Cytokinetics, Incorporated CYTK has entered a pivotal phase following the FDA approval of its first drug, Myqorzo (aficamten), for the treatment of symptomatic obstructive hypertrophic cardiomyopathy (oHCM).

The approval marks the company’s transition into a commercial-stage biotech.

Myqorzo is an allosteric and reversible inhibitor of cardiac myosin motor activity. It is approved in the United States and China for the treatment of adults with symptomatic oHCM.

The commercial outlook for Myqorzo appears promising. The company initiated the U.S. commercial rollout in January 2026. Early launch metrics indicate strong physician engagement and patient uptake, with over 275 unique healthcare providers prescribing the drug and approximately 680 patients being prescribed Myqorzo by the end of the first quarter.

More than 70% of patients on therapy transitioned to paid prescriptions.

International expansion provides an additional growth lever. The European Commission approval in February 2026 further expands Myqorzo's addressable market.

Cytokinetics recently achieved an important commercial milestone with the first European launch of Myqorzo in Germany, marking the drug's entry into the EU market.

CYTK is also working on a label expansion of Myqorzo. The FDA accepted its supplemental new drug application for MAPLE-HCM, a phase III study of aficamten as monotherapy compared with metoprolol as monotherapy in patients with oHCM. The regulatory body assigned a target action date of Nov. 14, 2026.

Meanwhile, aficamten continues to be evaluated across additional patient populations, supporting potential lifecycle expansion opportunities. The drug was studied in the phase III ACACIA-HCM study in non-obstructive hypertrophic cardiomyopathy (nHCM).

The ACACIA-HCM study successfully met both co-primary endpoints, demonstrating statistically significant improvements from baseline through week 36 in both Kansas City Cardiomyopathy Questionnaire (KCCQ) Clinical Summary Score and maximal exercise performance (peak VO2). Statistically significant improvements compared to placebo were also observed in key secondary endpoints.

The company’s tailored commercialization model, including dedicated cardiac account specialists and patient support programs, may further drive uptake.

Competition for CYTK’s Myqorzo

Myqorzo operates within an evolving treatment landscape for oHCM. Its primary branded competitor is Camzyos, a cardiac myosin inhibitor marketed by Bristol Myers Squibb BMY. In addition to this direct competition, Myqorzo faces established generic therapies, namely beta blockers and calcium channel blockers, which continue to serve as the first-line standard of care.

BMY obtained FDA approval for Camzyos in 2022 for the treatment of adults with symptomatic New York Heart Association class II-III obstructive HCM to improve functional capacity and symptoms.

The drug continues to gain traction in the targeted market, supported by growing demand and increased adoption among eligible patients

The FDA accepted BMY’s supplemental new drug application seeking approval of Camzyos for the treatment of adolescentsaged 12 to under 18 years with symptomatic oHCM.

A potential competitor for Cytokinetics is Edgewise Therapeutics, Inc. EWTX, whose cardiovascular program includes novel, oral, selective cardiac sarcomere modulators — EDG-7500 and EDG-15400.

Edgewise recently reported top-line results from the 12-week phase II Part D CIRRUS-HCM study of EDG-7500 in oHCM and nHCM. Consistent and clinically meaningful improvements were observed in echocardiogram parameters, biomarkers, symptoms and functional status across obstructive and nonobstructive HCM.

EWTX expects to initiate a phase II study on EDG-15400 in participants with heart failure with preserved ejection fraction in the second half of 2026.

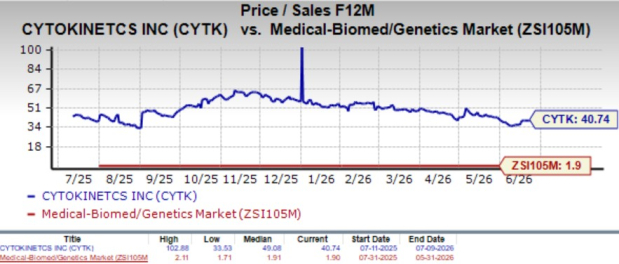

CYTK’s Price Movement, Valuation and Estimates

Cytokinetics’ shares have gained 35.5% year to date compared with the industry’s 6.3% growth.

Image Source: Zacks Investment Research

Going by the price/sales ratio, CYTK’s shares currently trade at 40.74X forward sales, higher than the industry’s average of 1.90X but lower than its mean of 49.04X.

Image Source: Zacks Investment Research

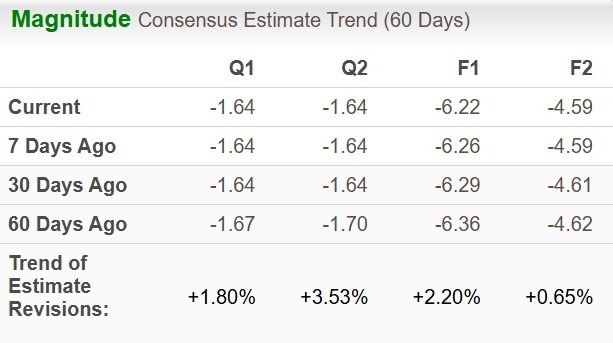

The Zacks Consensus Estimate for 2026 loss per share has narrowed to $6.22 from $6.36 and that for 2027 has narrowed to $4.59 from $4.62 in the past 60 days.

Image Source: Zacks Investment Research

CYTK currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Cytokinetics, Incorporated (CYTK): Free Stock Analysis Report

Bristol Myers Squibb Company (BMY): Free Stock Analysis Report

Edgewise Therapeutics, Inc. (EWTX): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).