Data storage giant Seagate Technology Holdings plc (STX) has emerged as a standout beneficiary of the artificial intelligence (AI) boom, with its stock surging in triple digits over the past year as demand for data storage skyrockets alongside AI model training. And that momentum has carried strongly into 2026. A combination of solid earnings, improving fundamentals, and increasingly bullish analyst calls has propelled the stock to new highs.

On Apr. 6, shares hit a record $470.23 after Morgan Stanley elevated Seagate to its “Top Pick” in IT hardware, replacing peer Western Digital (WDC), a notable shift that highlights growing confidence in Seagate’s outlook. The bullish call is backed by a much brighter outlook for the hard-disk drive (HDD) market. According to the investment bank, demand from hyperscale data centers continues to accelerate, while supply remains tight, creating a favorable imbalance that could persist through 2028.

More Yield, Less Trap: Sign up free to get Barchart’s daily Dividend Investor newsletter straight to your inbox.

This dynamic is expected to give Seagate greater pricing power and stronger earnings visibility, particularly through 2027. Reflecting this optimism, Morgan Stanley raised its price target on the stock to $582 from $468, while maintaining an “Overweight” rating, signaling further upside potential. So, with Seagate now firmly positioned as Wall Street’s preferred play in the HDD space, here’s a closer look at this stock.

About Seagate Stock

California-based Seagate Technology has long been a key player in mass-capacity data storage, helping organizations unlock the growing value of data. The company’s portfolio of storage solutions is widely used by hyperscale cloud providers, enterprises, and consumers to store, manage, and protect the data that underpins digital transformation. With a history spanning more than four decades, Seagate has consistently evolved alongside the data economy, developing high-capacity and performance-driven storage technologies designed to operate at a global scale.

