The AI infrastructure stocks remain one of the market’s hottest themes, and cloud companies tied to artificial intelligence have been among the biggest beneficiaries. As demand for compute capacity continues to surge, investors have been rewarding firms that can help power the next wave of AI growth. CoreWeave (CRWV) has been one of the names riding that momentum.

Now, however, CRWV stock has a specific date to watch. On April 14, CoreWeave plans to close two major debt offerings, including senior notes and convertible notes, as it looks to raise capital to support growth and repay existing obligations. The company recently priced a $1.75 billion private offering of 9.750% senior notes due 2031, a larger deal than originally announced, underscoring both its rapid expansion and its ongoing need for financing.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

For investors following the AI cloud space, here is what CRWV stock fans should know heading into April 14.

CoreWeave Rides Surge in AI Cloud Demand

CoreWeave, backed by the chip giant Nvidia (NVDA), is one of the discussed names in the AI cloud market. On one hand, it is a fast-growing cloud provider built for AI workloads, with huge GPU and CPU capacity that leading AI labs and enterprises use to train and run models. On the other hand, it is still a young business, deeply unprofitable, and heavily dependent on major contracts to keep its growth story alive.

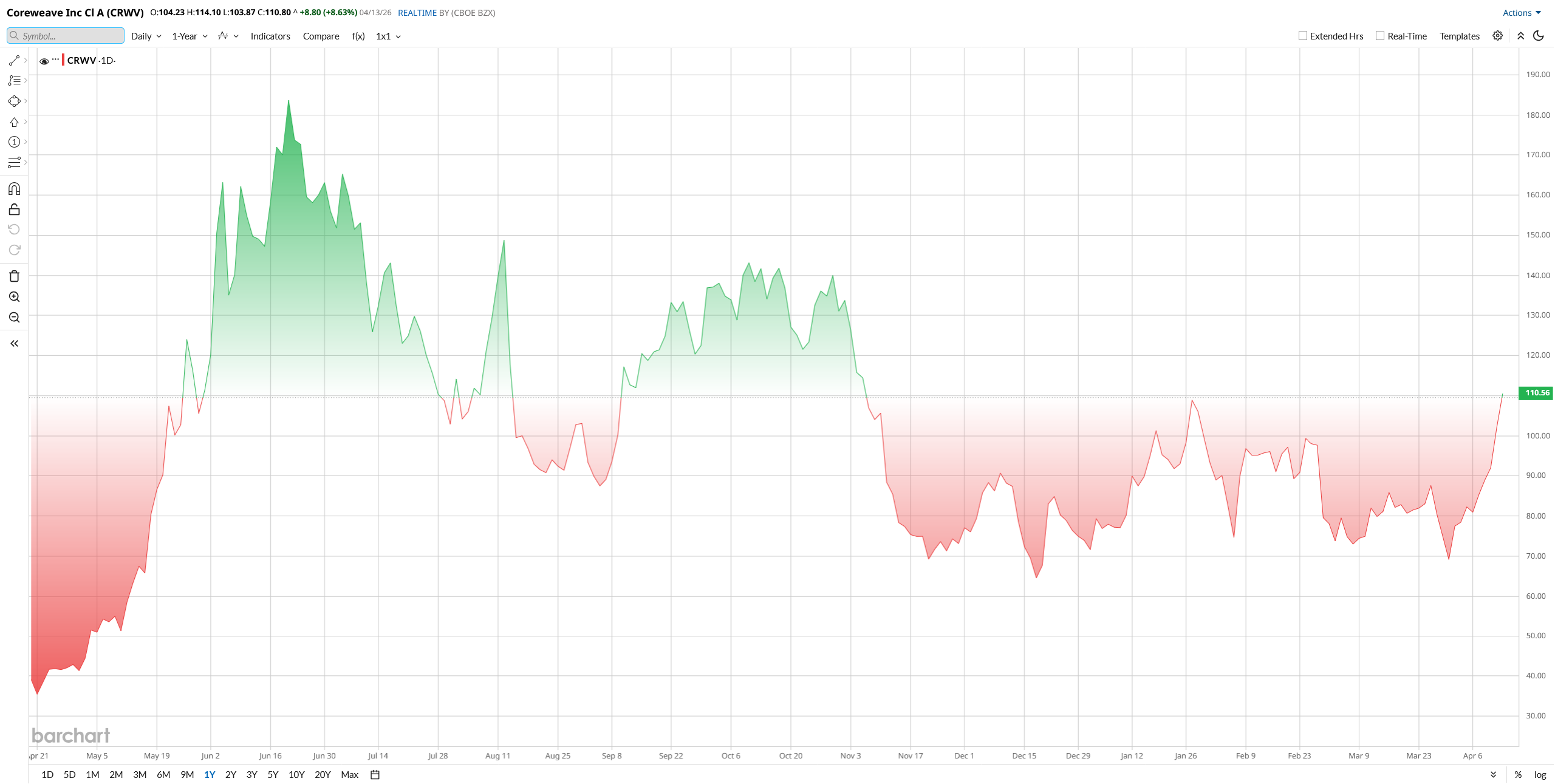

That matters because CRWV has already had a huge run. The stock is up well over 150% over the past year and has climbed roughly 54% just in 2026. Momentum has been lifted by massive new deal announcements with Meta (META) and Anthropic. But the stock is also expensive, and investors are clearly paying up for future growth rather than current earnings.

CRWV does not look cheap. The stock trades at about 7.5 times sales and 10.7 times book value. Those are high numbers for a company that is still losing money. In simple terms, the market is betting that CoreWeave can keep growing fast enough to justify the price.

