Zscaler, Inc. ZS is facing rising infrastructure costs as demand for artificial intelligence (AI)-powered cybersecurity services increases. Higher prices for memory, storage and processors are expected to raise spending on data center equipment and Zero Trust Branch appliances. However, the company believes its growing scale, pricing actions and operational discipline can help offset these cost pressures over time.

Management expects capital expenditures to reach the high single digits as a percentage of revenues in fiscal 2026 compared with its earlier expectation of the mid-single digits. It also anticipates fiscal 2027 capital expenditures as a percentage of revenues to rise by as much as 200 basis points from the 2026 level because of higher hardware costs. To reduce the impact, Zscaler has already increased prices for its branch appliances and is purchasing equipment early to lock in current prices.

Despite these near-term challenges, the company continues to deliver strong financial performance. In the third quarter of fiscal 2026, revenues increased 25% year over year to $850 million, while annual recurring revenues exceeded $3.5 billion. Remaining performance obligations reached roughly $6.5 billion, providing strong visibility into future revenues.

Profitability also remains healthy. Zscaler’s third-quarter non-GAAP gross margin expanded 40 basis points year over year to 80.7%, while non-GAAP operating margin increased by 140 basis points to 23%. Year to date, the company generated a free cash flow margin of 29%, highlighting its ability to fund growth while maintaining financial discipline.

As its customer base expands and long-term contracts grow, Zscaler's larger revenue scale should help absorb higher infrastructure costs. Continued demand for AI security and Zero Trust solutions could further strengthen its operating leverage over the long run. The Zacks Consensus Estimate for fiscal 2026 is currently pegged at $3.33 billion, indicating a year-over-year increase of approximately 25%.

How Are ZS’ Rivals Managing Rising Infrastructure Costs?

Zscaler’s major competitors, including Palo Alto Networks, Inc. PANW and CrowdStrike Holdings, Inc. CRWD, are also investing heavily in AI infrastructure to strengthen their cybersecurity capabilities.

Palo Alto Networks is investing heavily in AI, cloud security and platform integration while using its large scale to protect margins. In the third quarter of fiscal 2026, revenues increased 31% year over year to $3 billion, and next-generation security ARR surpassed $8 billion. Palo Alto Networks continues to consolidate multiple security products into one platform, helping spread infrastructure costs across a larger customer base and supporting long-term profitability.

CrowdStrike is also expanding AI-powered capabilities while keeping profitability strong. In the first quarter of fiscal 2027, revenues rose 26% year over year to approximately $1.39 billion, while annual recurring revenues reached about $5.51 billion, up 24%. Its cloud-native Falcon platform reduces the need for on-premise hardware, allowing the company to scale efficiently even as AI workloads increase.

Zscaler’s Price Performance, Valuation & Estimates

ZS shares have plunged 33.5% year to date against the Zacks Security industry’s surge of 72.3%.

Zscaler YTD Price Return Performance

Image Source: Zacks Investment Research

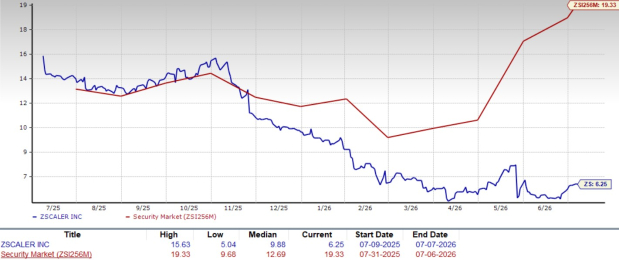

From a valuation standpoint, ZS trades at a forward price-to-sales ratio of 6.25, significantly below the industry’s average of 19.33.

Zscaler Forward 12-Month P/S Ratio

Image Source: Zacks Investment Research

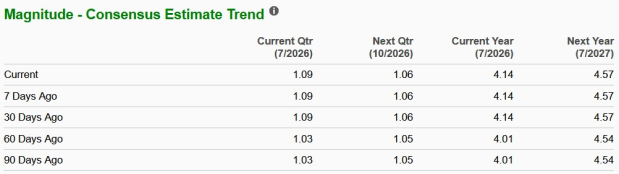

The Zacks Consensus Estimate for Zscaler’s fiscal 2026 and 2027 earnings implies year-over-year increases of 26.2% and 10.6%, respectively. Estimates for fiscal 2026 and 2027 have been revised upward over the past 60 days.

Image Source: Zacks Investment Research

Zscaler currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Zscaler, Inc. (ZS): Free Stock Analysis Report

Palo Alto Networks, Inc. (PANW): Free Stock Analysis Report

CrowdStrike (CRWD): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).