EMCOR Group, Inc.’s EME Network and Communications segment has emerged as a primary engine of long-term visibility, with Remaining Performance Obligations (RPOs) surging to a record $4.46 billion—an increase of $1.65 billion, or nearly 60% year over year. This scale is particularly notable, as the segment’s RPO alone now exceeds EMCOR’s total company-wide backlog at the end of 2019, which stood at approximately $4.036 billion. Since then, high-tech manufacturing and network-related markets have delivered a compound annual growth rate of 48%, highlighting a structural shift from a strong data center business to a significantly more robust growth engine.

The primary driver for this surge is the sustained capital investment from large data center customers building next-generation digital infrastructure. EMCOR has established a differentiated national footprint, operating across approximately 17 electrical and seven mechanical markets, with nationwide fire life safety capabilities. Importantly, the shift toward AI-driven data centers is increasing project complexity, with mechanical scope often expanding by 1.5x to 2x, creating a meaningful incremental growth lever.

Looking ahead, management expressed strong confidence in revenue visibility over the next two to three years. Total RPO reached $13.25 billion in 2025, up 31% year over year, reflecting broad-based demand across diverse end markets. This balanced exposure supports resilience, with strength in technology and industrial segments offsetting softer commercial activity. At the same time, the strategic acquisition of Miller Electric continues to enhance capabilities in complex, high-growth project areas. Supported by advanced Virtual Design and Construction and prefabrication capabilities, EMCOR is well-positioned to convert its backlog into sustained revenue and earnings growth.

While execution remains key—particularly given the scale and complexity of these projects—the record RPO level signals a more durable growth profile. With a strong pipeline and multi-year project commitments in place, EMCOR appears well-positioned to sustain momentum, supporting both revenue growth and earnings visibility over the medium term.

EMCOR’s Competitive Landscape: Visibility and Scale in Focus

EMCOR Group operates in a highly competitive infrastructure and mission-critical construction market, competing with established peers such as Sterling Infrastructure, Inc. STRL and Quanta Services, Inc. PWR. These companies are similarly benefiting from strong demand tied to data centers, electrification and large-scale infrastructure investment, though their execution models and backlog visibility differ.

Sterling continues to demonstrate strong operational momentum, driven by its E-Infrastructure and Transportation segments. In the fourth quarter, the company delivered robust growth in both revenues and adjusted operating income, supported by solid execution, organic expansion and successful integration of acquisitions. Adjusted EBITDA rose 70% year over year to $142.1 million, while gross margin improved to a record 21.7%, reflecting a more favorable project mix and enhanced efficiency—positioning Sterling as a formidable competitor in data center-related site development.

Quanta, by contrast, maintains a leading position in electrical infrastructure, with deep capabilities in transmission, distribution and grid modernization. Similar to EMCOR, the company is benefiting from secular tailwinds such as AI-driven data center expansion and rising power demand. Quanta reported gross profit of $1.22 billion in the fourth quarter, up from $1.06 billion a year earlier, supported by higher volumes and disciplined project execution.

EME Stock’s Price Performance & Valuation Trend

Shares of this Connecticut-based infrastructure service provider have gained 19.1% in the past six months, underperforming the Zacks Building Products - Heavy Construction industry, but outperforming the Construction sector and the S&P 500 Index.

Image Source: Zacks Investment Research

EME stock is currently trading at a premium compared with the industry peers, with a forward 12-month price-to-earnings (P/E) ratio of 27.77, as evidenced by the chart below.

Image Source: Zacks Investment Research

Earnings Estimate Revision of EME

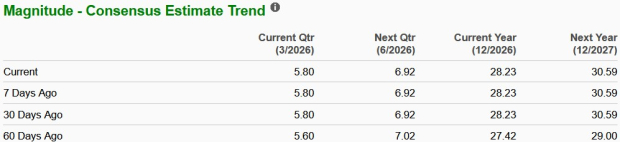

EME’s earnings estimates for 2026 and 2027 have moved upward in the past 60 days. The estimates for 2026 and 2027 imply year-over-year growth of 9.1% and 8.3%, respectively.

Image Source: Zacks Investment Research

EMCOR stock currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Quantum Computing Stocks Set To Soar

Artificial intelligence has already reshaped the investment landscape, and its convergence with quantum computing could lead to the most significant wealth-building opportunities of our time.

Today, you have a chance to position your portfolio at the forefront of this technological revolution. In our urgent special report, Beyond AI: The Quantum Leap in Computing Power , you'll discover the little-known stocks we believe will win the quantum computing race and deliver massive gains to early investors.

Access the Report Free Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Quanta Services, Inc. (PWR): Free Stock Analysis Report

EMCOR Group, Inc. (EME): Free Stock Analysis Report

Sterling Infrastructure, Inc. (STRL): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).