Despite the macroeconomic uncertainties, technology stocks have witnessed an impressive rally so far this year as investors continue pouring money into companies benefiting from artificial intelligence (AI), cloud computing and digital transformation. While many of the biggest gainers now trade at premium valuations, a handful of companies stand out for a different reason. Their stocks have rallied sharply, yet their earnings multiples remain well below the technology sector average.

A strong rally alone does not necessarily mean a stock has become expensive. If profits are growing faster than the share price, valuation can remain attractive. That is exactly what investors should look for when searching for the next leg of upside. Companies that combine accelerating earnings, industry tailwinds and reasonable valuations often outperform over longer periods.

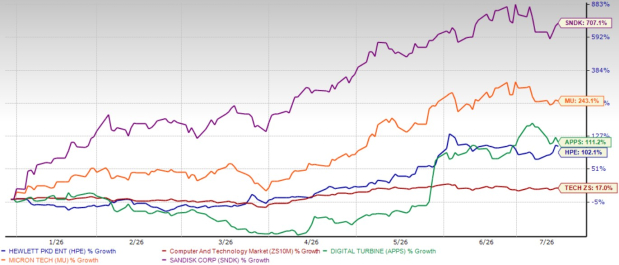

SanDisk Corporation SNDK, Micron Technology, Inc. MU, Digital Turbine, Inc. APPS and Hewlett Packard Enterprise Company HPE are four such names. Their shares have climbed 707.1%, 243.1%, 111.2% and 102.1%, respectively, year to date (YTD) and have outperformed the Zacks Computer and Technology sector’s 17% gain.

YTD Price Return Performance

Image Source: Zacks Investment Research

Even after these eye-catching gains, all four stocks trade at forward 12-month price-to-earnings (P/E) multiples below the sector average of 24.8X, suggesting investors are still paying relatively modest prices for their future earnings.

Although these companies operate in different parts of the technology industry, they are all benefiting from powerful secular trends. SanDisk and Micron are riding on the recovery in memory demand driven by AI infrastructure and enterprise storage. Digital Turbine is capitalizing on improving digital advertising conditions and expanding mobile partnerships. Hewlett Packard Enterprise is benefiting from accelerating AI server demand and enterprise modernization.

If these growth drivers continue playing out, these stocks could have room to extend their remarkable rallies. These stocks have a favorable combination of a VGM Score of A or B and a Zacks Rank #1 (Strong Buy), offering solid investment opportunities.

SanDisk Rides on AI Storage Boom

SanDisk has emerged as one of the biggest winners in the technology sector as demand for high-performance storage continues to accelerate. AI workloads, hyperscale cloud providers and enterprise data centers require increasingly larger amounts of flash storage, creating a favorable backdrop for the company.

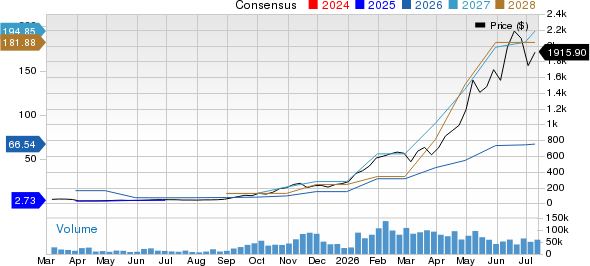

The recovery in NAND pricing has also significantly improved SanDisk's earnings outlook after a prolonged industry downturn. At the same time, disciplined industry supply has helped balance the memory market, supporting healthier pricing trends. In the last reported financial results for the third quarter of fiscal 2026, its revenues jumped 251% year over year to $5.95 billion. The company reported non-GAAP earnings per share (EPS) of $23.41, a robust improvement from the year-ago quarter’s loss of 30 cents.

SanDisk continues introducing advanced SSDs and enterprise storage solutions designed for AI servers, cloud infrastructure and high-performance computing. As AI adoption expands across industries, storage demand is expected to grow alongside computing requirements. Despite the extraordinary stock rally, SanDisk's forward 12-month P/E valuation multiple of 9.85 remains well below the sector and many AI-focused technology companies, leaving room for further upside if earnings continue improving.

The Zacks Consensus Estimate for fiscal 2026 and 2027 earnings indicates a year-over-year increase of 2,125% and 193%, respectively. The consensus mark for both periods’ earnings has been revised upward over the past seven days. Currently, SanDisk sports a Zacks Rank of 1 and has a VGM Score of B. You can see the complete list of today’s Zacks #1 Rank stocks here.

Sandisk Corporation Price and Consensus

Sandisk Corporation price-consensus-chart | Sandisk Corporation Quote

Micron Benefits From AI Memory Demand

Micron remains one of the clearest beneficiaries of the AI infrastructure boom. Every AI server requires significantly more high-bandwidth memory (HBM) and advanced DRAM than traditional computing systems, creating a powerful demand driver for Micron's products.

The company has established itself as an important supplier of HBM used in AI accelerators, while demand for DRAM and NAND continues improving across cloud, enterprise and consumer markets. Capacity remains tight across several advanced memory products, allowing healthier pricing and supporting margin expansion. Micron is also benefiting from growing investments by hyperscale cloud companies that continue expanding AI data-center infrastructure.

