Retail trader darling and AI-led data analytics company Palantir's (PLTR) stock should have been an expected beneficiary of the U.S./Israel and Iran war in the Middle East. Thanks to its advanced suite of products that aid decision-making and its proximity to the U.S. government, Palantir remains a crucial cog in the latter's defensive capabilities. However, its share price performance would not reflect as such.

PLTR stock is down over 14% since the war started, and the latest blow came from a familiar skeptic of the company: Michael Burry. The famed Big Short investor highlighted that Palantir's moat is weak and the likes of Anthropic provide a cheaper and easier-to-adapt alternative for enterprises.

Join 200K+ Subscribers: Find out why the midday Barchart Brief newsletter is a must-read for thousands daily.

www.barchart.com

www.barchart.com Why Is Burry Wrong?

However, cheaper is not always better. Palantir's much-vaunted Ontology layer provides enterprises with unmatched insights and aids faster decision-making, capabilities that others simply do not have right now. Notably, Ontology securely maps chaotic and siloed enterprise data into a unified digital twin while enforcing rigorous role-based access controls. An up-and-coming model from Anthropic cannot natively respect the security clearances of, say, a defense contractor or the patient privacy protocols of a hospital network without massive, expensive, and time-consuming internal engineering efforts. Thus, enterprises gladly pay a premium for Palantir because it provides the secure integration layer that transforms a generic intelligence model into a commercially viable operational tool with immediate utility.

More importantly, enterprises are highly focused on immediate return on investment, and Palantir collapses the time to value from several months of disjointed internal engineering using isolated application programming interfaces to just a few days through its immersive bootcamps. This then somewhat justifies the premium pricing model of Palantir, considering the immediate operational leverage, military-grade security, and seamless data integration it delivers for enterprises.

Moreover, Palantir is not standing still and has been constantly improving its offerings. Throughout late 2025 and early 2026, the company integrated a comprehensive suite of advanced models directly into its ecosystem. Enterprises can now seamlessly utilize OpenAI GPT 5.1, Anthropic models with massive two-million-token context windows, Nvidia (NVDA) Nemotron 3 for high-volume automation, and Grok 4.20 for complex reasoning tasks. By offering this diverse catalog within a secure, ontology-powered environment, Palantir ensures that clients always have access to the most optimal compute engine for their specific operational needs. This prevents the platform from becoming obsolete when a competitor releases a faster or cheaper model. Instead, Palantir simply incorporates the new model into its secure framework, effectively turning potential rivals into modular components of its own stack.

Finally, the firm is drastically reducing friction for developers building proprietary applications on top of its architecture. Recent updates to its toolchain include sophisticated code workspaces and near-real-time metrics tracking that allow engineering teams to monitor performance within seconds. Combined with an immersive five-day bootcamp strategy that radically compresses the sales cycle, these product iterations create an incredibly sticky ecosystem.

Overall, the continuous enhancement of developer tools and vertical-specific products ensures that switching away from the platform becomes increasingly financially and operationally prohibitive for any enterprise client.

Strong Financials With Not-So-Good Valuations

Palantir delivered another standout quarter, with its financial metrics continuing to impress. The company uses the “Rule of 40” as a key performance gauge, combining revenue growth and operating margin. A score above 40% is generally viewed as strong; Palantir’s latest reading reached an exceptional 127%.

The fourth quarter was yet another beat. Revenue totaled $1.41 billion, rising 70% year-over-year (YoY). Earnings per share increased 78% to $0.25, comfortably ahead of consensus expectations. Operating margin expanded nicely to 57% from 45% in the prior-year quarter.

Commercial revenue continued to narrow the gap with government revenue. U.S. commercial revenue surged 137% to $507 million, while U.S. government revenue grew 66% to $570 million. Total contract value signed during the quarter jumped 138% YoY to $4.26 billion, pointing to robust demand and greater revenue visibility.

Cash generation remained solid. Net cash from operating activities rose 69% YoY, and adjusted free cash flow increased 53% to $791.4 million. Palantir closed the quarter with $1.42 billion in cash and minimal short-term debt of $45.86 million.

For the first quarter, the company guided revenue to between $1.532 billion and $1.536 billion. For the full year 2026, guidance is set at $7.182 billion to $7.198 billion. At the midpoint, this implies roughly 140% growth for Q1 and 60% growth for the full year.

Yet, valuation continues to be the main point of caution. The stock trades at a forward P/E of 106.53x, P/S of 46.35x, and P/CF of 94.98x, all well above sector medians. Even the forward PEG ratio, which accounts for the company’s strong growth, stands at 2.32 compared with the sector median of 1.36.

