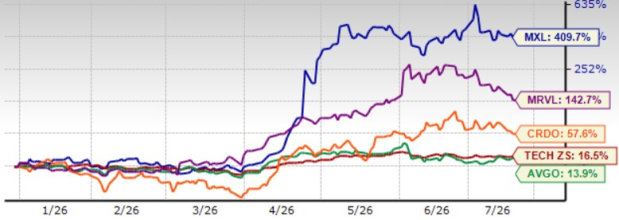

MaxLinear MXL shares closed at $88.84 on July 15, 30.8% lower from the 52-week high of $128.30 the company hit on June 30. The pullback reflects some profit-taking following the stock’s massive year-to-date (YTD) surge, while investors assess whether the company can sustain its AI-driven growth trajectory. MXL shares have jumped 409.7% YTD, outperforming the broader Zacks Computer and Technology sector’s return of 16.5%.

However, we believe the share price appreciation is limited in the near term given supply chain constraints, rising manufacturing costs, increasing dependence on hyperscale spending and stiff competition from the likes of Marvell Technology MRVL, Broadcom AVGO and Credo Technology CRDO. YTD, shares of Marvell, Broadcom and Credo have returned 142.7%, 13.9% and 57.6%, respectively. So, what should investors do with MXL stock? Let’s find out.

MXL Stock’s Price Performance

Image Source: Zacks Investment Research

Strong AI Infrastructure Demand Aids MXL’s Prospects

MaxLinear has emerged as one of the fastest-growing beneficiaries of AI networking infrastructure, with investors increasingly pricing in a multi-year optical data center growth cycle. MaxLinear’s rapidly expanding optical connectivity business for hyperscale AI data centers has been a key catalyst. Infrastructure revenues surged 136% year over year in the first quarter of 2026 to become the company's largest business, driven by production ramps of optical interconnect products. MXL increased its 2026 optical data center revenue outlook to $150-$170 million, reflecting stronger customer demand and improving visibility. For the second quarter of 2026, MXL expects revenues between $160 million and $170 million.

The company’s expanding hyperscale AI clientele is a major driver. MaxLinear’s management has disclosed that its Keystone PAM4 DSP platform is ramping at multiple major hyperscale customers across the United States and Asia for both 400G and 800G optical deployments. The company also expects a step-function increase in data center revenues beginning in the second quarter of 2026, with backlog already extending into 2027.

An expanding portfolio comprising Rushmore 200G/lane PAM4 DSP, Washington 200G/lane TIA and Annapurna 1.6T electrical retimer platform is expected to drive top-line growth. These innovative product pipeline targets next-generation 1.6T optical modules, Linear Pluggable Optics, Linear Receive Optics, Active Electrical Cables and Co-packaged optics. MaxLinear expects production ramps to begin in late 2026 with further revenue acceleration through 2027.

Moreover, growth is expanding beyond optical DSPs. MaxLinear has highlighted several new opportunities, including XGS-PON control plane architecture for hyperscale data centers, USB bridge controllers for AI server rack management, Panther storage accelerator SoCs, CRS radio SoCs for AI-enabled 5G infrastructure, and Wi-Fi 7 and fiber gateway platform. Persistent memory bottlenecks in AI servers are creating demand for Panther storage accelerators. MXL expects Panther storage accelerator revenues to at least double during 2026, providing another AI-related growth driver.

MXL Faces Multiple Near-Term Challenges

Despite strong demand from AI infrastructure customers, MaxLinear faces several near-term execution risks that are expected to hurt its near-term prospects. The company has acknowledged that industry-wide supply constraints remain a challenge, particularly for advanced wafers used in its optical data center products. To secure future production, MaxLinear has increased wafer prepayments, reflecting confidence in demand but also tying up working capital. At the same time, MXL warned that higher wafer, packaging and other manufacturing costs could weigh on profitability if they cannot be fully passed on to customers.

MaxLinear's growing dependence on hyperscale cloud providers is a headwind. The company’s bullish outlook is largely tied to production ramps of 400G and 800G optical DSPs and the successful commercialization of next-generation 1.6T products for AI data centers. While hyperscale spending remains robust, any slowdown in AI infrastructure investments, delays in customer deployments or changes in purchasing priorities could significantly affect revenue growth given the increasing contribution of the infrastructure segment. In addition, competition remains intense across AI networking, with larger rivals such as Broadcom, Marvell and Credo aggressively investing in high-speed optical connectivity and data center interconnect solutions.

Customer concentration also remains an important consideration. Although MaxLinear has expanded its presence across multiple hyperscale customers, a meaningful portion of its expected growth is still driven by a relatively small number of large cloud operators and Tier-1 OEMs.

MXL’s Earnings Estimate Revision Shows Steady Trend

The Zacks Consensus Estimate for second-quarter 2026 earnings is pegged at 33 cents per share, unchanged over the past 30 days. MXL reported earnings of 2 cents per share in the year-ago quarter.

MaxLinear, Inc Price and Consensus

MaxLinear, Inc price-consensus-chart | MaxLinear, Inc Quote

The consensus mark for 2026 earnings is pegged at $1.33 per share, unchanged over the past 30 days. MXL reported earnings of 31 cents per share in 2025.

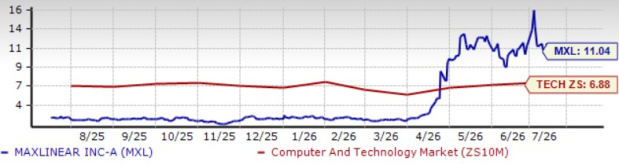

MXL Shares Are Overvalued

MaxLinear shares are overvalued, as suggested by a Value Score of F.

The MXL stock is trading at a forward 12-month price/sales (P/S) of 11.04X compared with the broader sector’s 6.88X. However, the stock is trading at a discount compared with Broadcom’s 12.33X, Credo’s 16.38X, and Marvell’s 13.02X.

MXL Stock’s Valuation

Image Source: Zacks Investment Research

Here’s Why MaxLinear Stock is a Hold Now

MaxLinear is well positioned to benefit from long-term AI infrastructure spending, supported by expanding hyperscale deployments, a growing optical connectivity portfolio and multiple new product launches. However, much of that optimism appears reflected in the stock following its exceptional YTD rally. With supply chain constraints, higher manufacturing costs, customer concentration and intense competition likely to remain key overhangs, investors may prefer to wait for stronger execution, broader revenue diversification or a more attractive valuation before turning more constructive on the stock.

MXL currently has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

MaxLinear, Inc (MXL): Free Stock Analysis Report

Marvell Technology, Inc. (MRVL): Free Stock Analysis Report

Broadcom Inc. (AVGO): Free Stock Analysis Report

Credo Technology Group Holding Ltd. (CRDO): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).