UnitedHealth vs. Humana: Which Healthcare Stock Has More Upside Now?

The landscape of managed care is undergoing significant changes due to rising medical utilization, evolving reimbursement models and ongoing cost challenges. Meanwhile, the aging population and the changing government-funded programs scenario are also playing a key role in shaping the growth patterns within the health insurance industry. Within this backdrop, UnitedHealth Group Incorporated UNH and Humana Inc. HUM stand out as two major players in U.S. managed care, with significant exposure to Medicare Advantage and other government programs.

Both companies operate at scale and aim to manage medical costs while expanding care delivery capabilities, yet they differ in diversification, vertical integration and revenue mix. UNH combines a broad insurance platform with a sizable health services arm, while HUM maintains a more concentrated focus on government-sponsored plans and value-based care initiatives.

Let’s dive deep and closely compare the fundamentals of the two stocks to determine which stock offers greater upside right now.

The Case for UNH

UnitedHealth, with a current market cap of $248.2 billion, continues to lean on its diversified operating model, combining UnitedHealthcare’s insurance platform with Optum’s health services businesses. This diversified structure allows the company to capture value across multiple points in the healthcare chain rather than relying solely on premium growth. Its Optum arm, which includes pharmacy services and data-driven care solutions, provides an additional earnings engine that complements its insurance operations. The company’s total revenues rose 12.3% year over year in the fourth quarter of 2025, with 17.5% growth at UnitedHealthcare and 8% growth at Optum.

The company continues to advance technology-led growth initiatives across its operations. It has been expanding the use of artificial intelligence and advanced analytics in areas such as claims processing, care coordination and pharmacy management to improve accuracy, reduce administrative costs and enhance medical management.

Scale remains one of UNH’s strongest competitive advantages. With a nationwide footprint and deep relationships across employers, Medicare and Medicaid, the company benefits from pricing leverage and strong provider contracting power. In the last reported quarter, UNH’s Medicare Advantage membership increased 7.6% year over year, along with 0.8% growth in domestic medical membership. It missed earnings estimates twice in the past four quarters and beat on the other occasions.

UnitedHealth Group Incorporated Price, Consensus and EPS Surprise

UnitedHealth Group Incorporated price-consensus-eps-surprise-chart | UnitedHealth Group Incorporated Quote

Financially, UNH is in a solid position. It ended 2025 with $28.1 billion in cash and short-term investments, sufficient to cover its short-term borrowings and current maturities of long-term debt, which stands at $6.1 billion. Its total debt-to-capital of 41.6% is above HUM’s 41.1% but below the industry’s 44.3%.

However, rising medical utilization has squeezed profit margins. In the fourth quarter of 2025, the company’s medical care ratio rose to 92.4% compared with 85.1% the previous year, indicating that rising medical costs are eating into the premiums collected. Medical costs surged 22.4% year over year in the quarter.

The Case for HUM

Humana, with a market cap of $21.1 billion, sets itself apart with a sharp focus on government-sponsored healthcare, especially in the realm of Medicare Advantage. This specialization allows it to develop a deep understanding of senior healthcare management, enabling the creation of tailored benefit structures and care programs that cater specifically to the needs of aging populations. In the fourth quarter of 2025, its total revenues rose 11.3% year over year.

The company has broadened its primary and home-based care services, which boosts its ability to improve patient outcomes beyond traditional insurance coverage. By investing in senior-focused care delivery models, HUM aims to control medical costs more effectively while enhancing member engagement and satisfaction. Its specialty membership rose 4% year over year, along with 7.6% growth in Medicare stand-alone PDP in the fourth quarter of 2025. It beat earnings in three of the past four quarters with an average surprise of 7%.

Humana Inc. Price, Consensus and EPS Surprise

Humana Inc. price-consensus-eps-surprise-chart | Humana Inc. Quote

As of Dec. 31, 2025, the company had cash and cash equivalents of $4.2 billion, with no short-term debt, which implies a solid capital position. Humana has been returning excess capital to its shareholders in the past several years. It bought back shares worth $151 million in 2025. The company also paid dividends of $430 million during 2025. However, its dividend yield of 2% is below UNH’s 3.1%.

