Buy the Dip in Nvidia Stock After Q4 Earnings, or is it Too Soon?

Despite posting blowout quarterly results as usual, Nvidia NVDA stock is now down over 6% since its Q4 report on Wednesday.

This comes as the chip giant’s Q4 sales of $68.12 billion and EPS of $1.62 stretched 73% and 82% year over year, respectively, and represented significant sequential growth as well.

Still, the stellar results didn't calm deeper investor concerns about the sustainability of the AI boom, concentration risks, and future growth, although Nvidia impressively surpassed Wall Street’s expectations.

Image Source: Zacks Investment Research

AI Sustainability Concerns

Notably, a recurring theme across analyst commentary is skepticism about how long hyperscalers can keep spending tens of billions on AI infrastructure.

Others question whether AI monetization is happening fast enough to justify the spending, and the shift in sentiment is weighing on Nvidia because it’s the primary beneficiary of that spending.

Furthermore, 90% of Nvidia’s revenue now comes from data centers, and much of that is just from five major cloud providers, which include Amazon AMZN, Alphabet GOOGL, Microsoft MSFT, Oracle ORCL, and Alibaba BABA. That level of dependency raises questions about what happens if even one of those customers slows orders.

Investors are also increasingly concerned about competition from AMD AMD, and that hyperscalers are working on their own in-house AI accelerators, with an emphasis on Alphabet and Amazon building out custom AI chips, with others likely to eventually follow suit.

In other words, even if Nvidia remains dominant, the fear is that margins or growth rates could eventually compress.

Nvidia’s Reassuring Revenue Guidance

While Nvidia didn’t provide CapEx or EPS guidance, which is consistent with its long-standing practice of typically only providing revenue guidance, its top-line forecast reassuringly beat Wall Street’s expectations.

For its current fiscal 2027, Nvidia issued Q1 revenue guidance of $78B plus or minus 2%, which came in pleasantly above analysts’ expectations of about $72.8B and would equate to at least 73% YoY growth and 12% sequentially.

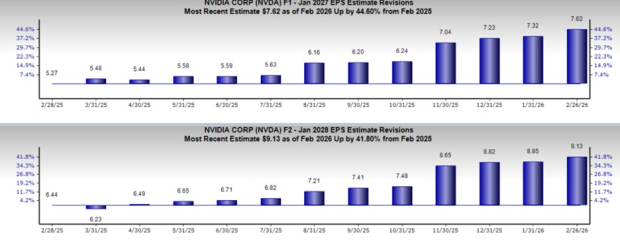

Tracking the Trend of EPS Revisions

Following Nvidia’s stellar Q4 results and positive guidance, EPS estimates for its FY27 and FY28 have trended over 3% higher in the last week.

In the last 90 days, these revisions have risen roughly 7% respectively. Nvidia’s annual earnings are now expected to leap 60% in FY27 and are projected to increase another 20% in FY28 to $9.13 per share.

Image Source: Zacks Investment Research

More astonishing, the year-ago EPS estimates picture shows that Nvidia’s FY27 and FY28 revisions have climbed over 40%.

Image Source: Zacks Investment Research

Nvidia’s Compelling P/E Valuation

Further encouraging is that Nvidia is trading near its cheapest forward P/E valuation in a decade, offering a noticeable discount to its median of 45X during this period, and well below highs of 118X.

It’s noteworthy that NVDA is only trading at a slight premium to the benchmark S&P 500 and is beneath its Zacks Semiconductor-General Industry average of 27X.

Image Source: Zacks Investment Research

Conclusion & Final Thoughts

Even with AI sustainability concerns looming, it doesn’t look like the time to count Nvidia out.

Ultimately, investors shouldn’t dismiss Nvidia despite rising concerns about the long-term sustainability of AI spending because the company continues to demonstrate overwhelming demand, structural dominance, and is the leader in a revolutionary technology — factors that outweigh near-term worries about energy use, customer concentration, or a potential AI spending plateau.

Based on a very positive trend of EPS revisions, Nvidia stock currently sports a Zacks Rank #1 (Strong Buy).

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

NVIDIA Corporation (NVDA): Free Stock Analysis Report

Amazon.com, Inc. (AMZN): Free Stock Analysis Report

Advanced Micro Devices, Inc. (AMD): Free Stock Analysis Report

Microsoft Corporation (MSFT): Free Stock Analysis Report

Oracle Corporation (ORCL): Free Stock Analysis Report

Alphabet Inc. (GOOGL): Free Stock Analysis Report

Alibaba Group Holding Limited (BABA): Free Stock Analysis Report

Meta Platforms, Inc. (META): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).