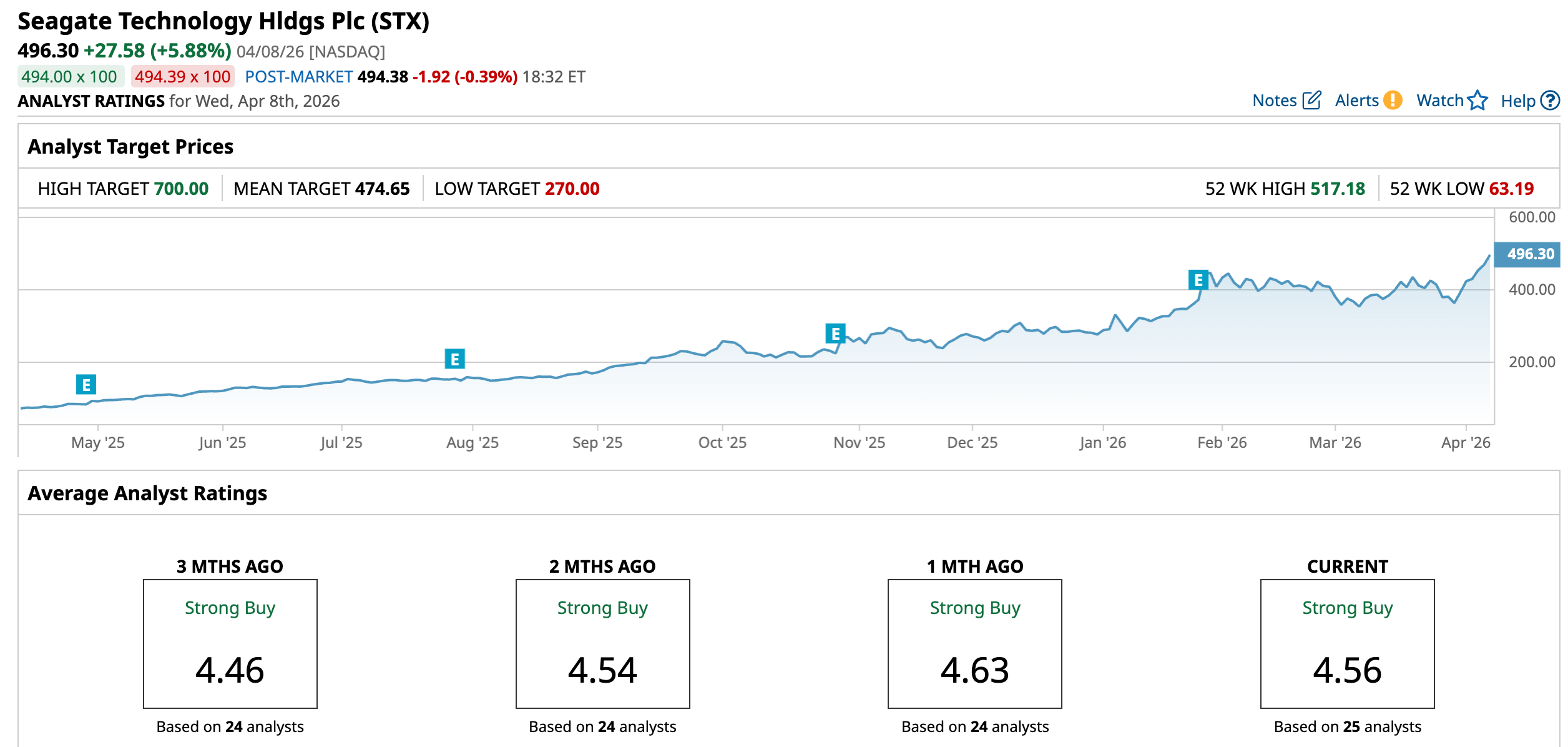

Currently commanding a market capitalization of about $102.22 billion, Seagate has become one of the most explosive winners of the AI-driven rally. The stock has surged an eye-popping 645.87% over the past year, massively outperforming the broader S&P 500 Index ($SPX), which gained just 36.13% in the same period. And the momentum hasn’t slowed in 2026.

Shares are already up 80.22% year-to-date (YTD), even as the broader market has slipped 0.92% into the red, highlighting just how strong investor appetite remains for AI-linked infrastructure plays like Seagate. Following its record high on Apr. 6, sparked by Morgan Stanley's bullish call, the stock continues to hover near peak levels, signaling sustained confidence and leaving investors watching closely for the next leg of upside.

www.barchart.com

www.barchart.com Inside Seagate’s Q2 Earnings Report

Seagate delivered a powerhouse fiscal second quarter for 2026, reported in late January, with results that handily beat Wall Street expectations across the board. The company generated $2.83 billion in revenue, marking a solid 22% year-over-year (YOY) increase and comfortably topping analyst estimates of $2.75 billion. The surge was largely fueled by intense demand from global cloud providers and data centers, which are racing to secure high-capacity storage to support the massive datasets required for generative AI training and inference.

That strength was clearly visible in the company’s core segment. Data center revenue climbed to $2.2 billion, up 28% YOY, and now accounts for nearly 79% of total revenue, underscoring how central AI-driven infrastructure has become to Seagate’s growth story. Profitability was even more impressive. The company posted a record gross margin of 41.6%, a sharp jump from 34.9% a year ago, while non-GAAP earnings per share surged 53.2% to $3.11, crushing Wall Street’s forecast of $2.83.

Management attributed this blockbuster performance to strong operational execution, resilient data center demand, and the continued ramp of its HAMR-based Mozaic platform. On the technology front, Seagate highlighted that its Mozaic 3 HAMR drives are now qualified with all major U.S. cloud service providers, while development of its next-generation Mozaic 4 terabyte-per-disc products remains on track. These advancements support the company’s long-term roadmap, which aims to reach 10 terabytes per disc early in the next decade, signaling significant future capacity gains.

Financially, Seagate is in one of its strongest positions in years. The company generated $607 million in free cash flow during the quarter, the highest level in eight years, while maintaining a healthy balance sheet. This allowed the company to retire roughly $500 million in gross debt and return $154 million in capital to shareholders through dividends, ending the quarter with $1 billion in cash and equivalents.

Looking ahead, Seagate expects continued momentum, guiding for fiscal third-quarter revenue in the range of $2.80 billion to $3 billion, with a midpoint of $2.90 billion. At the same time, the company projects non-GAAP earnings to land between $3.20 and $3.60 per share, implying a midpoint of $3.40.

How Are Analysts Viewing Seagate Stock?

On Apr. 6, Seagate shares popped nearly 5.6% after Morgan Stanley struck a bullish tone on the stock. Analyst Erik Woodring pointed to strengthening demand for HDDs, particularly from hyperscalers, as the key driver behind the optimistic outlook for the stock. This rising demand is not only improving order visibility but also giving Seagate greater confidence in its ability to push pricing higher over time.

A major highlight is the sharp improvement in the pricing outlook. Large hyperscaler customers are now discussing prices close to $20 per terabyte for 2027–2028 purchases, compared to current expectations of around $13–$15. This suggests pricing could come in much higher than previously thought, boosting future profits.

