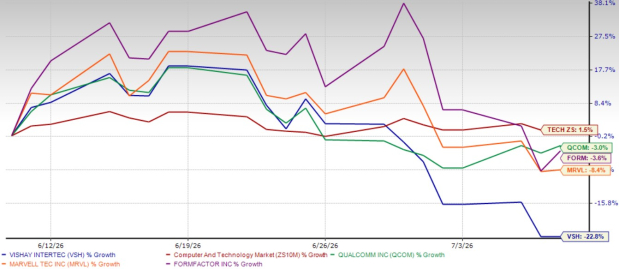

Vishay Intertechnology, Inc. VSH stock has come under intense selling pressure, declining 22.8% over the past month and significantly underperforming the broader Zacks Computer and Technology sector, which has gained 1.5% during the same period.

The weakness has not been limited to Vishay Intertechnology. Several leading semiconductor stocks, including Qualcomm Incorporated QCOM, FormFactor Inc. FORM and Marvell Technology, Inc. MRVL, have also lost ground. Over the past month, shares of Qualcomm, FormFactor and Marvell Technology have fallen 3%, 3.6% and 8.4%, respectively.

Vishay Intertechnology One-Month Price Return Performance

Image Source: Zacks Investment Research

VSH stock’s recent sell-off has been driven by three major reasons.

Firstly, investors have turned cautious on semiconductor stocks amid concerns that the massive artificial intelligence (AI) spending by hyperscalers may not generate returns quickly enough to justify current investment levels.

Secondly, many chip stocks surged sharply during early 2026, pushing valuations to elevated levels and encouraging institutional investors to lock in profits. Despite the recent sell-off, Vishay Intertechnology currently trades at a forward 12-month price-to-earnings (P/E) multiple of 36.35, a significant premium to the sector’s average of 24.56.

Vishay Intertechnology Forward 12-Month Price-To-Earnings Ratio

Image Source: Zacks Investment Research

Compared with other semiconductor peers, Vishay Intertechnology trades at a premium to QUALCOMM, while at a lower multiple than FormFactor and Marvell Technology. At present, Qualcomm, FormFactor and Marvell Technology trade at P/E multiples of 16.77, 42.23 and 46.42, respectively.

Thirdly, Vishay Intertechnology faced company-specific pressure after announcing on July 7, 2026 that its 2.25% convertible senior notes due 2030 had become convertible, raising concerns about potential future share dilution. Following the news, shares of the company fell 9.4% in a single day.

While these issues have weighed heavily on sentiment, they appear to overshadow a business that is showing improving fundamentals. With demand strengthening across several end markets and management executing its long-term strategy successfully, the recent decline could offer investors an attractive buying opportunity.

Vishay Intertechnology 3.0 Strategy Is Delivering Results

The company's multi-year Vishay 3.0 transformation is now translating into stronger operating performance. The strategy focuses on expanding manufacturing capacity, broadening the product portfolio, improving customer engagement and increasing technical support, enabling Vishay Intertechnology to capture more business across growing markets.

The benefits became visible in the first quarter of 2026. Revenues increased 17.3% year over year to $839.2 million, exceeding management's guidance. Growth was broad-based across every end market, every sales channel and all three major geographic regions. Volume increased 5.8%, supported by stronger customer demand, inventory replenishment and continued market-share gains.

Vishay Intertechnology also reported a healthy book-to-bill ratio of 1.34, including 1.47 for semiconductors, while the backlog expanded 21% to $1.6 billion, representing 5.7 months of sales visibility. These numbers indicate that demand continues to outpace shipments, providing a favorable setup for future revenue growth.

VSH’s Multiple Market Exposure Offers Several Growth Drivers

Unlike many semiconductor companies that rely heavily on a single end market, Vishay Intertechnology benefits from exposure to several fast-growing industries.

AI-related demand remains one of the strongest growth engines. The company continues receiving orders for high-voltage MOSFETs, polymer capacitors, current-sense resistors and magnetics used in AI servers, networking equipment and power management systems. Management expects AI-related revenues in 2026 to be well above last year's level, helped by expanding customer relationships and additional design wins.

Industrial demand is also improving rapidly. Customers are increasing spending on renewable energy, smart grids, factory automation, power transmission and AI infrastructure. Industrial revenues have now posted five consecutive quarters of sequential growth, supported by improving customer inventories and stronger capital spending. In the first quarter of 2026, revenues from the industrial segment increased 7% sequentially and 22% year over year.

