see the complete list of today’s Zacks #1 Rank stocks here.

The stock also holds a Value Score of B, a Growth Score of F, a Momentum Score of A and a VGM Score of C. According to the Zacks Style Scores methodology, stronger combinations of Value, Growth, and Momentum characteristics tend to support more favorable risk-adjusted performance over time.

While the Zacks Rank reflects current estimate revision trends following the quarter, it may change as analysts reassess forward expectations in response to updated guidance and evolving industry conditions.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

TD SYNNEX Corporation (SNX): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).