The reason behind this pricing power is simple. Demand is rising fast, while supply isn’t expanding. With no significant new production capacity being added, the market remains tight, allowing HDD makers like Seagate to command better prices and improve margins over time. And it’s not just Morgan Stanley waving the bullish flag.

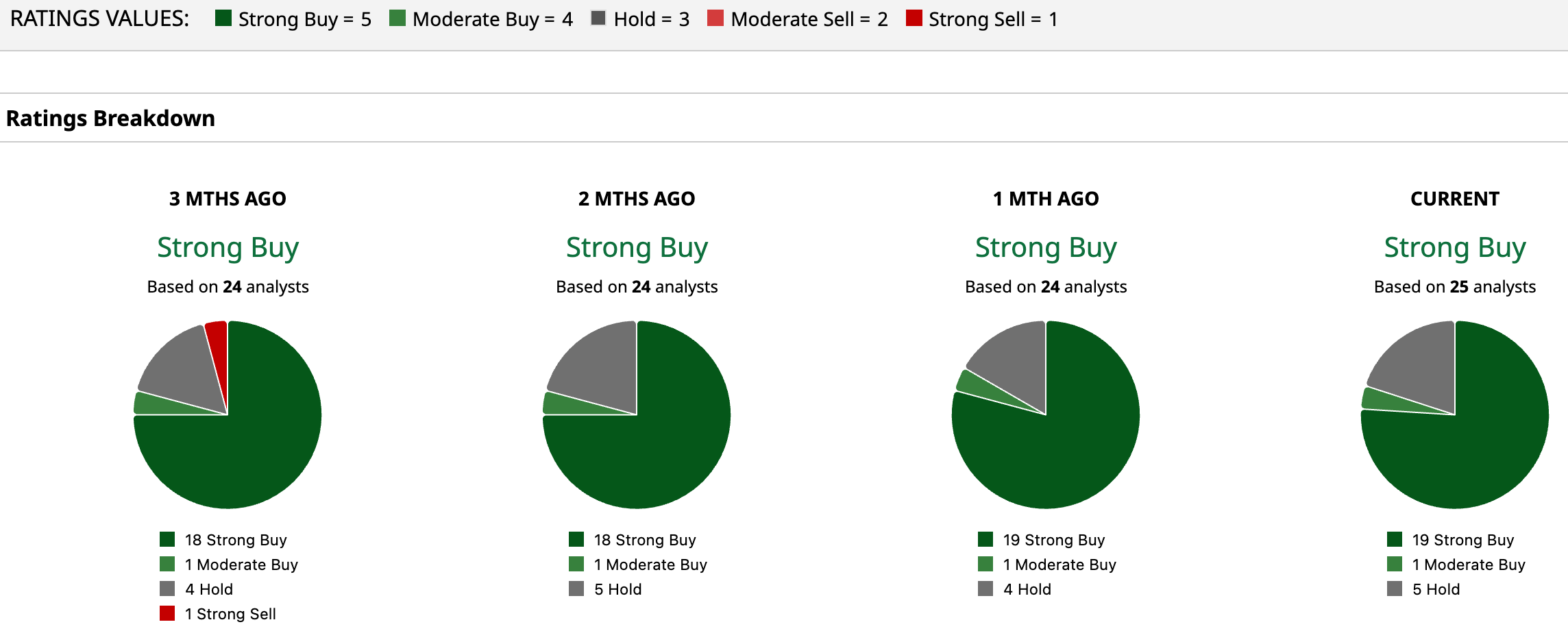

The overall sentiment on Wall Street toward Seagate is overwhelmingly positive. The stock currently carries a “Strong Buy” consensus rating, underscoring growing confidence in its AI-fueled growth trajectory. Among the 25 analysts covering the name, a striking 19 recommend “Strong Buy,” with only one “Moderate Buy” and five opting to stay on the sidelines with “Hold” ratings, tilting the balance heavily in favor of bulls.

The average price target of $474.65 points to limited near-term upside after the stock’s sharp rally. However, the Street-high target of $700 implies nearly 41% upside, suggesting that if current tailwinds persist, Seagate’s run may be far from over.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Tech Stocks Are Experiencing Historic 50-Year Weakness. Should You Buy the Dip in This 1 ETF? Hard Disk Drive Prices Are Rising. Why That Makes Seagate Stock a Top Buy. Lockheed Martin Stock Is Up 30% in 2026 and Yields 2%. Is It a Top Buy While the Iran War Drags On? Move Over, Western Digital! Why Seagate Is the New Top Stock Pick