Gartner Inc. IT is benefiting from its diverse offerings across domains, reducing reliance on single revenue streams and ensuring a stable top line. Its rich domain expertise and technology-related insights, which help clients maximize returns on capital investments, enable IT to charge a premium for the services. Strong shareholder-friendly policies are an added advantage.

However, higher talent costs, foreign exchange risk and heightened competition within the consulting services industry put pressure on profitability and scalability.

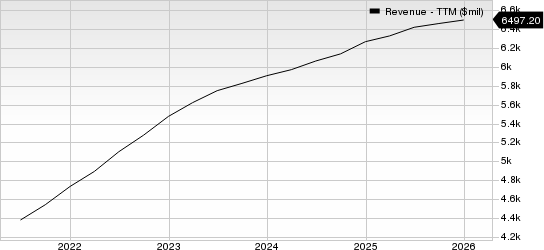

How Is IT Faring?

Gartner offers a comprehensive services portfolio, using advanced technologies to collect and analyze troves of data, providing key insights and decision-support solutions to enable informed decision-making. These insights are typically drawn from a critical fact base, a collection of verified and structured information and collated from interactions with clients in more than 15,000 distinct organizations worldwide.

The company’s wide range of products and services results in low customer concentration, mitigating operating risks and increasing operational efficiency. Its differentiated product portfolio and integrated research and consulting team give the company a competitive advantage against the rivals. Gartner creates and distributes broader proprietary research content via published reports, interactive tools, facilitated peer networking, briefings, consultancy and advisory services and events, facilitating a steadily improving revenue stream for itself.

Gartner, Inc. Revenues (TTM)

Gartner, Inc. revenue-ttm | Gartner, Inc. Quote

The company's timely, thought-provoking and comprehensive analysis of unbiased, pragmatic and actionable insights offers huge value to its customers by helping them save thousands of dollars through in-depth research. The industry’s dynamic and complex nature drives the growth of Gartner’s research and consultancy services to support higher productivity, improve performance metrics and protect the enterprise from cybersecurity threats, allowing it to charge a premium for the services.

Gartner consistently rewards its shareholders through share repurchases. It repurchased shares worth $2 billion, $700 million, $600 million and $1 billion in 2025, 2024, 2023 and 2022, respectively. Such moves indicate the company’s commitment to return value to its shareholders and instill their confidence in the business.

Meanwhile, Gartner faces significant competition from electronic and print media companies, as well as consulting firms. This competition fuels innovation across the industry while driving pricing pressures. The requirement to invest in technology increases the difficulty in balancing growth and profitability with its competitors.

IT has been witnessing higher costs due to a competitive talent market. While advancements in automation and AI offer massive opportunities to the industry, these technologies enable clients to improve performance with in-house tools, thereby creating uncertainty for consulting services firms.

The company’s global presence makes it vulnerable to foreign exchange risk. Thus, appreciation or depreciation of the U.S. dollar compared with foreign currencies such as the British pound, euro, Canadian dollar, Australian dollar and Japanese yen could impact the company's financial results.

Recently, IT reported impressive fourth-quarter 2025 results. It earned an adjusted profit of $3.94 per share, which beat the Zacks Consensus Estimate by 12.6% but decreased 27.7% from the year-ago quarter. Revenues of $1.8 billion missed the consensus estimate by a slight margin and rose 2.2% year over year.

Gartner currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Earnings Snapshots of Some Players

Waste Connections, Inc. WCN reported impressive fourth-quarter 2025 results.

WCN's adjusted earnings (excluding 28 cents from non-recurring items) of $1.29 per share marginally beat the Zacks Consensus Estimate and increased 11.2% year over year. Waste Connections’ revenues of $2.4 billion met the consensus estimate and grew 5% from the year-ago quarter.

Equifax Inc. EFX posted impressive fourth-quarter 2025 results.

EFX's adjusted earnings were $2.09 per share, outpacing the Zacks Consensus Estimate by 2.5% but declining 1.4% from the year-ago quarter. Equifax’s total revenues of $1.6 billion surpassed the consensus estimate by 1.3% and grew 9.2% on a year-over-year basis.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the #1 favorite stock to gain +100% or more in the coming year. While not all picks can be winners, previous recommendations have soared +112%, +171%, +209% and +232%.

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor.

Today, See These 5 Potential Home Runs >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Equifax, Inc. (EFX): Free Stock Analysis Report

Gartner, Inc. (IT): Free Stock Analysis Report

Waste Connections, Inc. (WCN): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).