HD Jumps 17% in 3 Months: Should You Buy, Hold or Sell the Stock?

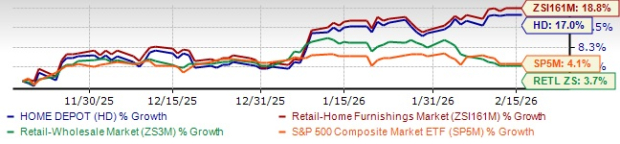

Shares of The Home Depot, Inc. HD have risen 17% over the past three months, slightly underperforming the Zacks Retail - Home Furnishings industry's growth of 18.8%. However, this prominent player in the home improvement market has outpaced the Retail-Wholesale sector’s return of 3.7% and the S&P 500's rally of 4.1% during the same period. The stock now sits 8.4% below its 52-week high of $426.75 reached in September.

HD’s Past 3-Month Performance

Image Source: Zacks Investment Research

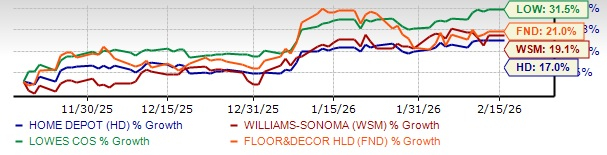

However, the stock has lagged key peers such as Lowe’s Companies Inc. LOW, Williams-Sonoma, Inc. WSM and Floor & Decor Holdings, Inc. FND over the past three months. Lowe’s, Williams-Sonoma, and Floor & Decor Holdings have posted growth of 31.5%, 19.1% and 21%, respectively.

HD vs. Peer Performances

Image Source: Zacks Investment Research

Closing at $391.05 in Friday’s trading session, Home Depot is trading above its 50 and 200-day simple moving averages of $365.99 and $373.14, respectively, indicating a favorable technical setup for the stock.

HD Trades Above 50 & 200-Day Moving Averages

Image Source: Zacks Investment Research

HD Builds Momentum Through Pro Expansion & Digital Innovation

Home Depot’s long-term growth strategy is increasingly anchored in the expansion of its Pro ecosystem, strengthened through the additions of SRS and GMS. These platforms extend the company’s reach into specialty categories, such as roofing, drywall, ceilings and steel framing.

By combining retail scale with wholesale distribution expertise, Home Depot is deepening relationships with professional contractors. This integrated structure enhances cross-selling opportunities and positions the company as a comprehensive solutions provider for complex projects.

Building on this foundation, the company is enhancing its Pro engagement through advanced digital innovation. Its AI-powered blueprint takeoffs tool uses proprietary algorithms to analyze construction plans and generate material estimates with greater speed and precision. This replaces a traditionally manual, time-intensive process and significantly improves planning efficiency. The technology strengthens contractor productivity and simplifies procurement decisions.

Complementing these tools is Home Depot’s continued investment in fulfillment and operational efficiency. Faster delivery speeds, improved inventory visibility and optimized freight processes are elevating the overall customer experience. These enhancements ensure that once materials are planned and ordered, they can be sourced and delivered seamlessly. The result is a smoother, more reliable end-to-end workflow for customers.

Home Depot continues to support its long-term growth through disciplined capital allocation, balancing reinvestment with shareholder returns. In the third quarter of fiscal 2025, the company invested about $900 million in capital expenditure focused on store expansion, supply-chain upgrades and technology enhancements, with the full-year capex projected at 2.5% of sales.

HD’s Downward Estimate Revisions Raise Concerns

The Zacks Consensus Estimate for Home Depot’s current fiscal year projects a 3.3% year-over-year increase in sales and a 4.9% decline in EPS. For the next fiscal year, the consensus estimate indicates a 4.2% rise in sales and 4.3% growth in earnings. The consensus estimate for EPS for the current and next fiscal years has fallen by 1 cent and 4 cents to $14.50 and $15.13, respectively, over the past 60 days.

Image Source: Zacks Investment Research

What’s Behind HD’s Downward Estimate Revision?

Home Depot acknowledged continued pressure in the broader home improvement environment, particularly within larger discretionary projects. Management noted that high interest rates and subdued housing turnover are weighing on customer demand for big-ticket remodels. While smaller repair and maintenance projects remain stable, larger-scale renovations have been deferred. This backdrop reflects ongoing macroeconomic uncertainty affecting homeowner confidence.

The company also pointed to weather-related volatility during the quarter, which negatively impacted seasonal categories. Unfavorable weather patterns reduced demand in certain outdoor and project-driven segments. Management indicated that storm-related benefits seen in prior periods did not repeat, creating a tougher comparison base. These external factors contributed to uneven category performance.

Demand softness in select Pro-heavy categories, including drywall and other building materials, reflects slower activity in new construction. Contractors remain cautious amid project delays and tighter financing conditions. This moderation has tempered volume momentum in specialty distribution channels. The environment continues to limit acceleration in Pro-driven growth.

HD’s Valuation Snapshot

The company is currently trading at a forward 12-month price-to-earnings (P/E) multiple of 25.74, which positions it at a premium compared with the industry’s average of 23.53 and the sector's 24.19. The stock is also trading above its median P/E level of 23.83 observed over the past year. The valuation suggests that Home Depot is overvalued.

Image Source: Zacks Investment Research

This valuation positioning becomes clearer when viewed alongside key peers. While HD trades at a premium to Lowe’s (with a forward 12-month P/E ratio of 21.96) and Williams-Sonoma (23.46), it trades at a discount to Floor & Decor Holdings (31.72).

How to Play HD Stock?

Home Depot continues to demonstrate structural strength through its Pro expansion strategy, digital investments and scale advantages. These initiatives support its long-term growth outlook and reinforce its leadership in the home improvement space.

That said, the stock’s premium valuation, combined with slower earnings momentum and ongoing housing-related headwinds, limits near-term upside potential. Much of the strategic optimism appears embedded in the current price. Considering the balance between long-term strengths and short-term uncertainties, maintaining existing positions appears sensible. New investors may benefit from waiting for clearer demand improvement or a more attractive valuation entry point.

Home Depot currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. Little-known AI firms tackling the world's biggest problems may be more lucrative in the coming months and years.

SeeWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Lowe's Companies, Inc. (LOW): Free Stock Analysis Report

The Home Depot, Inc. (HD): Free Stock Analysis Report

Williams-Sonoma, Inc. (WSM): Free Stock Analysis Report

Floor & Decor Holdings, Inc. (FND): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).