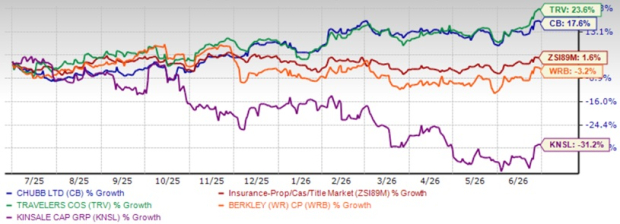

Shares of Chubb Limited CB have gained 17.6% in the past year, outperforming the industry’s growth of 1.6%. Its share price closed at $340.74 on Tuesday, near its 52-week high of $345.67, reflecting strong investor confidence.

Chubb's strong underwriting performance, growing investment income and disciplined capital management position the stock for further price appreciation. While its premium valuation may limit multiple expansion, its solid fundamentals should continue to support long-term gains. CB has surpassed earnings estimates in each of the last four quarters, the average being 12.4%.

Shares of some of its peers, like The Travelers Companies, Inc. TRV, have gained 23.6%, whereas W.R. Berkley Corporation WRB and Kinsale Capital Group, Inc. KNSL have lost 3.2% and 31.2%, respectively, in the past year.

1- Year Price Performance: CB, TRV, WRB, KNSL & Industry

Image Source: Zacks Investment Research

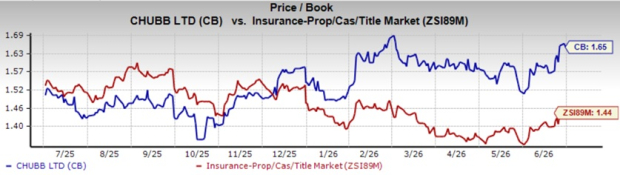

CB’s Premium Valuation

Shares of Chubb Limited are trading at a premium compared with the industry. Its trailing 12-month price-to-book value of 1.65X is higher than the industry average of 1.44X, reflecting investor confidence. However, it currently carries a Value Score of B.

Image Source: Zacks Investment Research

Shares of other insurers like TRV, WRB, and KNSL are trading at a multiple higher than the industry average.

CB’s Growth Projection Encourages

The Zacks Consensus Estimate for Chubb Limited’s 2026 EPS indicates a year-over-year increase of 8.1%. The consensus estimate for revenues is pegged at $64.40 billion, implying a year-over-year improvement of 7.4%.

The consensus estimate for 2027 earnings per share and revenues indicates an increase of 7.7% and 4.9%, respectively, from the corresponding 2026 estimates.

Optimist Analyst Sentiment on CB

Three analysts covering the stock have raised estimates for 2026 and 2027, with no downward revisions over the past 60 days. Thus, the Zacks Consensus Estimate for 2026 and 2027 earnings have moved up 0.4% and 0.7%, respectively, in the same time frame.

CB’s Favorable Return on Capital

Return on equity in the trailing 12 months was 12%, better than the industry average of 6%. Return on equity, a profitability measure, reflects how effectively a company is utilizing its shareholders’ equity.

Return on Invested Capital in the trailing 12 months was 9.5%, better than the industry average of 5.7%, which reflects CB’s efficiency in utilizing funds to generate income

Factors Benefiting CB Stock

Chubb remains focused on capitalizing on the potential of middle-market businesses (both domestic and international), while maintaining disciplined underwriting. The company prioritizes profitability over premium growth by exiting inadequately priced business, particularly in large-account property insurance. Continued investments in AI, digital capabilities, and distribution, along with strong broker relationships, drive new business growth and improve renewal rates.

Chubb continues to benefit from broad-based premium growth across its businesses. In the first quarter of 2026, total net premiums written increased 10.7%, driven by solid growth in P&C insurance, Overseas General and Consumer Insurance. Strong momentum across Europe, Asia and Latin America, along with continued expansion in Worksite Benefits and Life Insurance, and growing demand for specialty and cyber insurance, supports premium growth and strengthens Chubb's long-term growth profile.

CB pursues strategic mergers and acquisitions to diversify its portfolio, add capabilities and synergies, and expand its geographic footprint. The company acquired Liberty Mutual's insurance business in Thailand in April 2025 and is expected to complete the acquisition of Liberty Mutual Vietnam in early 2026. These acquisitions have strengthened Chubb's presence in Southeast Asia and contributed to premium revenue growth.

Higher investment income remains a key earnings driver for Chubb, supported by a growing invested asset base, higher portfolio yields and favorable private equity returns. Chubb Limited expects adjusted net investment income to be between $1.825 billion and $1.85 billion in the second quarter of 2026.

Chubb has a strong capital position and sufficient cash-generation capabilities, with an operating cash flow of $3.9 billion as of March 31, 2026, which supports wealth distribution to shareholders and growth initiatives. The company recently increased its dividend by 5.2%, marking its 33rd consecutive annual increase. The dividend yield of 1.2%, higher than the industry average of 0.3%, Chubb remains an attractive choice for income-focused investors.

Risks for CB

Being a P&C insurer, CB is exposed to catastrophe events, which induce volatility in underwriting profitability and affect the combined ratio. Given the uncertainty surrounding the magnitude of cat loss, higher losses could drain earnings.

Softening commercial insurance pricing remains a headwind for Chubb, as continued rate declines could weigh on premium growth and profitability.

Conclusion

Chubb Limited’s market-leading position, disciplined underwriting, broad-based premium growth, higher investment income, strong capital position and capital returns pave the way for long-term growth. Favorable estimates, optimistic analyst sentiment and higher ROE are other positives. A VGM Score of B instills confidence.

However, given its premium valuation, catastrophe losses and softer commercial pricing remain risks. We prefer to stay cautious on this Zacks Rank #3 (Hold) stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Chubb Limited (CB): Free Stock Analysis Report

The Travelers Companies, Inc. (TRV): Free Stock Analysis Report

W.R. Berkley Corporation (WRB): Free Stock Analysis Report

Kinsale Capital Group, Inc. (KNSL): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).