Silicon Motion Technology Corporation SIMO and Micron Technology, Inc. MU are key players in the broader technology hardware ecosystem. Silicon Motion is a leading developer of microcontroller ICs for NAND flash storage devices. The semiconductor company also designs, develops and markets high-performance, low-power semiconductor solutions for original equipment manufacturers (OEMs) and other customers.

Micron offers high-performance memory and storage technologies, including Dynamic Random Access Memory (DRAM), NAND flash memory, NOR Flash, 3D XPoint memory and other technologies. It is expanding its foothold in the solid-state drive (SSD) storage market as the emergence of thinner laptops and tablets over the past few years has created ideal market conditions for SSDs. Furthermore, secular growth of digital data, modest growth in TAM and higher demand for storage will likely drive growth for SSDs.

Let us delve a little deeper into the companies’ competitive dynamics to understand which of the two is relatively better placed in the industry.

The Case for SIMO

Silicon Motion has established itself as the leading merchant supplier of client SSD (solid state drive) controllers to module makers, including most market leaders in the United States, Taiwan and China. The company believes that it is well-equipped to adapt to industry changes as it has collaborated with flash vendors for developing proprietary controller technology to overcome the existing weakness of 3D NAND and outshine peers. Silicon Motion has commenced initial sales of 3D SSD controllers to flash partners. It expects this controller to be a significant SSD controller growth driver for the next year, as NAND Flash partners’ 3D capacity expands.

Silicon Motion operates a fabless business model, focusing on chip design while outsourcing manufacturing to foundries like TSMC. Consequently, the company has a low capital investment requirement as it does not require expensive fabrication plants, enabling it to adopt advanced manufacturing nodes quickly, leading to higher margins compared to integrated manufacturers. This, in turn, enables the company to focus on innovation and product development rather than manufacturing complexity. The key growth drivers for SIMO include AI and high-performance computing, cloud data centers, automotive storage, smartphones and mobile devices. Each of these end markets is growing fast and offers lucrative growth potential. Over the past 10 years, the company has shipped more than 5 billion controllers cumulatively – more than any other company in the world. Silicon Motion ships more than 750 million NAND controllers on average every year.

However, sluggishness in the global economy is likely to weigh on the company’s wireless and broader semiconductor market. The demand for PCs and smartphones in the end market continues to be soft as numerous suppliers are focusing on reducing their inventory levels. The near-term price fluctuation in the PC market remains a concern. Silicon Motion continues to acquire a large number of companies. While this improves revenue opportunities, business mix and profitability, it adds to integration risks. Moreover, the semiconductor industry is highly dynamic as it is prone to swift technological changes, stiff competition from evolving industry standards and declining average selling prices.

The Case for Micron

Micron is capitalizing on the AI boom with its HBM solutions, which are increasingly being adopted by major hyperscalers and enterprise customers. On the second-quarter fiscal 2026 earnings call, the company highlighted strong customer interest in its HBM portfolio, which is expected to drive substantial revenue growth in the quarters ahead. Micron’s HBM portfolio is generating multi-billion-dollar quarterly revenues. Micron is poised to be the key beneficiary of surging AI-related infrastructure spending, as companies continue to build out GPU clusters and AI data centers that require advanced memory solutions.

Micron is witnessing a strong demand for memory chips in the data center end market with a healthy inventory improvement across other markets, such as automotive, industrial and others. DRAM pricing is anticipated to keep increasing in the near term, which will further boost Micron’s revenue growth. The pricing benefits are likely to be driven by rising AI server demand, causing a scarcity in the availability of cutting-edge DRAM supplies.

However, Micron faces competition from Samsung Electronics Co., Ltd., SK Hynix Inc., Spansion Inc. and Toshiba Corporation in the semiconductor memory market. Wafer capacity increases from its competitors could disrupt DRAM and NAND supply dynamics, affecting prices and the company’s results. Moreover, heightening trade tension might compel many Chinese companies to buy chips from Samsung and other non-American chipmakers, consequently dumping Micron. Ramped-up production of domestic memory chips in China can also seriously jeopardize Micron’s prospects going forward. Changxin Memory Technologies has unveiled China's first domestically designed DRAM chip. Yangtze Memory Technologies is likely to start manufacturing NAND flash memory to challenge Samsung, Toshiba, Western Digital and Micron.

How Do Zacks Estimates Compare for SIMO & MU?

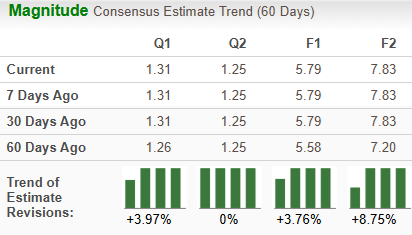

The Zacks Consensus Estimate for Silicon Motion’s 2026 sales indicates a year-over-year rise of 43%, while that for EPS suggests growth of 63.1%. The EPS estimates have been trending northward (up 3.8%) over the past 60 days.

Image Source: Zacks Investment Research

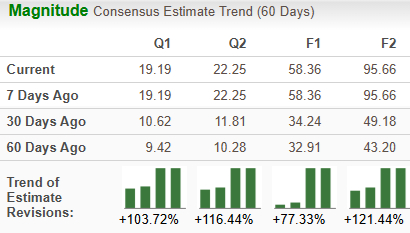

The Zacks Consensus Estimate for Micron’s fiscal 2026 sales implies year-over-year growth of 194.4%, while that of EPS suggests an improvement of 604%. The EPS estimates have trended up 77.3% over the past 60 days.

Image Source: Zacks Investment Research

Price Performance & Valuation of SIMO & MU

Over the past year, Silicon Motion has gained 204.9% compared with the industry’s growth of 123.5%. Micron has surged 492.2% over the same period.

Image Source: Zacks Investment Research

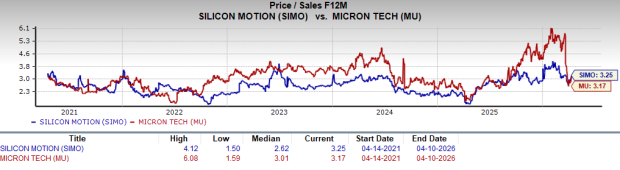

Silicon Motion looks slightly more expensive than Micron from a valuation standpoint. Going by the price/sales ratio, SIMO’s shares currently trade at 3.25 forward sales, higher than Micron’s 3.17.

Image Source: Zacks Investment Research

SIMO or MU: Which is a Better Pick?

Silicon Motion carries a Zacks Rank #3 (Hold), while Micron sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Both Silicon Motion and Micron expect sales and earnings to increase in the current fiscal year. In terms of price performance, Micron has outperformed SIMO. MU has exhibited better estimate revisions than SIMO and is trading relatively cheaply in terms of valuation. With a superior Zacks Rank and favorable metrics, Micron seems to hold a slight competitive edge over Silicon Motion and is therefore a better investment option at the moment.

Quantum Computing Stocks Set To Soar

Artificial intelligence has already reshaped the investment landscape, and its convergence with quantum computing could lead to the most significant wealth-building opportunities of our time.

Today, you have a chance to position your portfolio at the forefront of this technological revolution. In our urgent special report, Beyond AI: The Quantum Leap in Computing Power , you'll discover the little-known stocks we believe will win the quantum computing race and deliver massive gains to early investors.

Access the Report Free Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Micron Technology, Inc. (MU): Free Stock Analysis Report

Silicon Motion Technology Corporation (SIMO): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).