Most tech companies have fallen victim to this year’s selling pressure. High-growth names faced valuation resets, amplified by concerns around AI spending sustainability and a rotation into defensives.

But one stock is quietly delivering consistent outperformance, even when the broader technology landscape feels unsettled. Jabil, a key AI infrastructure company, has stood out as a notable exception in 2026.

Through early April, Jabil shares have advanced roughly 20% year-to-date, meaningfully outperforming the weaker performance of the broader indexes. Over the trailing 12 months, the stock is up more than 125%, a testament to the company’s ability to navigate cycles with resilience and strategic focus.

Image Source: StockCharts

Why Jabil is Bucking the Trend

This outperformance is not accidental. Jabil has evolved from a traditional contract manufacturer into a diversified, high-margin partner for some of the world’s most demanding end-markets. The company serves as a critical hardware partner in the AI data center supply chain, manufacturing the physical infrastructure required to run high-performance AI models.

Its success in 2026 reflects the power of a broad portfolio that spans AI infrastructure, healthcare, regulated industries, and advanced automation — areas that have proven more durable than pure consumer electronics amid economic caution.

In our experience, companies that can pivot toward secular growth drivers while maintaining operational discipline often reward patient investors during periods when the market favors caution over speculation. Jabil fits that profile exceptionally well.

Jabil reported its fiscal Q2 results last month, extending its long track record of exceeding estimates and reinforcing its leadership position. The company posted net revenue of $8.3 billion, up 23% year-over-year and comfortably ahead of consensus expectations of approximately $7.8 billion. Adjusted EPS reached $2.69, beating estimates of $2.54 and reflecting a 38.7% increase from the prior year.

Management responded with meaningful upward revisions to full-year fiscal 2026 guidance. Revenue is now projected at $34 billion (up from the prior $32.4 billion), while core EPS is expected at $12.25 (up from $11.55).

These raises reflect increasing confidence in the back half of the year, particularly in AI data center infrastructure, healthcare, and advanced warehouse/retail automation. In our view, the ability to raise guidance amid a cautious macro backdrop speaks volumes about Jabil’s visibility and execution capabilities.

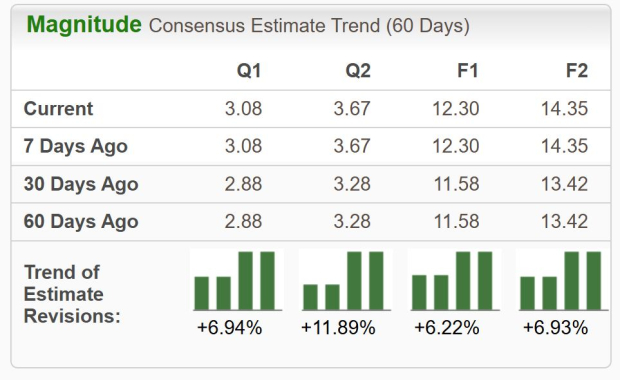

The Zacks Rundown

Jabil currently carries a Zacks Rank #2 (Buy), supported by positive estimate revisions and strong momentum in its growth segments. Consensus estimates for fiscal 2026 are in line with the recent raises from management, with analysts continuing to nudge numbers higher in recent weeks:

Image Source: Zacks Investment Research

What makes Jabil’s story particularly sincere is its strategic evolution over the past several years. The 2024 divestiture of its low-margin mobility business was a pivotal move that sharpened focus on higher-value segments. Today, Jabil serves as a critical manufacturing and engineering partner for leading players in AI hardware, GLP-1 injector pens (a major healthcare growth driver), capital equipment, and automation solutions.

This diversification has reduced cyclicality compared to pure-play consumer electronics manufacturers. In an environment where many tech names have faced questions around growth deceleration, Jabil’s exposure to structural secular drivers has provided a buffer and a growth engine.

The AI tailwind is especially meaningful. Jabil’s Intelligent Infrastructure segment, which includes data center racks, liquid cooling systems, and related assemblies, has seen explosive demand as hyperscalers and enterprises accelerate their AI deployments.

Management highlighted that AI-related revenue grew 46% year-over-year in the latest quarter, and the raised full-year guidance reflects confidence that this momentum will persist. In addition, the company’s strong free cash flow generation supports continued share repurchases and dividend growth, adding to total shareholder returns.

Bottom Line

Jabil’s geographic diversification, long-term customer relationships, and focus on higher-value segments provide meaningful buffers. The company’s track record of operational discipline and strategic portfolio management offers assurance that it can navigate near-term uncertainties while capitalizing on multi-year opportunities.

In 2026, while many tech names have faced headwinds, Jabil has quietly compounded value through diversification, execution, and exposure to enduring secular trends in AI and healthcare. The stock’s ability to buck the negative trend this year may signal not just near-term strength, but the potential for sustained outperformance as these tailwinds gain further momentum.

Disclosure: Jabil JBL is a long-term holding in the Zacks Headline Trader portfolio.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Jabil, Inc. (JBL): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).