Humana has been witnessing increasing operating expenses for the past few years. In 2022, 2023, 2024 and in the fourth quarter of 2025, the metric jumped 11.5%, 14.9%, 12.5% and 12%, year over year, respectively, due to higher benefits and operating costs. The benefit ratio came in at 93% in fourth-quarter 2025, which deteriorated 150 basis points year over year. Unlike UNH, HUM operates at a smaller scale and relies heavily on Medicare Advantage, making its earnings more exposed to shifts in government reimbursement rates and STAR rating fluctuations. Also, its return on asset of 4.1% is below UNH’s 4.8%.

How Do Estimates Compare for UNH & HUM?

The Zacks Consensus Estimate favors UNH at this stage. The consensus estimate for UNH’s 2026 earnings indicates an 8.2% increase from a year ago. Over the past month, the estimate has witnessed nine upward revisions with two downward adjustments. Meanwhile, the consensus estimate for revenues suggests a 1.6% decline.

On the other hand, the Zacks Consensus Estimate for HUM’s 2026 revenues indicates 18.6% year-over-year growth, but the same for EPS signals a massive 41% decline. Over the past month, the estimate has seen one upward revision with six downward adjustments.

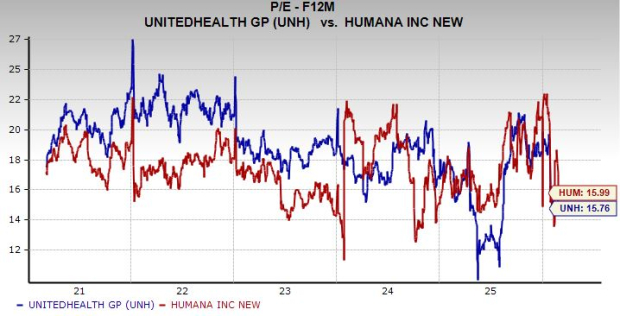

Valuation: UNH vs. HUM

From a valuation standpoint, UnitedHealth may appear slightly more expensive than the industry at first glance, but it represents its size, operational consistency and business diversification. Humana’s stock currently trades at a slightly higher multiple than UNH. UnitedHealth is currently priced at 15.76X forward 12-month earnings, compared to Humana’s 15.99X, both above the industry average of 13.48X.

Image Source: Zacks Investment Research

UNH currently trades below its average analyst price target of $361.43, implying a 27.2% potential upside from current levels. HUM also trades below its average analyst price target of $219.13, implying an attractive 24.5% potential upside from current levels.

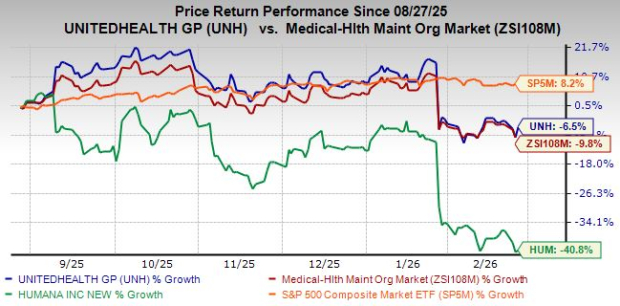

Price Performance Comparison

Over the past six months, UNH has shed less value than HUM and the industry. However, the S&P 500 increased 8.2% during this time.

Price Performance – UNH, HUM, Industry & S&P 500

Image Source: Zacks Investment Research

Conclusion

While both managed care giants are navigating higher medical costs and regulatory complexity, UnitedHealth appears better positioned at this stage. Its broader scale, diversified revenue streams and strong balance sheet provide a cushion against utilization pressures and reimbursement volatility. In contrast, Humana remains more exposed to Medicare Advantage concentration and margin swings. Considering earnings stability, estimate revisions and operational breadth, UNH stands out as the more compelling upside candidate right now.

While UnitedHealth currently carries a Zacks Rank #3 (Hold), Humana has a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Just Released: Zacks Top 10 Stocks for 2026

Hurry – you can still get in early on our 10 top tickers for 2026. Handpicked by Zacks Director of Research Sheraz Mian, this portfolio has been stunningly and consistently successful.

From inception in 2012 through November, 2025, the Zacks Top 10 Stocks gained +2,530.8%, more than QUADRUPLING the S&P 500’s +570.3%.

Sheraz has combed through 4,400 companies covered by the Zacks Rank and handpicked the best 10 to buy and hold in 2026. You can still be among the first to see these just-released stocks with enormous potential.

See New Top 10 Stocks >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

UnitedHealth Group Incorporated (UNH): Free Stock Analysis Report

Humana Inc. (HUM): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).