CorMedix Banks on DefenCath Sales in Q4 as Melinta Adds Upside

The majority of CorMedix’s CRMD revenues come from its lead product, DefenCath, which is approved as the first and only antimicrobial catheter lock solution in the United States. The product is indicated to reduce the incidence of catheter-related bloodstream infections (CRBSIs) in adult patients with kidney failure who receive chronic hemodialysis through a central venous catheter. CRBSIs can delay treatment, increase hospital stays, raise healthcare costs and increase the risk of death. Through DefenCath, CorMedix is addressing an important unmet medical need.

In the first nine months of 2025, DefenCath recorded $167.6 million in net sales, reflecting strong uptake trends. Like the previous three quarters of 2025, DefenCath is expected to remain a key top-line driver in the fourth quarter as well. The higher-than-expected utilization of DefenCath by outpatient dialysis customers is likely to have driven sales in the fourth quarter.

CorMedix recently reported preliminary fourth-quarter and full-year 2025 results, with net revenues of approximately $127 million and $310 million, respectively.

Management also introduced full-year 2026 revenue guidance of $300-$320 million, including $150-$170 million from DefenCath. Importantly, DefenCath’s 2026 revenue guidance is weighted toward the first half of the year.

Meanwhile, CorMedix took a major step in diversifying its business and reducing its high dependence on DefenCath with the acquisition of Melinta Therapeutics in August 2025. The acquisition added seven approved therapies to CRMD’s commercial portfolio, strengthening its presence in hospital acute care and infectious disease markets. These acquired products from Melinta generated $12.8 million in revenues for CorMedix in the third quarter of 2025, reflecting a partial quarter of sales.

CorMedix’s preliminary net revenues for the fourth quarter and full-year 2025 reflect the growing momentum with DefenCath and early Melinta portfolio contributions.

As CorMedix is gearing up to report fourth-quarter results, DefenCath is expected to have sustained strong sales growth and adoption, while the Melinta portfolio is likely to have provided incremental growth, supporting overall top-line momentum.

CRMD’s Competition in the Target Market

While CorMedix is currently benefiting from DefenCath’s success, it faces strong competition from larger, established players in the heparin market.

DefenCath is a fixed-dose combination of taurolidine, an antimicrobial agent, and heparin, designed for a specific group of kidney failure patients. While CorMedix currently enjoys a first-mover advantage in the United States, competition remains a key risk. Large companies such as Pfizer PFE, Amphastar Pharmaceuticals AMPH, B. Braun, Baxter and Fresenius Kabi USA already sell heparin for various uses.

Pfizer, which markets Heparin Sodium Injection for dialysis, surgery and thrombosis, could use its global scale to enter the CRBSI prevention space. Amphastar Pharmaceuticals, with end-to-end control over enoxaparin production, also has the efficiency and technical capabilities to pursue similar opportunities. If either Pfizer or Amphastar Pharmaceuticals expands into catheter-related infection prevention, CorMedix could face significant competitive pressure.

With broader pipelines, larger manufacturing capacity and stronger financial resources, these companies could quickly emerge as major competitors if they target catheter-related bloodstream infections, potentially weakening CorMedix’s market position and long-term growth prospects.

CRMD’s Stock Price, Valuation and Estimates

Shares of CorMedix have plunged 33.1% in the past six months against the industry’s growth of 23.9%. The stock has also underperformed the sector and the S&P 500 index during the same time frame, as seen in the chart below.

Image Source: Zacks Investment Research

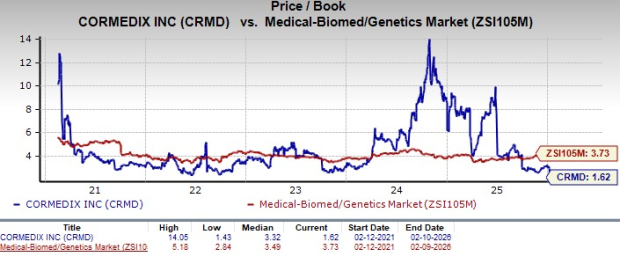

From a valuation standpoint, CorMedix is trading at a discount to the industry. Going by the price/book ratio, the company’s shares currently trade at 1.62, lower than 3.73 for the industry. The stock is also trading below its five-year mean of 3.32.

Image Source: Zacks Investment Research

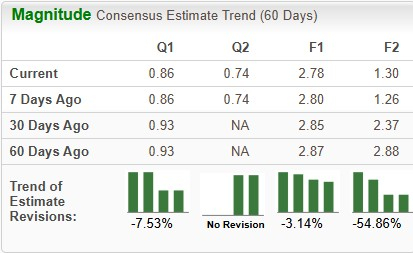

Estimates for CorMedix’s 2025 earnings have decreased from $2.85 to $2.78 per share in the past 30 days, while estimates for 2026 earnings have declined from $2.37 to $1.30 during the same timeframe.

Image Source: Zacks Investment Research

CRMD’s Zacks Rank

CorMedix currently carries a Zacks Rank #5 (Strong Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Picks Stock Most Likely to "At Least Double"

Our experts have revealed their Top 5 recommendations with money-doubling potential – and Director of Research Sheraz Mian believes one is superior to the others. Of course, all our picks aren’t winners but this one could far surpass earlier recommendations like Hims & Hers Health, which shot up +209%.

See Our Top Stock to Double (Plus 4 Runners Up) >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Pfizer Inc. (PFE): Free Stock Analysis Report

Amphastar Pharmaceuticals, Inc. (AMPH): Free Stock Analysis Report

CorMedix Inc (CRMD): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).