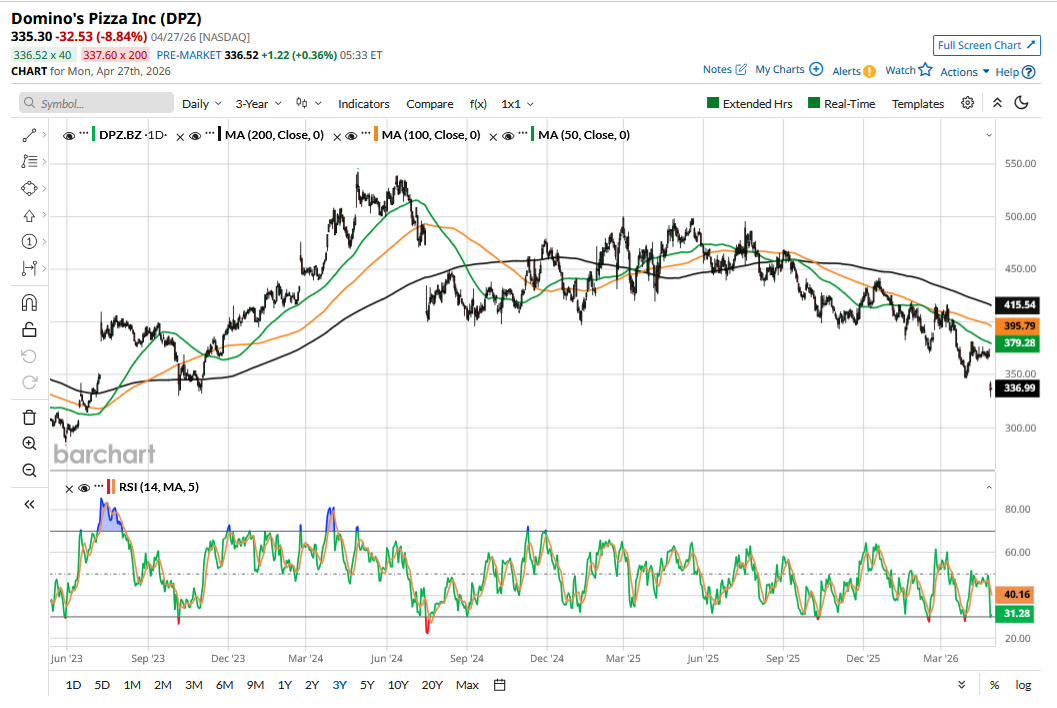

Domino’s Pizza (DPZ), which counts Berkshire Hathaway (BRK.B) (BRK.A) as its biggest investor after Vanguard, fell nearly 9% yesterday, April 27, as markets gave a thumbs-down to its Q1 2026 earnings. The stock has now extended its year-to-date (YTD) decline to nearly 20%, while the drawdown from 52-week highs is over 31%.

While we don’t know the exact price at which Berkshire bought DPZ, Barron’s estimates the number to be between $400 and $450 per share. Even going by the low end of that range, Berkshire is losing money on that investment, which was disclosed in Q3 2024 13F. Back then, I had noted that given the small size of that investment, it was unlikely that Buffett—who has since quit as the conglomerate’s CEO, handing over the baton to Greg Abel—had made the investment. I also argued that Domino’s and Pool Corp. (POOL), which was another new investment Berkshire disclosed in the quarter, did not appear to be good investments to me.

More Yield, Less Trap: Sign up free to get Barchart’s daily Dividend Investor newsletter straight to your inbox.

Both stocks are down significantly from the levels at which Berkshire bought the stake. While the conglomerate seemed to have done some bottom fishing in both these stocks back then, they have continued to underperform despite the brief bump following the announcement of Berkshire taking a stake.

www.barchart.com

www.barchart.com Domino’s Pizza Is a Dividend Powerhouse

Meanwhile, Domino’s Pizza is a dividend powerhouse. While the dividend yield of around 2.4% might not look too enticing, the payouts have increased at an annualized rate of nearly 20% over the last ten years, including a 15% increase for this year. The company generates healthy free cash flows, which totaled $671 million in 2025, a trailing free cash yield of over 5.2%. Along with dividends, Domino’s has also been spending cash on share repurchases as well as deleveraging its balance sheet.

The Pizza Industry Is Facing Several Challenges

The pizza industry is battling several headwinds and has become increasingly crowded. While quick delivery used to be Domino’s USP, that competitive advantage has been greatly eroded with the advent of delivery apps like Uber Eats (UBER) and DoorDash (DASH), which let smaller restaurants also offer deliveries to customers. There is also a pizza price war in the U.S., and Domino’s key U.S. competitors, namely Pizza Hut and Papa John's (PZZA), have been offering promotions to match its pricing.