That is a big ask. The stock has strong momentum, but it is already priced for a lot of success. If growth slows, the valuation could become a problem quickly.

www.barchart.com

www.barchart.com CoreWeave's Business Is Growing Fast, but Losses Are Still Wide

The latest quarter showed why investors are excited. In Q4 2025, CoreWeave posted revenue of $1.57 billion, up 110% from a year earlier. Full-year revenue reached $5.13 billion, up 168% year-over-year (YoY). Management said 2025 was a defining year, and the company also finished the year with a massive $66.8 billion backlog.

That backlog is important. It gives CoreWeave visibility into future demand. It also indicates that the company is building a real business, not just chasing short-term hype.

Still, the profit picture remains weak. CoreWeave posted a net loss of $452 million in the quarter. It also spent heavily on data centers and infrastructure. Operating cash flow was strong, but capital spending was even larger, which left free cash flow deeply negative. In short, CoreWeave is growing fast, but that growth is expensive.

The company is not slowing down. CoreWeave expects Q1 2026 revenue of $1.9 billion to $2.0 billion. For the full year, it is guiding for $12 billion to $13 billion in revenue and up to $1.1 billion in adjusted operating income.

That is an aggressive target. It suggests management believes demand for AI compute is still rising fast. The company is also financing its expansion through debt and equity raises, which makes the April 14 debt closing an important date for investors to watch.

Big Deals Keep CoreWeave in the Spotlight

CoreWeave has stayed busy in 2026, and the new deals show just how fast the company is scaling. On April 9, it announced a $21 billion multi-year AI cloud expansion with Meta through 2032. The very next day, it unveiled a multi-year agreement with Anthropic to power the new Claude models. Nine of the top ten AI labs now run on CoreWeave, the company notes.

Meanwhile, S&P recently raised CoreWeave’s credit outlook to positive (already rated B/B+) on its scale and backing. All of these developments, plus the April funding round, show how CoreWeave is racing to keep up with explosive AI demand.

