Tyson Foods Q1 Earnings Miss Estimates, Sales Grow 5.1% Y/Y

Tyson Foods, Inc. TSN reported solid first-quarter fiscal 2026 results, wherein the top line beat the Zacks Consensus Estimate and showed year-over-year growth, while the bottom line missed the same and declined from the prior year.

TSN’s Quarterly Performance: Key Insights

Tyson Foods posted adjusted earnings of 97 cents per share, which missed the Zacks Consensus Estimate of $1.01. The bottom line declined 15% from the year-ago quarter’s reported figure of $1.14.

Tyson Foods, Inc. Price, Consensus and EPS Surprise

Tyson Foods, Inc. price-consensus-eps-surprise-chart | Tyson Foods, Inc. Quote

Total sales of $14,313 million rose 5.1% year over year. The top line beat the Zacks Consensus Estimate of $14,122 million. Excluding the impact of a $150 million increase in legal contingency accruals, recognized as a reduction to sales, sales rose 6.2%. Average price changes had a 6.5% positive impact on the top line, while total volumes dipped 0.3% year over year.

The gross profit in the quarter was $808 million, down from the $1,095 million reported in the year-ago period. Tyson Foods’ adjusted operating income decreased 13% to $572 million. The adjusted operating margin decreased 80 basis points year over year to 4%.

Decoding TSN’s Segmental Details

Beef: Sales in the segment increased to $5,771 million from $5,335 million reported in the year-ago quarter. Volumes fell 7.3% and the average price jumped 17.2% in the segment.

Pork: Sales in the segment declined to $1,609 million from $1,617 million reported in the year-ago quarter. Volumes grew 1.6% and the average price increased 1.6%.

Chicken: Sales in the segment improved to $4,212 million from $4,065 million reported in the year-ago quarter. Volumes grew 3.7%, but the average price was down 0.1%.

Prepared Foods: Sales in the segment came in at $2,673 million, up from $2,473 million reported in the year-ago quarter. Volumes grew 0.2% and the average price rose 7.9%.

International/Other: Sales in the segment were $582 million compared with $584 million reported in the year-ago quarter. Volumes fell 0.8%, whereas the average sales price increased 0.5%.

Tyson Foods’ Other Financial Updates

The company exited the quarter with cash and cash equivalents of $1,278 million, long-term debt of $7,453 million and total shareholders’ equity (including non-controlling interests) of $18,163 million. For the three months ended Dec. 27, 2025, cash provided by operating activities amounted to $942 million.

Liquidity was $4.5 billion as of Dec. 27, 2025. Management expects total liquidity to stay above the company’s minimum target of $1 billion in fiscal 2026.

Tyson Foods projects capital expenditures in the range of $700 million to $1 billion for fiscal 2026, involving investments in profit-improvement projects and projects for maintenance and repair.

Adjusted free cash flow amounted to $690 million in the fiscal first quarter. In fiscal 2026, free cash flow is expected to be in the range of $1.1-$1.7 billion.

What to Expect From TSN in FY26?

For fiscal 2026, the United States Department of Agriculture (“USDA”) anticipates domestic protein production (beef, pork, chicken and turkey) to rise around 1% compared with the level of fiscal 2025.

For the Beef segment, the USDA projects domestic protein production to dip nearly 2% year over year. The company expects an adjusted operating loss of $250-$500 million in fiscal 2026, an improvement from its earlier guidance of a $400-$600 million loss.

For Pork, the USDA projects domestic production to rise nearly 2%. The company expects adjusted operating income of $250-$300 million, compared with its prior outlook of $150-$250 million and domestic production growth of nearly 3%.

For Chicken, the USDA anticipates domestic production to grow about 1% year over year. The company now expects adjusted operating income of $1,650-$1,900 million, up from its previous forecast of $1,250-$1,500 million.

For Prepared Foods, management projects adjusted operating income of $1,250-$1,350 million for fiscal 2026, significantly higher than its earlier guidance of $950-$1,050 million.

For International/Other, management projects adjusted operating income of $150-$200 million for fiscal 2026.

Total company’s revenue growth is anticipated in the range of 2-4% in fiscal 2026 compared with the fiscal 2025 level. Adjusted operating income is envisioned in the $2.1-$2.3 billion band.

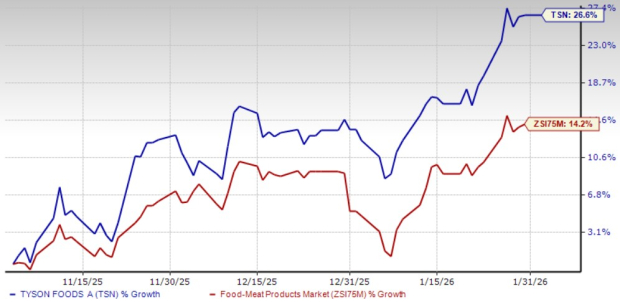

The Zacks Rank #3 (Hold) company’s shares have gained 26.6% in the past three months compared with the industry’s growth of 14.2%.

Image Source: Zacks Investment Research

Stocks to Consider

United Natural Foods, Inc. UNFI distributes natural, organic, specialty, produce and conventional grocery and non-food products in the United States and Canada. At present, United Natural flaunts a Zacks Rank of 1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The consensus estimate for United Natural’s current fiscal-year sales and earnings implies growth of 1.4% and 197.2%, respectively, from the year-ago figures. UNFI delivered a trailing four-quarter earnings surprise of 52.1%, on average.

Mama's Creations, Inc. MAMA manufactures and markets fresh deli-prepared foods in the United States. At present, MAMA sports a Zacks Rank of 1. Mama's Creations delivered a trailing four-quarter earnings surprise of 133.3%, on average.

The consensus estimate for Mama's Creations’ current fiscal-year sales and earnings implies growth of 39.9% and 44.4%, respectively, from the year-ago figures.

The Hershey Company HSY engages in the manufacture and sale of confectionery products and pantry items in the United States and internationally. It flaunts a Zacks Rank #1 at present. HSY delivered a trailing four-quarter earnings surprise of 15%, on average.

The Zacks Consensus Estimate for Hershey’s current fiscal-year sales implies growth of 3.6%, from the year-ago figures.

#1 Semiconductor Stock to Buy (Not NVDA)

The incredible demand for data is fueling the market's next digital gold rush. As data centers continue to be built and constantly upgraded, the companies that provide the hardware for these behemoths will become the NVIDIAs of tomorrow.

One under-the-radar chipmaker is uniquely positioned to take advantage of the next growth stage of this market. It specializes in semiconductor products that titans like NVIDIA don't build. It's just beginning to enter the spotlight, which is exactly where you want to be.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Tyson Foods, Inc. (TSN): Free Stock Analysis Report

Hershey Company (The) (HSY): Free Stock Analysis Report

United Natural Foods, Inc. (UNFI): Free Stock Analysis Report

Mama's Creations, Inc. (MAMA): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).