Helen of Troy Limited HELE presents a mixed case for investors weighing valuation against operating risk. The stock trades at a compressed earnings multiple, while the business is showing early signs of sales stabilization.

The debate is whether improving sales trends and debt reduction are enough to offset cost pressure, margin compression and uncertain second-half demand. That makes HELE more complicated than a bargain-stock screen.

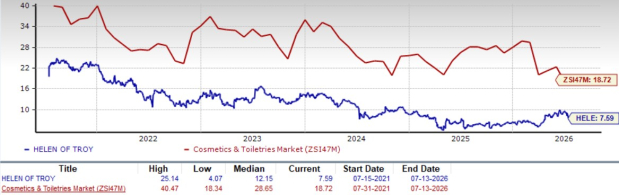

HELE Looks Cheap on Forward Earnings

HELE trades at 7.59X forward 12-month earnings. That is below 18.72X for the Zacks sub-industry, 16.96X for the Zacks sector and 21.23X for the S&P 500 index.

Image Source: Zacks Investment Research

The discount may attract value-oriented investors because it also sits below Helen of Troy’s five-year median of 12.15X. A lower-than-normal multiple can leave room for rerating if earnings visibility improves, but valuation alone does not prove the stock is mispriced.

Newell Brands NWL is a relevant comparison for investors studying branded consumer-products companies. Its portfolio includes household and consumer brands, making cost control, retailer demand and brand investment central to its investment narrative.

Helen of Troy Has Better Sales Signals

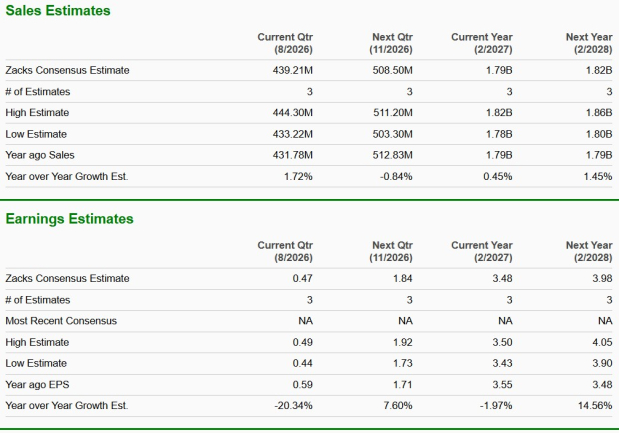

Helen of Troy’s valuation discount is not simply tied to collapsing demand. In the first quarter of fiscal 2027, net sales rose 8.2% to $402.1 million and topped the Zacks Consensus Estimate of $375 million.

The company also raised its fiscal 2027 net sales outlook to $1.759-$1.831 billion from $1.751-$1.822 billion. Home & Outdoor sales increased 9.5%, helped by international demand for packs, new product launches and expanded distribution. Beauty & Wellness sales rose 7%, led by nail care, fans and thermometers.

These figures suggest that brand momentum has improved more than the headline valuation implies. Growth across both operating segments gives investors a reason to look beyond the low multiple.

HELE Earnings Risks Still Matter

The low multiple does not automatically create upside because earnings quality remains uneven. Adjusted earnings were 17 cents per share in the fiscal first quarter, above the Zacks Consensus Estimate of 2 cents, but down from 41 cents a year earlier.

That decline came despite higher sales. Gross margin fell 110 basis points to 46%, while adjusted operating margin declined 30 basis points to 4%. Tariffs, freight, sourcing costs, inflation, inventory obsolescence and unfavorable mix are the central value-trap concerns.

Spectrum Brands Holdings SPB offers another useful consumer-products comparison. Like HELE, it operates in branded household and consumer categories where pricing, distribution and margin discipline can matter as much as sales growth.

Helen of Troy Improves Financial Flexibility

Helen of Troy is making progress on financial flexibility. The sale of its Southaven distribution facility generated $78.2 million in net proceeds, which were used to reduce borrowings.

Total debt declined to $716.1 million at May 31, 2026, from $780.8 million at fiscal 2026 year-end. Net leverage improved to 3.48X from 3.87X, and management continues to target a net leverage ratio of 3.2X or lower by the end of fiscal 2027.

Working-capital discipline also matters. Inventory declined nearly $17 million year over year to $467.4 million, even with roughly $15 million of incremental tariff-related inventory costs. A cleaner balance sheet gives Helen of Troy more room to invest behind its multi-year plan, though execution still has to follow.

Image Source: Zacks Investment Research

What HELE’s Rank Suggests for Buyers

The bottom line is that HELE looks inexpensive, but it is not a clean value call. Sales momentum and debt reduction are moving in the right direction, while earnings pressure and second-half demand uncertainty keep the case balanced.

The stock currently carries a Zacks Rank #3 (Hold), which fits a company with valuation appeal but limited near-term earnings clarity. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

No Value Score, Growth Score, Momentum Score or VGM Score is cited for HELE. Because Zacks Style Scores are designed to complement the Zacks Rank, investors have less style-based confirmation here and may need to lean more heavily on the Rank when judging whether HELE is undervalued or a value trap.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Helen of Troy Limited (HELE): Free Stock Analysis Report

Newell Brands Inc. (NWL): Free Stock Analysis Report

Spectrum Brands Holdings Inc. (SPB): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).