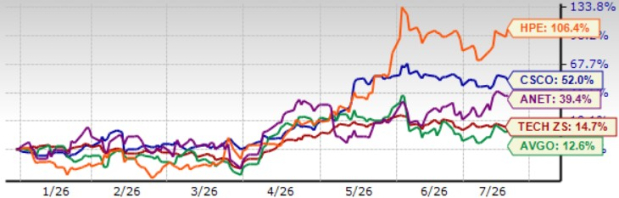

Cisco Systems CSCO shares have jumped 52% year to date (YTD), outperforming the broader Zacks Computer & Technology sector’s return of 14.7%. The company has been benefiting from a strong AI push, a networking supercycle, improving its enterprise networking business and recovering its security business. These factors have helped in improving Cisco’s competitive prowess compared with the likes of Hewlett Packard Enterprise HPE, Broadcom AVGO and Arista Networks ANET, shares of which have appreciated 106.4%, 39.4% and 12.6%, YTD, respectively. Is there room for further upside in Cisco shares? Let’s find out.

CSCO Stock’s Price Performance

Image Source: Zacks Investment Research

AI Push & Strong Networking Growth Aids Cisco’s Prospects

Cisco’s growing AI infrastructure business has been a major growth driver. The company raised its fiscal 2026 AI infrastructure order target from $5 billion to approximately $9 billion, reflecting stronger-than-expected hyperscaler demand. Cisco secured five new hyperscaler AI design wins during the third quarter of fiscal 2026, including Silicon One-powered systems and Acacia optical networking products. This reinforces investor confidence that the AI networking opportunity is expanding beyond a handful of deployments. Cisco now expects to recognize approximately $4 billion in AI infrastructure revenues from hyperscalers in fiscal 2026. The company expects at least $6 billion of AI-related revenues in fiscal 2027, indicating strong visibility into future growth.

Cisco is a key beneficiary of the networking supercycle as hyperscalers, enterprises, sovereign cloud operators, public-sector organizations and telecom providers modernize networks simultaneously to support AI workloads. The company believes this demand is larger and faster than previous technology cycles because AI infrastructure cannot function without modern, high-speed networking. In the third quarter of fiscal 2026, enterprise data center switching orders grew more than 40%, campus networking orders reached record levels (up more than 25%), and wireless orders increased more than 40% year over year.

The Acacia optics business generated more than $1 billion of orders in the third quarter of fiscal 2026 and is expected to grow over 200% in fiscal 2026, positioning Cisco to capture a larger share of AI networking spend. The business has shipped more than 750,000 400G coherent optics and over 40,000 800G coherent optics, giving Cisco leadership in AI optical interconnects. Meanwhile, Silicon One continues winning large hyperscaler deployments, strengthening Cisco's competitive position in AI networking.

The company’s refreshed security portfolio is gaining traction, with double-digit order growth in core security products (excluding Splunk) and strong firewall momentum. Cisco is leveraging its unique position across networking, security, identity and observability to address emerging AI security needs, including agentic AI security, AI Defense, Hypershield and Zero Trust Access. Cisco has also expanded its Secure AI Factory with NVIDIA and announced acquisitions of Galileo and Astrix to strengthen AI identity and agentic security capabilities.

Cisco’s Prospects: Key Catalysts Outweigh Challenges

Cisco’s prospects are likely to benefit from accelerating AI networking demand. Continued expansion of Silicon One, Acacia optics and AI switching is expected to support another leg of growth. A strong pipeline of AI infrastructure buildout ($3 billion roughly) across enterprise, sovereign AI and neocloud customers suggests that AI demand is broadening beyond hyperscalers. Cisco believes campus upgrades remain in the early innings as enterprises migrate to Wi-Fi 7, AI-enabled switching and secure networking.

In terms of the Security business, Cisco expects easier comparisons beginning in fiscal 2027 as Splunk’s cloud transition normalizes. Combined with stronger adoption of Hypershield, AI Defense and Zero Trust, Security could become a faster growth contributor. Strong adoption of agentic AI bodes well for Cisco’s prospects. The company believes that agentic AI requires security to be embedded directly into networking infrastructure, an area where Cisco has a competitive advantage over pure networking or standalone cybersecurity vendors.

These positive drivers are expected to help Cisco comfortably navigate challenges related to higher memory prices, Splunk’s cloud transition, stiff competition and heightened AI-related spending.

2026 Earnings Estimate Revisions Positive for CSCO

The Zacks Consensus Estimate for CSCO’s fiscal 2026 earnings is currently pegged at $4.28 per share, up 0.9% over the past 60 days, indicating year-over-year growth of 12.3%.

Cisco Systems, Inc. Price and Consensus

Cisco Systems, Inc. price-consensus-chart | Cisco Systems, Inc. Quote

The consensus mark for CSCO’s fourth-quarter fiscal 2026 earnings is currently pegged at $1.17 per share, up a penny over the past 60 days, indicating year-over-year growth of 18.2%.

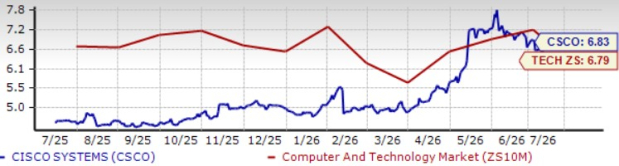

CSCO Shares Are Trading at a Premium

Cisco shares are trading at a premium, as suggested by the Value Score of F. In terms of the forward 12-month price/sales, CSCO is trading at a premium of 6.83X, higher than the broader sector’s 6.79X and Hewlett Packard Enterprise’s 1.35X.

However, Cisco shares are trading at a discount compared with Arista Networks and Broadcom. In terms of the forward 12-month P/S, Arista Networks and Broadcom shares are trading at 17.8X and 12.18X, respectively.

CSCO Stock’s Valuation

Image Source: Zacks Investment Research

Conclusion

Despite trading at a modest premium, Cisco’s improving fundamentals and expanding AI opportunity continue to support a constructive long-term outlook. Strong momentum in AI infrastructure, Silicon One, Acacia optics, campus networking and security, combined with rising earnings estimates and solid execution, provides multiple avenues for sustained growth. CSCO remains an attractive stock for investors seeking long-term exposure to enterprise networking and AI infrastructure driven by durable demand drivers and increasing revenue visibility.

CSCO currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Cisco Systems, Inc. (CSCO): Free Stock Analysis Report

Broadcom Inc. (AVGO): Free Stock Analysis Report

Arista Networks, Inc. (ANET): Free Stock Analysis Report

Hewlett Packard Enterprise Company (HPE): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).