Quantum computing is quickly shifting from theory to real business. The global quantum market was about $2.70 billion in 2024 and is expected to grow to roughly $20.20 billion by 2030, with growth running near 41.8% a year from 2025 to 2030.

That kind of jump is coming from real use cases like drug discovery, complex financial modeling, supply chain planning, and cybersecurity, where traditional computers start to struggle. It also explains why so many companies now want a serious piece of this space.

More Yield, Less Trap: Sign up free to get Barchart’s daily Dividend Investor newsletter straight to your inbox.

Honeywell International (HON) moved up a gear in February 2026 when its quantum arm, Quantinuum, confidentially filed a draft registration statement for an IPO, putting years of work on track to be judged in public markets. The company has been getting ready for this, from flagging the plan to file to raising money through a senior notes offering tied to a planned Honeywell Aerospace spin, which should leave it more focused on higher-value tech businesses.

All of that leads to a straightforward question right now. With a quantum listing coming and the core business being reshaped, how should you play HON stock here? Let's find out

Honeywell’s Cash, Valuation, and Earnings

Honeywell is a big industrial and technology company that makes aerospace systems, building and factory automation tools, specialty materials, and safety and productivity gear. It is based in Charlotte, North Carolina, and runs operations across many regions.

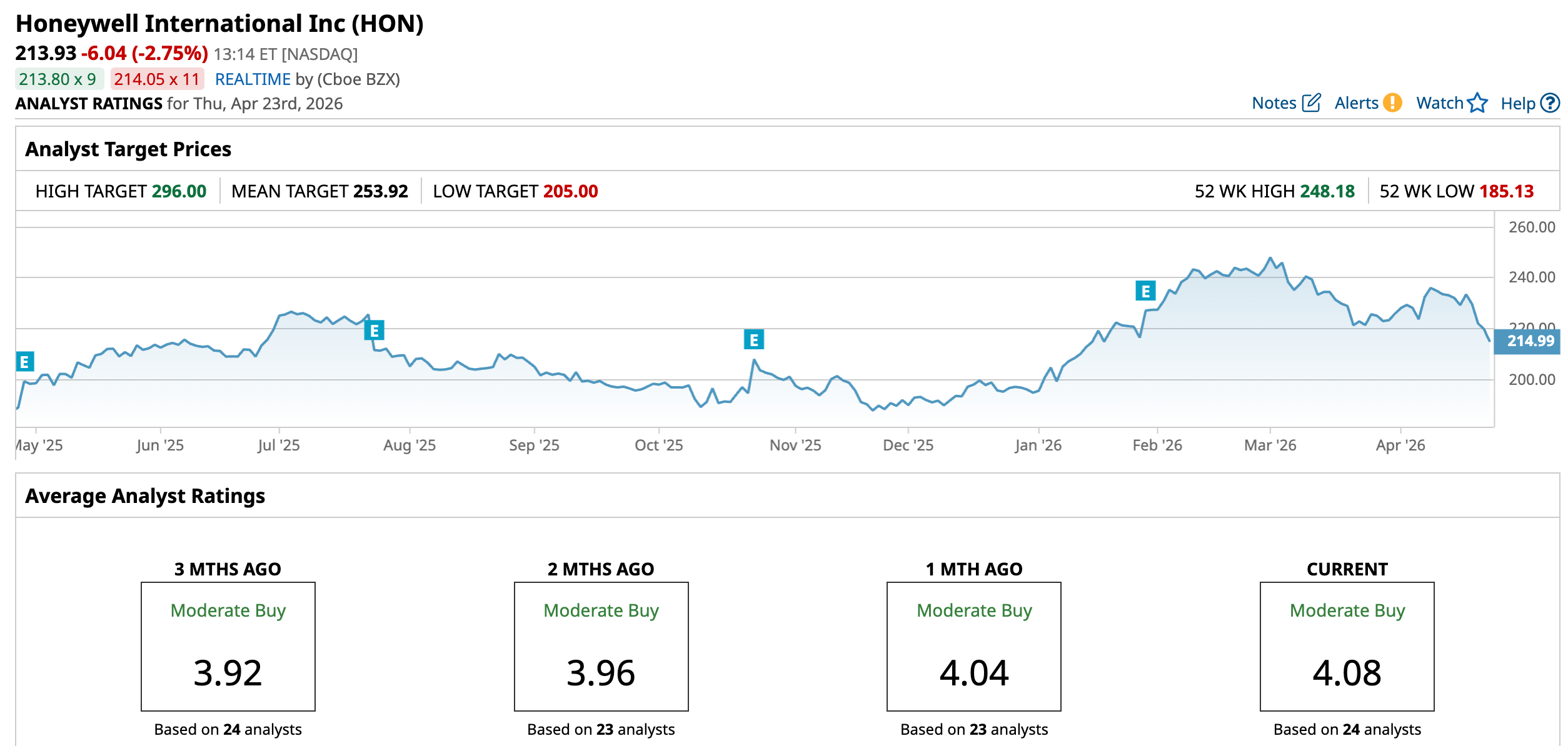

The stock's market capitalization is $139.4 billion, and the stock is up 9.5% so far this year and 14.77% over the past 12 months.

www.barchart.com

www.barchart.comHoneywell's shares trade at a premium of 20.83 times trailing earnings against a sector median of 22.20 times and a PEG ratio of 3.20 times compared with 1.76 times for peers. The company also pays a forward annual dividend of $4.76 per share, which works out to a 2.07% yield.

Honeywell’s fourth‑quarter 2025 update, released on January 30, showed EPS of $2.59 versus a $2.53 estimate, a 2.37% positive surprise. The same report showed $6.86 billion in sales for December 2025, down 34.09% from the prior quarter as portfolio changes and timing shifts pulled revenue lower. That quarter also included a net loss of $115 million and a 106.30% drop in net income versus the previous quarter, driven by restructuring charges and other one‑off items.