Automotive remains another attractive opportunity. Rising electronic content in hybrid and electric vehicles continues to increase semiconductor demand. Vishay has become the leading resistor supplier for several next-generation EV platforms while also expanding design wins in battery management, ADAS, electronic power steering and powertrain systems. First-quarter revenues from the automotive segment increased 3% sequentially and 11% year over year.

The aerospace and defense segment is emerging as another meaningful growth driver as higher government defense spending supports increasing orders for resistors, capacitors and custom magnetics. In the first quarter, revenues from the aerospace and defense segment increased 14% sequentially and 17% year over year. Healthcare demand also remains healthy, supported by wearable devices, patient monitoring and implantable medical technologies. First-quarter revenues from the healthcare segment increased 5% sequentially and 11% year over year.

Capacity Investments Position VSH for the Next Upcycle

Vishay Intertechnology has spent heavily over the past several years to prepare for stronger industry demand. Capacity expansion projects include its new 12-inch semiconductor fabrication facility in Germany, additional production at Newport, RI, silicon carbide investments and expanded subcontractor partnerships.

Although these investments have temporarily pressured free cash flow, they position Vishay Intertechnology to respond faster than competitors as industry demand strengthens. Management expects the German fab to begin non-automotive production during mid-2027, while new silicon carbide products continue entering production to address fast-growing power semiconductor markets.

Importantly, management believes the current industry recovery is arriving just as these investments become operational, creating an opportunity for both higher revenues and expanding margins over the coming years.

Vishay Intertechnology’s Profitability to Continue Improving

While VSH continues investing aggressively in capacity expansion, profitability is already improving. First-quarter 2026 gross margin expanded to 21% from 19% a year ago as higher shipment volumes offset ongoing material cost inflation. EBITDA margin improved to 9.3% from 7.6% in the year-ago quarter, while GAAP earnings returned to profitability at 5 cents per share from the year-ago quarter’s loss of 3 cents.

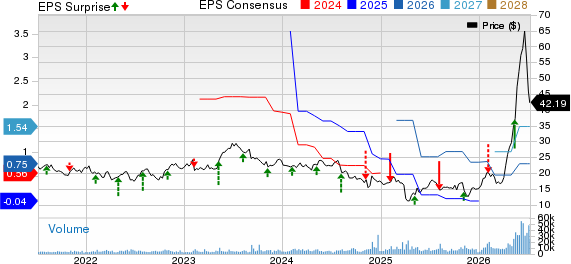

Vishay Intertechnology, Inc. Price, Consensus and EPS Surprise

Vishay Intertechnology, Inc. price-consensus-eps-surprise-chart | Vishay Intertechnology, Inc. Quote

Management expects further improvement during the second quarter, guiding for revenues between $875 million and $905 million and gross margin around 22%. Pricing actions implemented earlier this year should gradually offset higher metal costs, while increasing factory utilization is expected to provide additional operating leverage.

The Zacks Consensus Estimate for 2026 and 2027 revenues indicates year-over-year growth of 16.7% and 10.4%, respectively. The consensus mark for 2026 earnings per share is currently pegged at 75 cents, calling for a robust improvement from a loss of 5 cents in 2025. Earnings estimates of $1.54 per share for 2027 indicate a 104.9% year-over-year increase.

Buy-the-Dip Strategy Looks Good for VSH Stock

The recent sell-off appears to reflect short-term market fears rather than weakening business fundamentals. Concerns surrounding AI spending, profit-taking across semiconductor stocks and temporary dilution worries have overshadowed a business that is showing stronger demand, rising backlog, expanding margins and improving market share.

While near-term volatility may continue, Vishay Intertechnology appears well-positioned to benefit from the next semiconductor upcycle due to its expanded manufacturing capacity, diversified end-market exposure and improving execution under the Vishay 3.0 strategy.

Although the stock still trades at a premium valuation, that premium appears justified, given its consistent earnings growth and long-term prospects. For investors willing to look beyond current market sentiment, the recent pullback appears to present an attractive opportunity to buy a fundamentally strengthening semiconductor company.

Vishay Intertechnology sports a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Vishay Intertechnology, Inc. (VSH): Free Stock Analysis Report

QUALCOMM Incorporated (QCOM): Free Stock Analysis Report

FormFactor, Inc. (FORM): Free Stock Analysis Report

Marvell Technology, Inc. (MRVL): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).