The global apparel industry is navigating a complex environment marked by cautious consumer spending, evolving fashion trends and growing emphasis on brand equity. Ralph Lauren Corporation RL and PVH Corp. PVH emerge as two prominent players in the global fashion industry.

While RL is benefiting from its iconic brand portfolio, product innovations and disciplined execution of its Next Great Chapter strategy, PVH is a brand-focused fashion group with strengths in its flagship brands. Both companies command extensive global reach, powerful brand portfolios and well-established distribution networks while pursuing distinct yet overlapping strategies to drive long-term growth.

In this face-off between Ralph Lauren and PVH, we examine how market share strength, competitive positioning and differences in business models shape long-term growth potential and defensive appeal.

The Case for RL

Ralph Lauren’s investment thesis is anchored in its strong brand equity, premium positioning and solid execution under its “Next Great Chapter” strategy. Its “Next Great Chapter: Drive Plan” remains the cornerstone of its growth strategy, focusing on consumer centricity and operational agility. Management continues to highlight the strength of its globally recognized lifestyle brand, spanning apparel and accessories, enabling the company to capture demand across multiple consumer segments and occasions.

The company is focused on driving full-price selling, supported by tighter inventory control and reduced promotional activity. It has been streamlining its assortment and sharpening its focus on core segments, while selectively expanding into high-growth categories such as womenswear, outerwear and handbags. This approach is helping reinforce its premium image and improve average unit retail.

Digital transformation and direct-to-consumer (DTC) expansion remain central to RL’s growth strategy. The company is accelerating its direct-to-consumer business, including both its physical stores and digital channels. This shift allows Ralph Lauren to have greater control over its brand presentation, customer experience and pricing. Investments in digital platforms, including newer channels like social commerce, are helping the company attract younger consumers and expand its global reach.

International markets, particularly Asia and Europe, remain key growth drivers for Ralph Lauren. By building strong consumer ecosystems in major markets, the company targets deepening customer engagement and sustainable international growth. It is leveraging localized assortments, marketing campaigns and strategic partnerships to further strengthen its presence across these regions. Overall, Ralph Lauren is focused on elevating its brand, maintaining disciplined distribution and expanding its DTC business, supporting long-term growth while reinforcing its premium positioning.

The Case for PVH

PVH’s strategy is built around its PVH+ plan, which focuses on brand strength, operational simplicity and higher-quality growth. The company is doubling down on its two global power brands, namely, Calvin Klein and Tommy Hilfiger, by elevating product quality, sharpening brand identity and driving consistent global messaging. It is seeing strength in Calvin Klein and Tommy Hilfiger brands, supported by product innovation, cultural campaigns and digital strength.

PVH has been strengthening its DTC and digital channels, both of which are central to its PVH+ Plan. The company has significantly enhanced its e-commerce capabilities and omnichannel execution, as it delivered continued growth in its owned and operated e-commerce business, particularly in the Americas and Asia Pacific, supported by strong consumer engagement and effective digital campaigns. Both Calvin Klein and Tommy Hilfiger are benefiting from a strategy that connects hero product innovation with high-impact global marketing and cultural partnerships. This approach is driving higher online traffic, stronger engagement and improved full-price sell-through across channels.

The company is also focused on simplifying its operating model. This includes streamlining its supply chain, reducing SKU complexity and exiting non-core businesses to improve efficiency and profitability. These efforts are designed to create a more agile organization with better cost control. PVH has made meaningful progress on its cost optimization and efficiency initiatives, with annualized cost savings through its Growth Driver 5 actions. The company also maintained a strong focus on inventory and supply-chain optimization.

International markets remain a major growth lever, particularly in Europe and the Asia Pacific, where PVH is expanding distribution, tailoring assortments and strengthening local relevance through targeted marketing. At its core, PVH’s strategy is a balanced mix of brand elevation, operational discipline and digital expansion. By focusing on fewer brands, stronger products and deeper consumer engagement, the company is positioning itself for profitable growth despite macro and tariff headwinds.