Honeywell still brought in $6.41 billion in operating cash flow in December 2025, up 23.14% from the prior quarter, which shows cash generation holding up better than reported earnings. This also translated into net cash flow, which came in at $1.92 billion, down 18.75% quarter-over-quarter (QOQ) as more cash went toward dividends, buybacks, investments, and balance‑sheet moves while management reshaped the business.

Honeywell’s Strategic Focus

Honeywell has been busy reshaping its business, and the latest deals show management making room for areas with better long‑term potential. The company agreed to sell its Productivity Solutions and Services unit to Brady Corporation in an all‑cash $1.4 billion deal, with closing expected in the second half of 2026, as part of a push to simplify operations and refocus the portfolio.

The defense side is getting stronger, too. Honeywell Aerospace signed an agreement with the U.S. Department of Defense to speed up production of key defense technologies, which helps support demand over several years in a segment where budgets and margins are usually more stable. That kind of steady, government‑backed revenue makes it easier to take Quantinuum’s early‑stage quantum story seriously.

Other moves point the same way. Honeywell amended its deal to buy Johnson Matthey’s Catalyst Technologies business, adding more exposure to process technologies and cleaner fuels, which tie directly into the energy transition trend.

Also, the company settled with Flexjet and renewed a long‑term contract through 2035, keeping an important business‑aviation customer using Honeywell avionics and services for years. On the tech side, Honeywell rolled out in‑store personalization tools built with Google Cloud that use computer vision and data to help retailers better understand shoppers and lift sales.

Wall Street Leans Into Honeywell’s Quantum Angle

Analysts are going into Honeywell’s next update with expectations set fairly low. The company is due to report on April 23 before the market opens, and the current estimate for Q1 2026 is $2.31 per share, down from $2.51 a year earlier. That points to a projected earnings drop of about 7.97%, which makes clear that short‑term profit growth is not really the main attraction in the HON story right now.

That softer trend has not stopped price targets from moving up. Jefferies, a major Wall Street investment bank and research firm, recently raised its target on Honeywell to $240. They cite steady execution and a cleaner portfolio that should be easier to back as Quantinuum works toward a public debut.

