Hewlett Packard Enterprise (HPE) is a global edge-to-cloud leader that has pivoted from legacy hardware to high-value artificial intelligence (AI) and networking infrastructure. Formed from the 2015 split of Hewlett-Packard, the company today focuses on three strategic pillars: Networking, Cloud, and AI. Its GreenLake platform provides "everything-as-a-service" (EaaS), shifting the company toward recurring revenue while its specialized liquid-cooled AI factories power the world’s most demanding large language model (LLM) training clusters.

HPE stock recently received a new Street-high price target from Bank of America, but does that make it a buy? Let's take a closer look.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

About HP Enterprise Stock

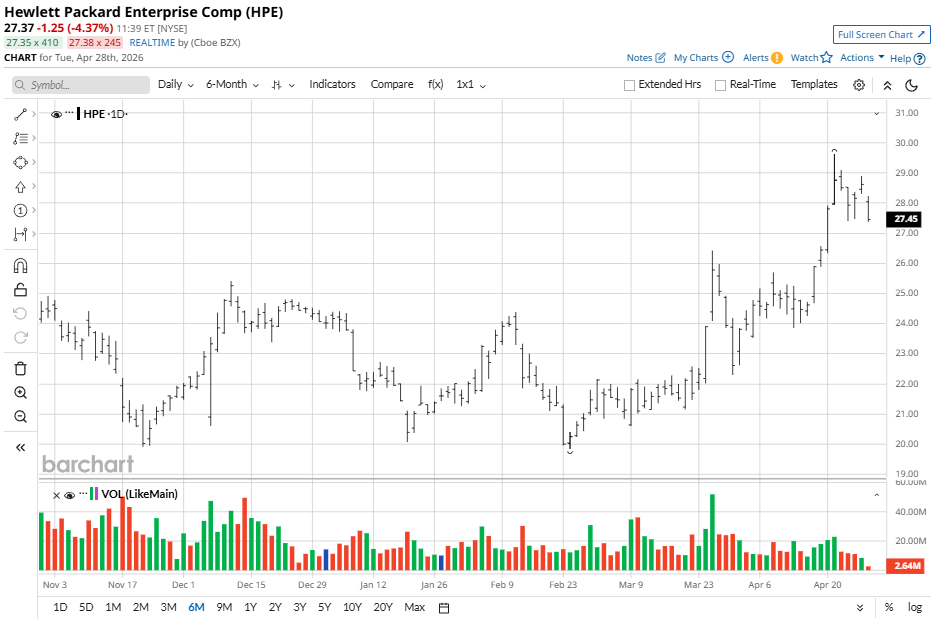

HP Enterprise stock has seen impressive momentum recently, hitting an all-time high of $29.63 earlier this month. The stock has surged roughly 73% over the last 12 months. This rally reflects investor confidence in the successful integration of Juniper Networks and HP Enterprise’s rising role as a "picks and shovels" play for AI infrastructure.

In comparison to the S&P 500 Information Technology Index ($SRIT), HPE has delivered significant outperformance over the past year. While the broader tech index has grown by approximately 50%, HPE stock’s 73% return has captured a massive performance gap as the market rewards the firm's transition toward high-margin networking and specialized AI servers. While it lacks the sheer scale of some "Magnificent Seven" peers, the company's focused leadership in liquid-cooling and "Sovereign AI" has allowed it to outpace the sector's average during the current AI infrastructure buildout phase.

www.barchart.com

www.barchart.com HP Enterprise's Financial Results

HP Enterprise reported strong results for the first quarter of fiscal 2026, posting revenue of $9.3 billion, an 18% increase year-over-year (YOY). The company achieved non-GAAP EPS of $0.65, handily beating the analyst consensus of $0.59.

A primary driver was the Networking segment, which grew 152% to $2.7 billion following the Juniper acquisition, now contributing over half of the company's total operating profits. Gross margins also saw a significant boost, reaching 36.6% on a non-GAAP basis. This profitability surge was supported by a record $5 billion backlog in AI systems and an increase in Wi-Fi 7 access point orders, signaling robust enterprise demand for modernized networking.

Looking ahead to Q2 2026, HP Enterprise estimates revenue between $9.6 billion and $10 billion, with a non-GAAP EPS range of $0.51 to $0.55. For the full fiscal year, management has raised its outlook, now projecting non-GAAP EPS of $2.30 to $2.50. CEO Antonio Neri highlighted that the "AI Factory" order target has been raised to nearly $1.9 billion by year-end.

Despite industry-wide supply-chain pressures in DRAM and NAND, HPE is leveraging agile pricing and multi-year supply agreements to protect margins. With $1.2 billion in operating cash flow, the company remains committed to returning capital, recently declaring a $0.1425 dividend payable in April 2026.

