Imperial Oil Stock Near 52-Week High: Time to Lock in Gains?

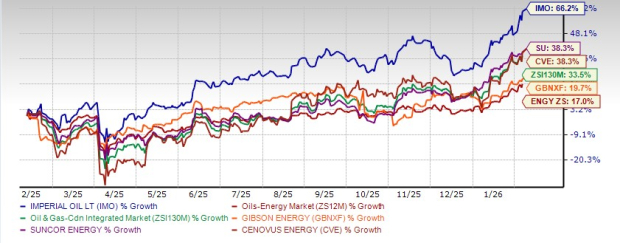

Shares of Imperial Oil Limited IMO closed at $114.34 on Monday, near its 52-week high of $114.52, following a gain of 66.2% in a year. During the same time period, the company’s shares outperformed the sub-industry and the broader oil and energy sector’s rise of 33.5% and 17%, respectively.

Peer comparison further highlights the strength, as Imperial Oil conveniently outperformed its peers: Gibson Energy Inc. GBNXF, which gained 19.7%, and Suncor Energy Inc. SU and Cenovus Energy Inc. CVE, both of which climbed 38.3% in the past year.

IMO Outperforms Industry, Sector & Peer Companies (GBNXF, SU, CVE)

Image Source: Zacks Investment Research

Imperial Oil stands out as one of Canada’s most resilient and growth-ready energy companies with a diversified portfolio spanning upstream, downstream and chemicals. Its strong upstream assets — Kearl, Cold Lake and Syncrude — deliver competitive costs, while its downstream and retail presence ensures steady cash flows even in volatile markets. Backed by ExxonMobil’s majority ownership, Imperial Oil benefits from unmatched financial strength and access to low-cost capital. Record production levels, efficiency gains and disciplined shareholder returns signal a company positioned not just to weather cycles but to create long-term value.

With the stock already achieving its 52-week high, investors are left grappling with a critical question: Should they ride the momentum or take profits at the peak and exit? Let us dig deeper into the company’s prospects to determine if it has enough room to rise further.

Factors Favoring Imperial Oil Stock

Record Production Levels Highlight Operational Strength: The company achieved the highest annual production in over 30 years at 438,000 gross oil-equivalent barrels per day in 2025. Core oil sands assets such as Kearl and Cold Lake remain long-life, low-decline resources that support sustained output. The start-up of the Leming SAGD project at Cold Lake adds incremental production with improved technology and lower unit costs over time. These assets provide long-term volume visibility and underpin IMO’s ability to generate durable cash flows across cycles.

Upstream Cost Leadership With Visible Improvement Runway: Imperial Oil’s upstream portfolio continues to deliver structural cost improvements. At Kearl, normalized unit cash costs remain below C$20 per barrel, with a defined trajectory toward C$18 per barrel, while Cold Lake reported unit cash costs of C$14.67 per barrel in 2025 and is targeting further reductions to C$13 per barrel by 2027. Management attributed these gains to sustained productivity enhancements, longer turnaround cycles, secondary recovery investments and improved asset reliability — all of which are embedded in the operating model rather than driven by short-term factors. As a result, margins are strengthened across commodity cycles, enhancing downside resilience and reinforcing IMO’s position as one of the lowest-cost oil sands producers in North America.

Exceptional Shareholder Returns Through Dividends and Buybacks: Imperial Oil returned $2.1 billion to its shareholders in the fourth quarter alone, including C$1.7 billion in share repurchases and C$361 million in dividends. The quarterly dividend was increased by a substantial 20% to 87 Canadian cents per share, reflecting management confidence in cash flow durability. Over the full year, dividends and buybacks totaled more than C$4.5 billion. This aggressive capital return strategy enhances per-share metrics and makes the stock attractive for income-focused and long-term investors. Although IMO has a strong track record of dividend payouts with an annualized yield of 1.8%, it lags behind its peers, as Cenovus Energy, Gibson Energy and Suncor Energy provide an impressive annualized yield of 2.8%, 6.1% and 3.2%, respectively.

Strong Balance Sheet and Liquidity Position: The company ended 2025 with C$1.1 billion in cash and relatively stable debt of about C$4.0 billion, maintaining a conservative balance sheet. Strong operating cash flow of C$6.7 billion for the year comfortably funded capex, dividends and buybacks without stressing leverage. This financial flexibility allows Imperial Oil to weather commodity downturns, fund growth projects and continue shareholder returns without relying heavily on external financing. Peer comparison further highlights the company’s strength, as Suncor Energy has reported a crippling long-term debt of C$9 billion.