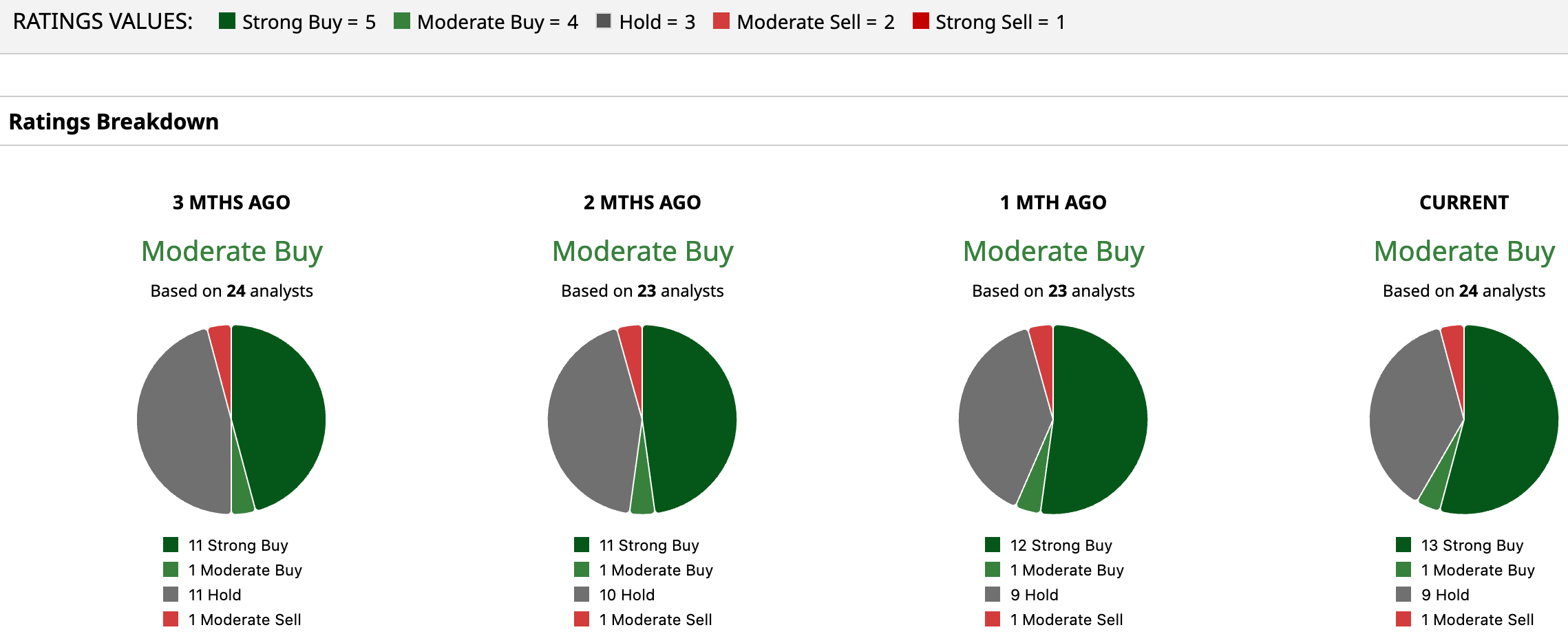

The wider group of analysts is on a similar page, as 24 analysts collectively rate HON at a “Moderate Buy,” even though not all of them are outright bullish on the stock. Their average target sits at $253.92, which works out to 18.7% upside from the recent price.

www.barchart.com

www.barchart.com www.barchart.com

www.barchart.comConclusion

Honeywell looks like a calm way to tap into the quantum theme without taking on the risk of a tiny, unproven name. The main business still generates solid cash, and the dividend helps while the story plays out. Quantinuum’s IPO simply adds extra upside on top, instead of being a do‑or‑die moment. Based on the recent setup and where targets sit, the share price seems more likely to drift higher over time than to break sharply lower, especially if better entry points appear on pullbacks.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Honeywell Just Announced That Its Quantinuum Unit Filed for an IPO. How Should You Play HON Stock Here? UnitedHealth Is Back! But Should You 'Long-Term Care' About UNH Stock? Capital Group Is Doubling Down on MicroStrategy. Should You Buy MSTR Stock Here Too? Broadcom Stock Is Trading at New All-Time Highs. Should You Buy Shares Here?