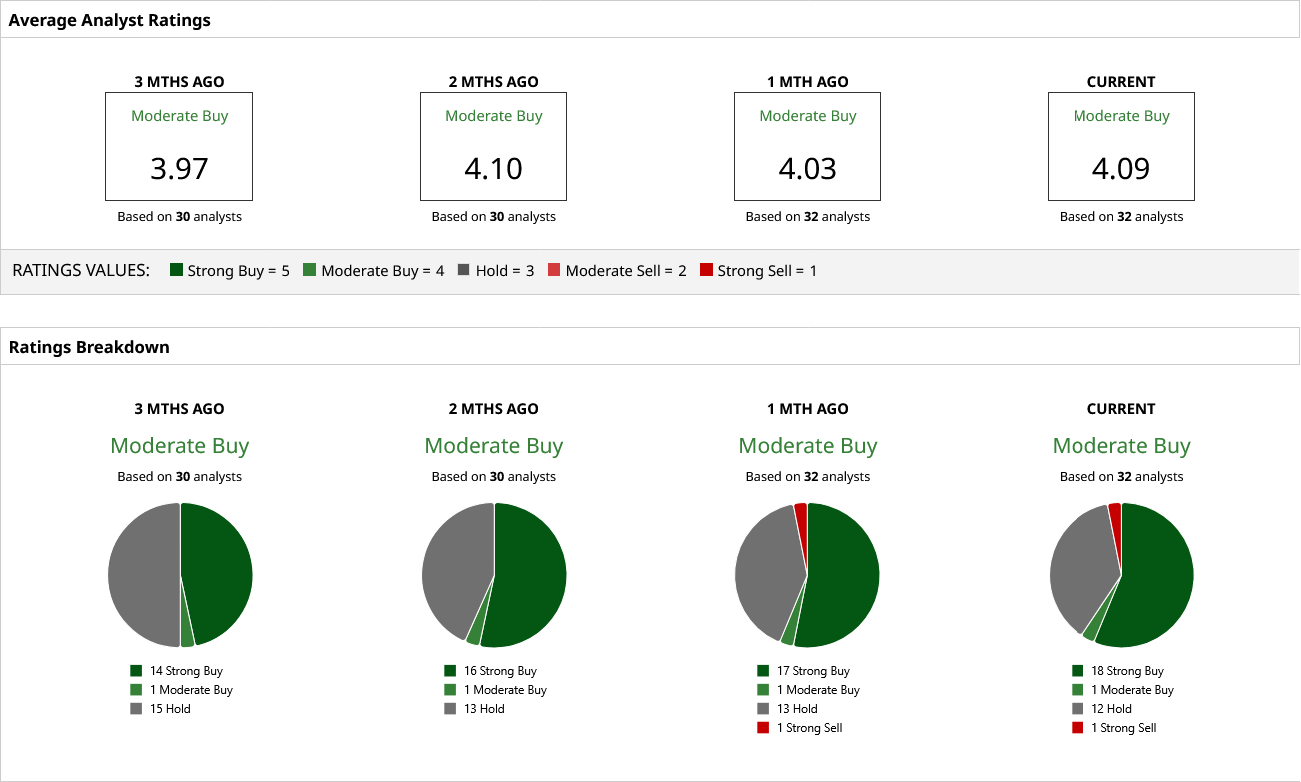

What Do Analysts Think of CRWV Stock?

Wall Street is positive but not overly excited. CRWV stock carries a consensus “Moderate Buy” rating, with an average 12-month price target near $117, implying roughly 6% upside from current levels.

Morgan Stanley’s Keith Weiss recently initiated coverage with a “Hold” rating and a $99 target, citing execution risks, while Goldman Sachs analyst Gabriela Borges maintains a “Neutral” stance with an $86 target due to valuation concerns.

On the bullish side, Evercore ISI rates the stock “Outperform” with a $120 target, supported by the Meta deal, and Cantor Fitzgerald initiated with an “Overweight” rating and a $149 target, pointing to AI-driven growth and the Anthropic partnership.

Likewise, Bank of America’s Tal Liani also upgraded the stock to “Buy” with a $100 target, highlighting its strong positioning in AI workloads.

www.barchart.com

www.barchart.com On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

On Semiconductor Pops on Analyst Upgrade. Should You Buy ON Stock Here? A $21 Billion Reason to Buy CoreWeave Stock Now Oracle (ORCL) Stock May Be Priced at a Genuine Discount As Waymo Launches in Nashville, Should You Buy, Sell, or Hold GOOGL Stock?