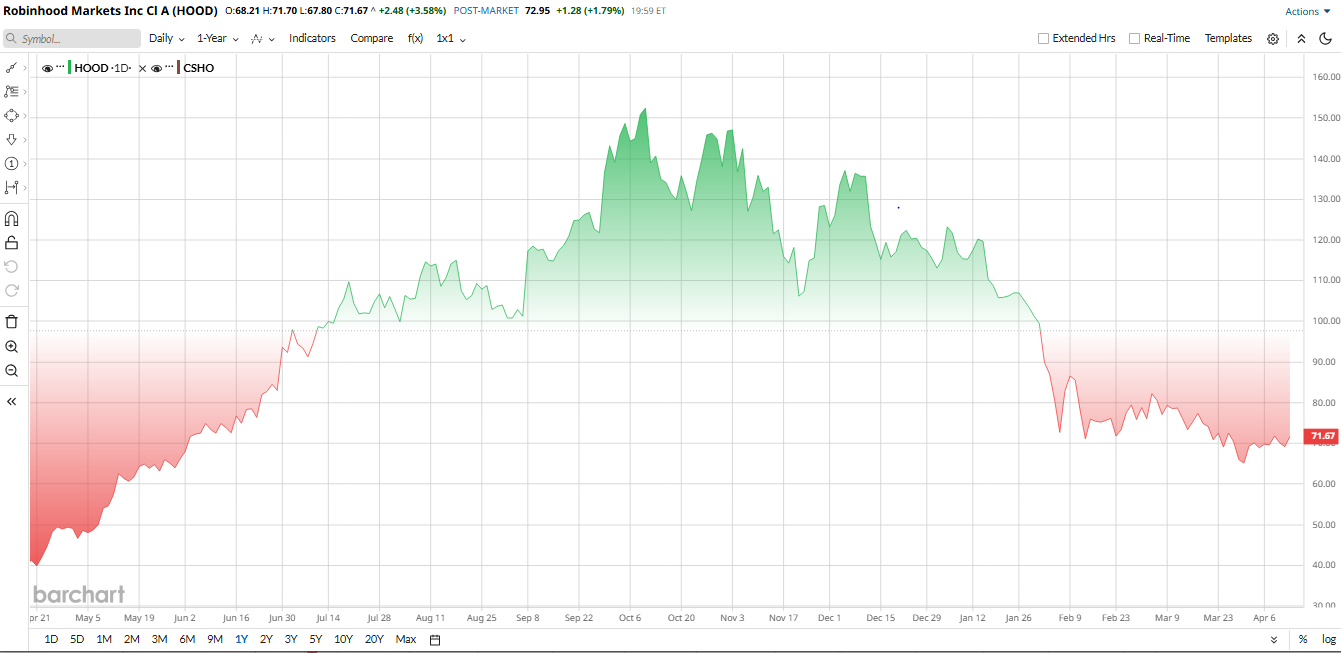

Robinhood Markets (HOOD) is not operating in an easy fintech environment right now. Retail traders are cautious, crypto trading volume has cooled, and the stock has shed 23% of its value year-to-date (YTD). Investors have taken a "risk off" attitude, fleeing to safety in energy and semiconductors while leaving growth names like Robinhood at multi-year lows. Now, Cathie Wood’s Ark Invest is doubling down, buying 182,641 shares worth about $12.74 million last week, even as the broader market yawns.

That is not automatically a buy signal, but it does add a layer of conviction around a stock that could use some positive news. The key question for investors is whether Wood is seeing a value inflexion point that the rest of the market is missing, or if this is just another case of catching a falling knife.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Robinhood Stock’s Wild Ride

Despite the recent pullback, HOOD stock has had a wild ride, gaining roughly 98% over the past year. These gains came alongside record profitability and expansion beyond just brokerage services.

From a valuation perspective, Robinhood stock looks significantly overvalued compared to traditional financial sector peers. Robinhood has a market capitalization of around $71 billion. HOOD stock trades at a price-to-book ratio of about 7 times, which is vastly higher than the sector median of 1.3 times. That suggests the market is still pricing in a strong growth trajectory, and it leaves little room for execution missteps. In a market where investors are fleeing expensive growth names, this premium is a big reason the stock has been a falling knife.

www.barchart.com

www.barchart.com Why Ark Invest's Purchase Matters for Robinhood

On one hand, Robinhood is a giant platform with more than 25 million funded accounts and a brand that resonates with younger investors. On the other hand, the business is tied closely to market volatility and crypto sentiment, two things that are notoriously hard to predict.