Moreover, consumer habits are changing, and pizza restaurants, which were once second in sales in the U.S., dropped to sixth in 2024. The woes are reflected in the same-store sales. Domino’s Pizza reported a 0.9% year-over-year (YoY) growth in the metric in Q1, which was less than half of what the Street expected. The company also lowered its U.S. same-store sales forecast from 3% growth to low-single-digit growth. It expects its competitors to report a decline in their Q1 same-store sales when they report their earnings.

Incidentally, Pizza Hut’s parent company, Yum! Brands (YUM) is exploring strategic alternatives, which include an outright sale, while Papa John's is reportedly weighing a $1.5 billion offer from Qatari royal family-backed Irth Capital Management. Domino’s expects Papa John's and Pizza Hut to shut some of their stores if they are sold, which I believe is a fair assumption, as usually the new buyer takes such actions to cut costs.

DPZ Stock Forecast

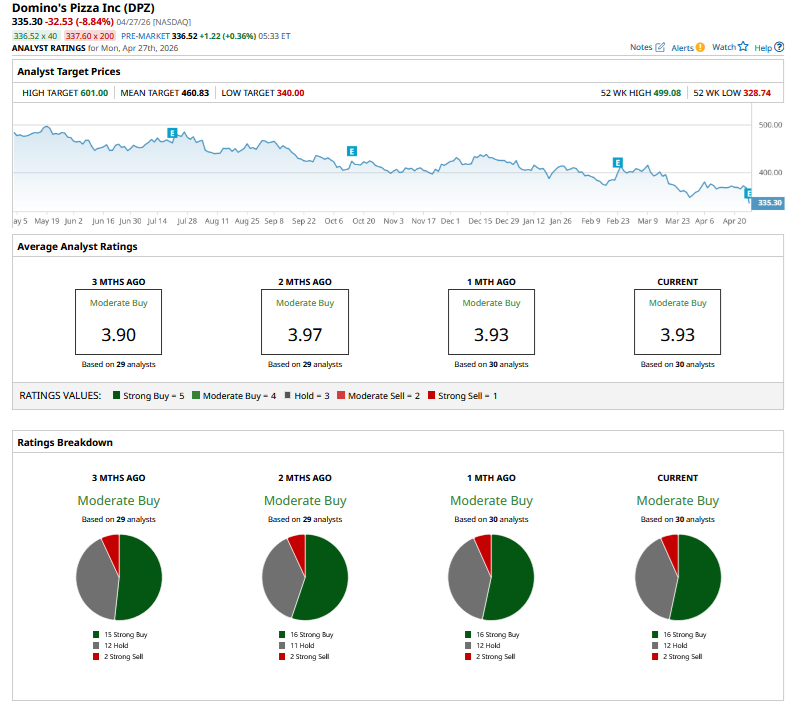

After DPZ’s Q1 earnings release, Baird and Stifel lowered the stock’s target price to $400 from $495 and $485, respectively. Barclays analyst Jeffrey Bernstein, who has an “Underweight” rating on the stock, lowered his price target from $370 to $316.

Of the 30 analysts covering Domino’s Pizza, 16 rate it as a consensus “Strong Buy,” while 12 analysts rate the leading pizza chain as a “Hold.” Two analysts rate the stock as a “Strong Sell.” DPZ’s mean consensus target price of $460.83 is 38% higher than current price levels. Notably, analysts have gradually been lowering Domino’s target price, and more downward adjustments could be on the way as brokerages reset their target prices following the Q1 earnings.

www.barchart.com

www.barchart.com Should You Buy Domino’s Pizza Stock?

While Domino’s Pizza has a healthy dividend yield and the payouts have risen at a good pace, we also need to look at the stock’s forecast. Domino’s trades at a forward price-to-earnings (P/E) multiple of just under 19x. The multiples have corrected over the last two years, as while the company’s profits have risen, its stock price has fallen.

While the multiples are not as exorbitant as they were in late 2024 when I covered the stock, they aren’t mouthwateringly cheap either. I find the risk-reward much more balanced now at these levels, but I won’t buy the stock yet, as valuations still don’t leave much margin of safety given the structural headwinds the pizza industry is facing.

On the date of publication, Mohit Oberoi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Warren Buffett’s Berkshire Hathaway Is Losing Money in This Dividend Stock: Can It Work for You? As Trump Renews Calls for Jimmy Kimmel's Removal, What's Next for Disney Stock? As Elon Musk Backs the Intel 14A Tech for His Terafab, Should You Buy INTC Stock? Nestlé Stock Jumped Despite Weak Sales. Here’s Why.