IMO: Risks to Watch

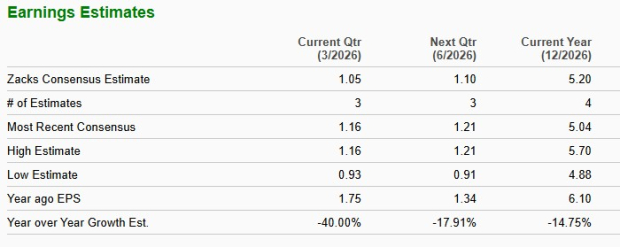

2026 Earnings Estimates: The Zacks Consensus Estimate implies a 14.8% year-over-year decline in 2026 earnings per share, signaling a shift to negative earnings growth. This anticipated decline contrasts with the optimism embedded in the stock’s current price. In other words, investors are paying up for Imperial Oil at a point when fundamentals are expected to cool rather than accelerate.

IMO’s Earnings Estimate

Image Source: Zacks Investment Research

Earnings Decline Reflects High Sensitivity to Crude Prices: Imperial Oil’s net income fell sharply year over year, with fourth-quarter 2025 net income declining to C$492 million from C$1.2 billion in the prior-year quarter. Lower crude prices significantly reduced upstream realizations, highlighting the company’s continued exposure to commodity price volatility. Despite integration benefits, sustained low oil prices would pressure earnings, limit free cash flow and potentially constrain future dividend growth. Imperial Oil’s peer companies, like Cenovus Energy, Gibson Energy and Suncor Energy, are also sensitive to oil price fluctuations, posing a risk to reduced margins.

Rising Capital Intensity Reduces Near-Term Cash Flexibility: For the fourth quarter of 2025, Imperial Oil’s capital and exploration expenditures increased to C$651 million and over C$2.0 billion for the full year. While investments support long-term growth, they reduce near-term free cash flow available for shareholder returns. Continued high capex requirements for oil sands, renewable fuels and emissions-related projects increase execution risk and could weigh on returns if commodity prices weaken or project economics disappoint.

The Chemicals Segment Remains Structurally Weak: Imperial Oil’s chemicals business delivered only C$9 million in net income in the fourth quarter of 2025, down sharply from prior periods due to weaker polyethylene margins. This segment is highly cyclical and exposed to global oversupply and demand uncertainty. Continued weakness limits diversification benefits and could remain a drag on consolidated earnings, especially if petrochemical markets fail to recover meaningfully.

Conclusion

Imperial Oil has firmly established itself as a leading Canadian energy producer with record production levels, structurally declining upstream costs and long-life oil sands assets that provide strong cash flow visibility across commodity cycles. The company’s integrated model cushions earnings volatility, while its downstream and retail operations stabilize returns during oil price weakness. A conservative balance sheet, ample liquidity and ExxonMobil’s backing enhance financial resilience and capital discipline. Importantly, Imperial Oil’s aggressive dividends and buybacks continue to lift per-share value even as earnings normalize.

While near-term EPS may soften, the company’s cost leadership, shareholder-friendly capital allocation and ability to sustain returns through cycles justify patience. For investors already positioned, retaining the Zacks Rank #3 (Hold) stock allows continued participation in steady cash returns and long-term value creation without materially increasing downside risk.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Just Released: Zacks Top 10 Stocks for 2026

Hurry – you can still get in early on our 10 top tickers for 2026. Handpicked by Zacks Director of Research Sheraz Mian, this portfolio has been stunningly and consistently successful.

From inception in 2012 through November, 2025, the Zacks Top 10 Stocks gained +2,530.8%, more than QUADRUPLING the S&P 500’s +570.3%.

Sheraz has combed through 4,400 companies covered by the Zacks Rank and handpicked the best 10 to buy and hold in 2026. You can still be among the first to see these just-released stocks with enormous potential.

See New Top 10 Stocks >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Suncor Energy Inc. (SU): Free Stock Analysis Report

Imperial Oil Limited (IMO): Free Stock Analysis Report

Cenovus Energy Inc (CVE): Free Stock Analysis Report

Gibson Energy Inc. (GBNXF): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).