This matters because HOOD stock has already been punished by bearish momentum. If Wood’s bet is based on the company’s strong underlying growth and new product pipeline rather than just a short-term trading bump, it signals a longer-term opportunity.

The Business Is Still Growing, But Sentiment Has Turned Negative

Still, it is important not to overstate the near-term damage. Robinhood’s latest quarter was neither a blowout nor a disaster. In the fourth quarter of 2025, net revenue came in at $1.28 billion, up 27% year-over-year (YOY), while total net revenues for the full year surged 52% to $4.5 billion.

That is clearly impressive growth, especially when you consider forward revenue growth of 22%, which considerably outpaces the sector median of 8%. Profitability is not an issue here, either. The company’s net income margin sits at a healthy 42%, which is significantly higher than the sector median.

Robinhood is still a functioning growth machine with the financial capacity to invest heavily in its future, even if the stock's momentum is negative.

Management Expands Product Push in 2026

The bigger story is what Robinhood is building next. In 2026, the company is rolling out new products to deepen engagement and grow revenue.

This includes the upcoming launch of Robinhood Legend for active traders and Cortex, an AI tool for research. Robinhood is also expanding into futures, index options, and banking, while pushing further into international markets. Finally, the company is working on newer ideas like Robinhood Chain and social features to keep users more engaged on the platform.

CEO Vlad Tenev’s goal is simple: turn Robinhood into a full financial app, not just a trading platform, and capture more of users’ financial activity.

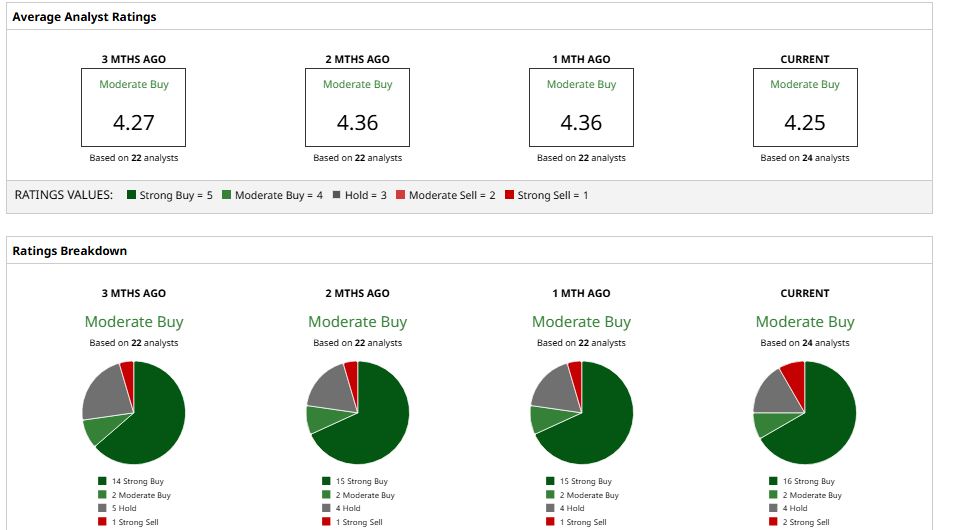

What Do Analysts Think of HOOD Stock?

Wall Street is somewhat divided on Robinhood, but the recent trend in revisions has been undeniably negative. In the past three months, analysts have made 16 downward revisions to EPS estimates compared to only two upward revisions. This suggests that, while the long-term story is intact, near-term expectations are being reset lower.

Goldman Sachs rates HOOD stock as a “Buy” and recently lowered its 12-month price target to $111 from $130. The firm believes the company has strong engagement metrics despite the recent volatility in net new assets.

Morgan Stanley is more cautious. The firm has an “Equal Weight” rating and a $95 target, noting that while the product roadmap is impressive, near-term headwinds in crypto and deposits could limit upside in the stock. Meanwhile, Bank of America is somewhat more upbeat, recently raising its target to $122.

Overall, Robinhood has a consensus “Moderate Buy” rating. The mean price target sits at $105.73, which implies roughly 21% potential upside from where HOOD stock trades today. Analysts see real potential upside if Robinhood’s expansion strategy gains traction, but the stock needs to prove it can overcome the negative momentum and justify that premium valuation.

www.barchart.com

www.barchart.com On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Should You Chase the Rally in SoundHound Stock Today? Cathie Wood Is Doubling Down on Robinhood Stock. Should You? Uber Stock Just Broke Above Its 50-Day Moving Average. Should You Chase the Rally? Macquarie Is Pounding the Table on CoreWeave Stock with a New ‘Outperform’ Rating. Should You Buy Here?