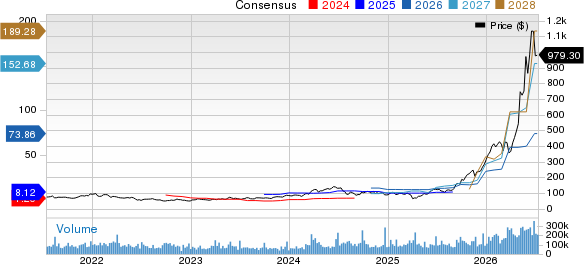

In the most recently reported financial results for the third quarter of fiscal 2026, revenues soared 346% year over year to $41.46 billion, while non-GAAP EPS jumped to $25.11 from $1.91 reported in the year-ago quarter. Although Micron shares have more than tripled this year, its earnings growth outlook remains exceptionally strong, making its forward 12-month P/E valuation multiple of 6.90 appear attractive relative to the sector as well as many semiconductor peers.

The Zacks Consensus Estimate for fiscal 2026 and 2027 earnings indicates a year-over-year increase of 791% and 107%, respectively. The consensus mark for fiscal 2026 and 2027 earnings has been revised upward over the past 30 days. Currently, Micron sports a Zacks Rank of 1 and has a VGM Score of B.

Micron Technology, Inc. Price and Consensus

Micron Technology, Inc. price-consensus-chart | Micron Technology, Inc. Quote

Digital Turbine Executes a Strong Turnaround

Digital Turbine has staged a remarkable recovery by improving operational efficiency while benefiting from healthier mobile advertising demand. The company's platform helps mobile operators, smartphone manufacturers and app developers connect users with applications through on-device discovery and digital advertising.

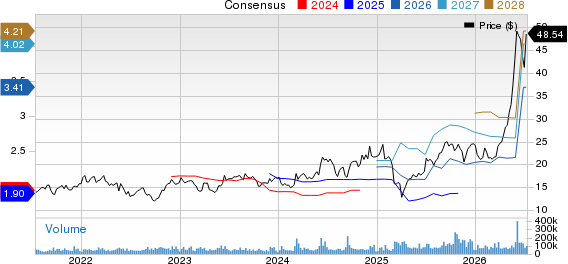

As advertising budgets stabilize and mobile engagement remains strong, Digital Turbine is seeing improving business momentum. In the last reported financial results for the fourth quarter of fiscal 2026, Digital Turbine’s revenues rose 20% year over year to $142.5 million. Management has also taken meaningful steps to simplify operations, reduce expenses and improve margins. Those initiatives are translating into healthier profits. In the fourth quarter, non-GAAP EPS jumped 60% year over year to 16 cents.

Digital Turbine's AI-powered first-party data strategy has become a core pillar of its long-term growth. Management identified AI and data as the primary drivers of future double-digit growth, noting that improved AI targeting has already increased advertiser outcomes, with AGP pricing rising about 40% year over year in the fiscal fourth quarter of 2026, as advertisers paid more for superior returns.

Digital Turbine also continues expanding relationships with wireless carriers and original equipment manufacturers, broadening the reach of its platform. As advertisers increasingly focus on performance-based marketing, Digital Turbine's technology is well-positioned to benefit. Even after its impressive YTD gain, the stock trades at a forward 12-month P/E valuation multiple of 11.71, significantly below the sector’s average and many fast-growing technology peers.

The Zacks Consensus Estimate for fiscal 2027 earnings indicates a 50% year-over-year increase. The consensus mark for fiscal 2027 earnings has been revised upward over the past 60 days. Currently, Digital Turbine sports a Zacks Rank of 1 and has a VGM Score of A.

Digital Turbine, Inc. Price and Consensus

Digital Turbine, Inc. price-consensus-chart | Digital Turbine, Inc. Quote

HPE Builds an AI Infrastructure Business

Hewlett Packard Enterprise has transformed itself into an increasingly important player in enterprise AI infrastructure. Demand for AI-optimized servers, networking equipment and storage solutions continues to rise as businesses modernize their technology environments.

Hewlett Packard Enterprise's AI systems business has been supported by robust enterprise and cloud customer spending. Its GreenLake platform is also gaining traction by allowing customers to consume computing infrastructure through a flexible, subscription-like model, creating more predictable recurring revenues. In the last reported financial results for the second quarter of fiscal 2026, its revenues soared 40% year over year to $10.7 billion, while non-GAAP EPS jumped 108% to 79 cents.

Hewlett Packard Enterprise is strengthening its competitive position through continued investments in networking, hybrid cloud and high-performance computing. As organizations deploy larger AI workloads, demand for integrated infrastructure solutions is expected to remain strong.

Despite more than doubling this year, HPE's forward 12-month P/E multiple of 12.65 remains below the broader technology sector average, reflecting a valuation that still appears attractive given its improving growth outlook.

The Zacks Consensus Estimate for fiscal 2026 earnings indicates a year-over-year increase of 76%. The consensus mark for fiscal 2026 earnings has remained unchanged over the past 60 days. Currently, Hewlett Packard Enterprise sports a Zacks Rank of 1 and has a VGM Score of B.

Hewlett Packard Enterprise Company Price and Consensus

Hewlett Packard Enterprise Company price-consensus-chart | Hewlett Packard Enterprise Company Quote

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Micron Technology, Inc. (MU): Free Stock Analysis Report

Sandisk Corporation (SNDK): Free Stock Analysis Report

Hewlett Packard Enterprise Company (HPE): Free Stock Analysis Report

Digital Turbine, Inc. (APPS): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).