Analyst Opinion on PLTR Stock

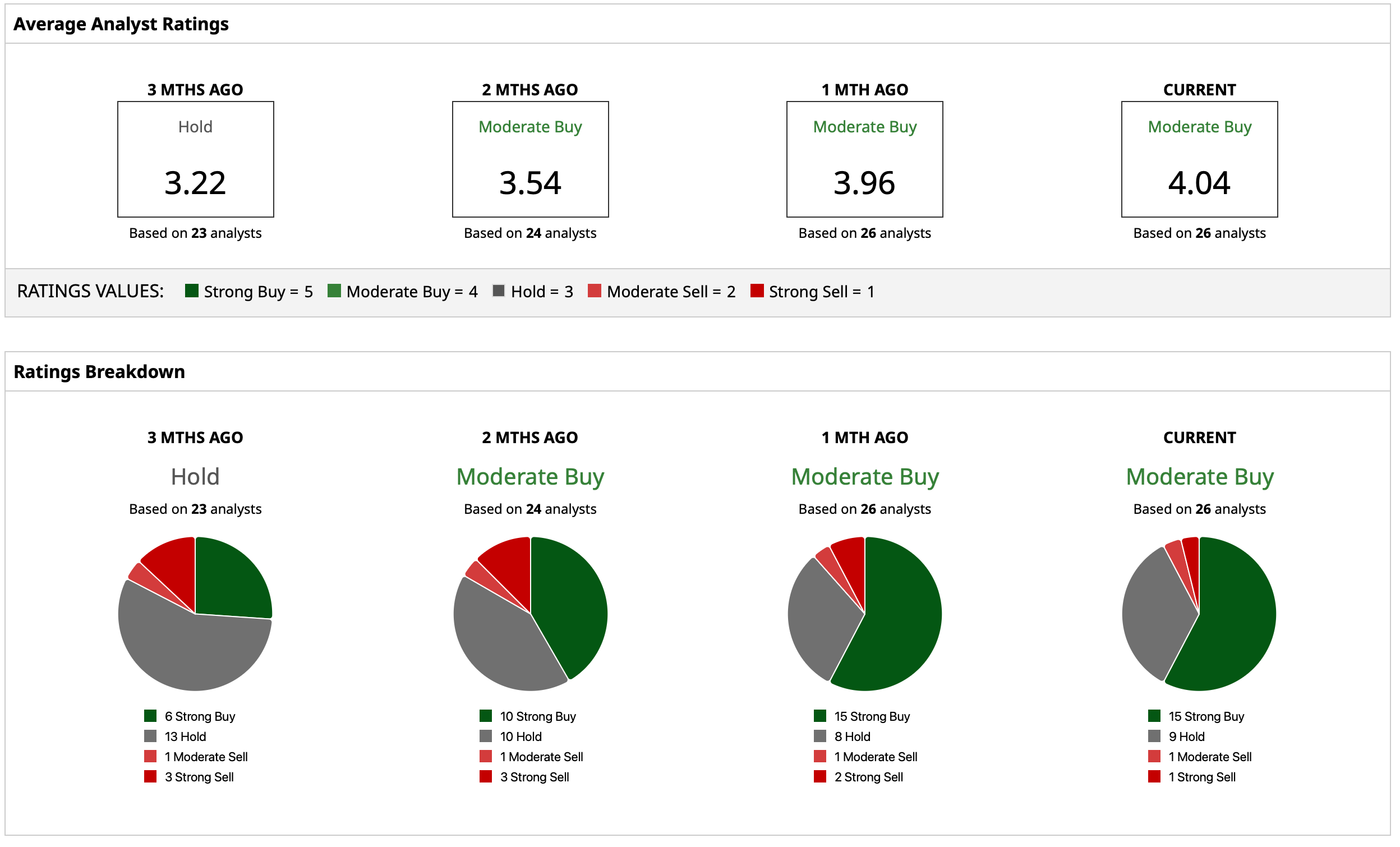

Thus, analysts have deemed the PLTR stock to be a “Moderate Buy,” with a mean target price of $198.30, which denotes an upside potential of about 55% from current levels. Out of 26 analysts covering the stock, 15 have a “Strong Buy” rating, nine have a “Hold” rating, one has a “Moderate Sell” rating, and one has a “Strong Sell” rating.

www.barchart.com

www.barchart.com On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

While the Stock Market Was Rallying, Palantir Stock Sold Off. Should You Buy the Dip in PLTR? Dear IBM Stock Fans, Mark Your Calendars for April 22 ConocoPhillips vs. EOG: 1 of These Energy Stocks Is Cheaper and Pays You More. Which One? Should You Buy, Sell, or Hold Palantir Stock Amid Trump Praise?