Shopify SHOP shares closed at $114.97 on Monday, which was 36.9% lower than the 52-week high of $182.19 it hit on Oct. 29. SHOP shares have dropped 28.6% year to date, underperforming the broader Zacks Computer and Technology sector’s decline of 1.4%. So, does the pullback offer a buying opportunity for investors? Let’s find out.

SHOP Shares Are Trading at a Premium

Shopify is significantly overvalued, as suggested by a Value Score of F. In terms of the forward 12-month price/sales (P/S), SHOP is currently trading at 9.71X compared with the broader sector’s 6.06X. Shopify shares are pricey compared with Amazon AMZN, Wix.com WIX and Commerce.com CMRC. Shares of Amazon, Wix.com and Commerce.com are trading at P/S multiples of 3.16, 2.16 and 0.90, respectively.

SHOP Stock’s Valuation

Image Source: Zacks Investment Research

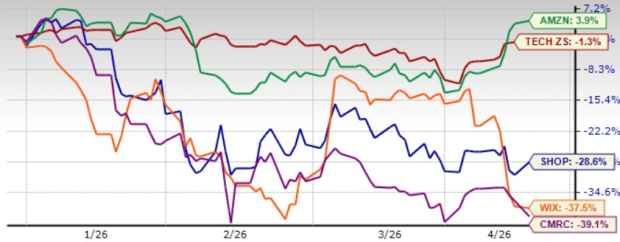

In terms of share price performance, Shopify has underperformed Wix.com and Commerce.com year to date but lags Amazon. While Amazon shares returned 3.9%, Wix.com and Commerce.com dropped 37.5% and 39.1%, respectively.

Shopify is facing stiff competition from Amazon, which dominates the U.S. e-commerce market, driven by its “Buy with Prime” service, which combines its payments and fulfillment services and makes them available at checkout on other websites while promising faster delivery for Prime members. AI integration across operations is enhancing personalization, logistics and AWS offerings, strengthening its competitive positioning. Wix is gaining momentum in its core business, driven by solid performance from new user cohorts, while Commerce.com’s strategy to provide flexible, enterprise-grade subscription solutions is expected to drive recurring base revenues.

SHOP Stock’s Price Performance

Image Source: Zacks Investment Research

SHOP’s 2026 Earnings Estimates Revisions Are Steady

Shopify’s near-term performance is expected to suffer from modest earnings growth given gross margin headwind, a challenging macroeconomic condition and stiff competition. The company’s gross margin is suffering from a higher mix of low-margin Merchant Solutions revenues and the negative impact of rapid Payments penetration.

The Zacks Consensus Estimate for SHOP’s 2026 earnings is currently pegged at $1.78 per share, unchanged over the past 30 days and indicating year-over-year growth of 52.14%. The consensus mark for SHOP’s 2026 revenues is currently pegged at $14.55 billion, implying a year-over-year rally of 25.87%.

Shopify Inc. Price and Consensus

Shopify Inc. price-consensus-chart | Shopify Inc. Quote

AI Push & International Expansion to Aid Shopify’s Prospects

Shopify hosts a data trove thanks to an expanding merchant base and a growing number of transactions. This whopping amount of data is helping Shopify offer better shopping experiences to merchants and eventually their customers. The company is leveraging agentic commerce to boost shopper experience, beginning with product discovery to conversation and finally checkout through tools like Catalog (product discovery), Universal Cart and Checkout Kit.

Shopify’s AI-powered post-purchase tools are helping merchants build long-term, durable relationships with shoppers. Growing adoption of Sidekick, Shopify’s on-platform intelligent assistant, reflects the company’s expanding footprint among AI-first merchants. The company’s AI partnership with Google establishes a standard for AI-driven commerce, which enables merchants to keep control of checkout logic. SHOP has expanded integrations, enabling merchants to sell across ChatGPT, Google AI Mode/Gemini and Microsoft Copilot.

Shopify is benefiting from strong subscription revenues, driven by reliable plans and loyal users, reducing revenue volatility. The growing contribution from Plus is significant, as these higher-tier merchants deliver stronger Gross Merchandise Volume (“GMV”) per merchant, multi-store needs and long-term stickiness. This is a sign that the company is scaling existing merchants and adding larger merchants. In the fourth quarter of 2025, Monthly Recurring Revenues (“MRR”) increased 15%, supported by continued growth across standard, Plus and offline, wherein Plus represented roughly 34% of MRR.

Shopify’s growing international footprint is a key catalyst. SHOP has been expanding localized payment options, language capabilities and cross-border commerce tools to make its platform more accessible globally. Shopify Payments has been expanded to 60 new countries, Shopify Capital is now available in eight countries, and Managed Markets 2.0 enables faster international payouts and broader payment method support. These capabilities allow businesses to sell internationally while managing compliance, payments and logistics through SHOP’s integrated ecosystem. International growth has been broadly balanced between new merchant acquisitions and expanded activity from existing merchants, suggesting engagement is deepening organically.

Conclusion

Shopify is expected to suffer from gross margin headwind and stiff competition in the near term. However, AI infusion and expanding international footprint bode well for the company’s long-term prospects. These factors justify Shopify’s premium valuation.

Shopify currently has a Zacks Rank #2 (Buy), which implies that investors should start accumulating the stock right now. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. Little-known AI firms tackling the world's biggest problems may be more lucrative in the coming months and years.

SeeWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Amazon.com, Inc. (AMZN): Free Stock Analysis Report

Wix.com Ltd. (WIX): Free Stock Analysis Report

Shopify Inc. (SHOP): Free Stock Analysis Report

Commerce.com, Inc. (CMRC): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).