Price Performance & Valuation of RL & PVH

In the past year, Ralph Lauren has delivered superior returns, with shares skyrocketing 79% compared with PVH’s rally of 29.8%. Both companies have performed better than the Textile - Apparel industry’s 3.1% decline, demonstrating resilience in a challenging consumer backdrop, reflecting investor confidence in their defensive business strategies and global brand strength.

Image Source: Zacks Investment Research

From a valuation standpoint, RL currently trades at a forward price-to-earnings (P/E) multiple of 20.41X compared with PVH’s 7.21X. Here, PVH trades at a cheaper forward P/E multiple compared with Ralph Lauren.

Image Source: Zacks Investment Research

How Does Zacks Consensus Estimate Compare for RL & PVH?

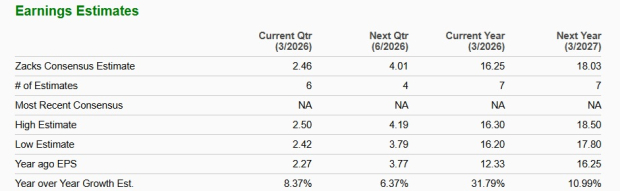

Ralph Lauren’s fiscal 2026 revenues and earnings per share (EPS) are projected to increase 12.4% and 31.8% year over year to $7.96 billion and $16.25 per share, respectively. RL’s fiscal 2027 revenues and EPS are likely to increase 6.5% and 11% year over year to $8.48 billion and $18.03 per share, respectively. The company has a strong track record of sales and earnings surprises.

Image Source: Zacks Investment Research

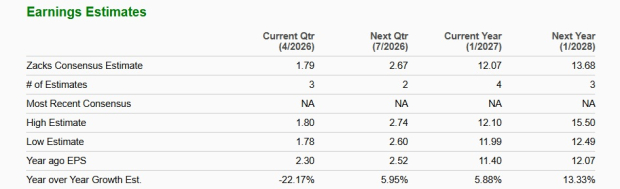

PVH Corp.’s fiscal 2026 revenues and EPS are expected to rise 1.1% and 5.9% year over year to $9.05 billion and $12.07 per share, respectively. PVH’s fiscal 2027 revenues and EPS are likely to jump 2.3% and 13.3% year over year to $9.25 billion and $13.68 per share, respectively.

Image Source: Zacks Investment Research

RL vs. PVH: Who Has the Edge?

In this fashion giant face-off, Ralph Lauren moves ahead, supported by stronger brand elevation, improving margin profile and disciplined execution. The company’s focused premium strategy, reduced promotional intensity and steady progress in direct-to-consumer channels are driving better earnings visibility and reinforcing investor confidence. With continued momentum in international markets and full-price selling, Ralph Lauren appears well-positioned to sustain its growth trajectory.

That said, PVH Corp. remains a strong contender. Its globally recognized brands, including Calvin Klein and Tommy Hilfiger, provide a solid foundation, while its ongoing transformation under the PVH+ plan supports long-term margin expansion and operational efficiency. Although execution risks remain, particularly amid macro uncertainty, PVH’s streamlined model and focus on higher-quality growth offer meaningful upside potential.

For investors prioritizing brand strength, financial resilience, earnings visibility and higher investor returns, Ralph Lauren takes the lead, while PVH offers a transformation-driven opportunity with longer-term potential. Supporting this stance, Ralph Lauren currently carries a Zacks Rank #2 (Buy), whereas PVH has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

#1 Semiconductor Stock to Buy (Not NVDA)

The incredible demand for data is fueling the market's next digital gold rush. As data centers continue to be built and constantly upgraded, the companies that provide the hardware for these behemoths will become the NVIDIAs of tomorrow.

One under-the-radar chipmaker is uniquely positioned to take advantage of the next growth stage of this market. It specializes in semiconductor products that titans like NVIDIA don't build. It's just beginning to enter the spotlight, which is exactly where you want to be.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Ralph Lauren Corporation (RL): Free Stock Analysis Report

PVH Corp. (PVH): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).