Buy, Sell or Hold Shopify Stock? Key Tips Ahead of Q4 Earnings

Shopify SHOP is scheduled to report its fourth-quarter 2025 results on Feb. 11.

For the to-be-reported quarter, Shopify expects revenues to grow at a mid-to-high twenties percentage rate on a year-over-year basis.

The Zacks Consensus Estimate for revenues is currently pegged at $3.58 billion, suggesting growth of 27.3% from the year-ago quarter’s reported figure.

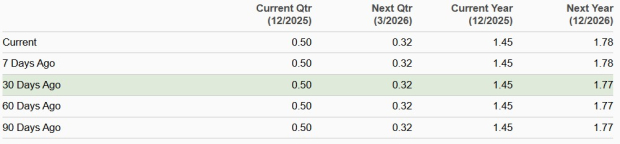

The consensus mark for earnings is pegged at 50 cents per share, unchanged over the past 30 days and indicating a 13.6% growth from the figure reported in the year-ago quarter.

Consensus Estimate Trend

Image Source: Zacks Investment Research

SHOP’s earnings beat the Zacks Consensus Estimate in one of the trailing four quarters, in line in two and missing once, the earnings surprise being 5.29%, on average.

Shopify Inc. Price and EPS Surprise

Shopify Inc. price-eps-surprise | Shopify Inc. Quote

Let’s see how things have shaped up prior to this announcement.

Key Factors to Note for SHOP’s Q4

Shopify is benefiting from strong growth in its merchant base, a trend that will likely be reflected in fourth-quarter results. Gross Merchandise Volume (GMV) in the third quarter of 2025 was $92.01 billion, which increased 32% year over year. Same-store sales growth from existing merchants, a higher number of merchants on SHOP’s platform and strong international growth drove GMV. These same factors are expected to have driven GMV growth in the to-be-reported quarter as well. The Zacks Consensus Estimate for fourth-quarter 2025 GMV is currently pegged at $120 billion, indicating 27.7% from the figure reported in the year-ago quarter.

Shopify’s Merchant Solutions revenues are expected to have benefited from the company’s AI push. Shopify hosts a data trove thanks to an expanding merchant base and a growing number of transactions. This huge amount of data is helping Shopify offer better shopping experiences to merchants and eventually their customers. The company is leveraging agentic commerce to boost shopper experience, beginning with product discovery to conversation and finally checkout through tools like Catalog (product discovery), Universal Cart and Checkout Kit.

New merchant-friendly tools like Shop Minis, Shop Cash, Sign in with Shop and Shop Pay solutions are helping Shopify win merchants rapidly. Shopify expects mid-to-high 20% revenue growth for the fourth quarter of 2025, led by sustained strength in Merchant Solutions. International growth, especially in Europe and emerging markets, is a key catalyst. Shopify’s expanding partner base is noteworthy in this regard. The company’s partnership with Perplexity is helping it gain a footprint in conversational shopping, while partners like OpenAI (ChatGPT) and Microsoft (CoPilot) are helping to smooth out in-chat shopping flows.

The consensus mark for Merchant Solutions revenues is currently pegged at $2.80 billion, suggesting 30.5% growth from the figure reported in the year-ago quarter. The Zacks Consensus Estimate for fourth-quarter 2025 Subscription revenues is currently pegged at $778 million, indicating 16.8% growth from the figure reported in the year-ago quarter.

However, Shopify’s near-term performance is expected to suffer from modest earnings growth given gross margin headwind, a challenging macroeconomic condition and stiff competition. The company’s gross margin is suffering from a higher mix of low-margin Merchant Solutions revenues and the negative impact of rapid payments penetration.

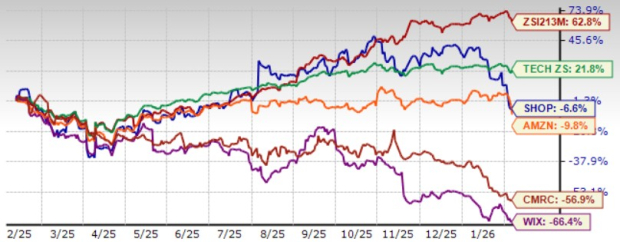

SHOP Shares Outperform Sector, Industry

SHOP shares have dropped 6.6% in a year, underperforming the Zacks Computer & Technology sector’s rise of 21.8% and the Zacks Internet Services industry’s return of 62.8%.

Shopify has outperformed peers including Amazon AMZN, Wix.com WIX and Commerce.com CMRC. In the trailing 12-month period, Amazon shares have declined 9.8% while Wix.com and Commerce.com shares have dropped 66.4% and 56.9%, respectively.

SHOP Stock’s Performance

Image Source: Zacks Investment Research

Wix is gaining from momentum in its core business and solid performance from new user cohorts. Wix continues to focus on strategic investments in AI offerings, Studio and commerce solutions. Amazon dominates the U.S. e-commerce market, driven by its “Buy with Prime" service. Amazon’s vast customer base, logistics and AI tools make it a formidable competitor worldwide.

However, the Value Score of F suggests a stretched valuation for Shopify at this moment.

SHOP stock is trading at a premium with a forward 12-month price/sales of 10.21X compared with the industry’s 7.22X, Amazon’s 2.77X, Wix.com’s 1.83X and Commerce.com’s 0.67X.

Shopify Trading at a Premium

Image Source: Zacks Investment Research

AI Push, Expanding International Footprint to Aid SHOP

Shopify’s long-term prospects are strong, given its growing merchant base and expanding partner base. Shopify’s rich partner, which includes Microsoft, TikTok, Roblox, PayPal, Snap, Pinterest, Criteo, IBM, Cognizant, Google Cloud and Adayen, has further expanded its merchant base.

Shopify’s growing international footprint is a key catalyst. Shopify Capital is now available in Germany, the Netherlands, Ireland and Spain, providing more merchants with access to growth funding. Shopify also launched Shopify Payments for POS to three additional countries and rolled out Tap to Pay in seven more countries in the third quarter of 2025. Shop App also expanded Track with Shop and Translations in six new markets in the third quarter of 2025, making it a top destination for local buyers globally.

Conclusion

Shopify is expected to suffer from gross margin headwinds and stiff competition in the near term. However, AI infusion and expanding international footprint bode well for the company’s long-term prospects. So, investors already holding the stock should remain put.

Shopify currently has a Zacks Rank #3 (Hold), which implies that investors should wait for a more favorable point to start accumulating the stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks Names #1 Semiconductor Stock

This under-the-radar company specializes in semiconductor products that titans like NVIDIA don't build. It's uniquely positioned to take advantage of the next growth stage of this market. And it's just beginning to enter the spotlight, which is exactly where you want to be.

With strong earnings growth and an expanding customer base, it's positioned to feed the rampant demand for Artificial Intelligence, Machine Learning, and Internet of Things. Global semiconductor manufacturing is projected to explode from $452 billion in 2021 to $971 billion by 2028.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Amazon.com, Inc. (AMZN): Free Stock Analysis Report

Wix.com Ltd. (WIX): Free Stock Analysis Report

Shopify Inc. (SHOP): Free Stock Analysis Report

Commerce.com, Inc. (CMRC): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).