Bank of America Just Raised Its Price Target

Bank of America recently raised its price target on HPE stock to $38 from $32 — reflecting 34% potential upside from current levels — while maintaining a “Buy” rating as it identifies "agentic AI" as a significant new driver for infrastructure. Unlike simple, one-off queries, agentic AI involves complex, multi-step workflows that turn discrete inferencing into persistent, sequenced tasks. This evolution requires more CPU-intensive hardware and robust storage access, directly benefiting HPE’s traditional server business alongside its high-performance AI offerings.

Analysts led by Wamsi Mohan view HP Enterprise as a premium AI server OEM, particularly well-positioned to gain market share as these sophisticated workloads become the industry standard. While HPE is strategically integrating Juniper Networks to lead in networking, it remains a critical player in the server space.

BofA estimates that HPE will generate approximately $6.5 billion in AI server revenue during 2026. By focusing on higher-margin orders and specialized "AI Factory" solutions, the company is set to capture a larger portion of the projected $496 billion total AI server market.

Should You Buy HPE Stock?

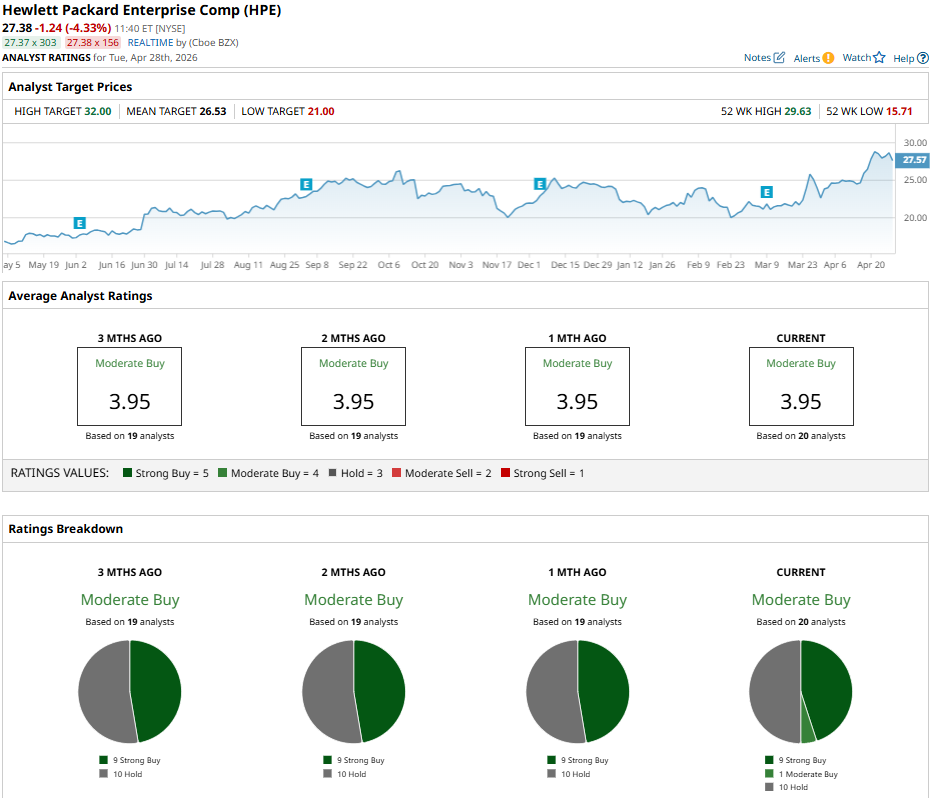

The recent price target upgrade from Bank of America has bolstered HPE stock’s standing as a high-growth value play. Shares currently hold a consensus "Moderate Buy" rating with a mean price target of $26.88, reflecting 5% potential downside from current levels. Professional sentiment is increasingly positive, with nine “Strong Buy” ratings, one “Moderate Buy,” and 10 “Hold” ratings out of 20 analysts with coverage.

With a forward price-to-earnings (P/E) ratio around 14.6 times, analysts suggest that the market has not yet fully priced in the long-term margin benefits of the Juniper acquisition or HPE’s expanding backlog. That makes it an attractive entry point for investors betting on the second wave of the AI buildout.

www.barchart.com

www.barchart.com On the date of publication, Ruchi Gupta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Intel Just Lost Its Chief Accounting Officer. Is That a Red Flag or a Nonissue for INTC Stock? Bank of America Just Gave HP Enterprise Stock a New Street-High Price Target As Super Micro Computer Expands Its Data Center Offerings, Should You Buy, Sell, or Hold SMCI Stock? Dan Ives’ Latest AI ETF Goes Beyond the Mag 7, Focusing on the ‘Circulatory System’ of a Tech Revolution