Fabrinet FN is set to report its third-quarter fiscal 2026 results in May. 4.

For the to-be-reported quarter, Fabrinet expects revenues between $1.15 billion and $1.2 billion, suggesting roughly 35% year-over-year growth at the midpoint. FN expects non-GAAP earnings in the $3.45-$3.60 per share range.

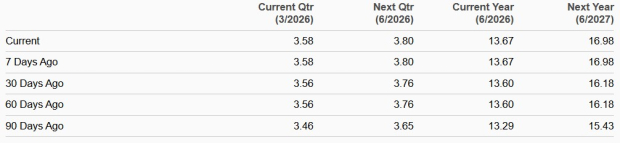

The Zacks Consensus Estimate for revenues is pegged at $1.2 billion, indicating an increase of 37.1% from the year-ago quarter’s reported figure. The consensus mark for earnings is pegged at $3.58 per share, up a couple of cents over the past 30 days, indicating an increase of 42.1% from the year-ago-quarter’s reported figure.

Consensus Estimate Trend

Image Source: Zacks Investment Research

FN’s earnings have surpassed the Zacks Consensus Estimate in each of the trailing four quarters, with the average surprise being 2.16%.

Fabrinet Price and EPS Surprise

Fabrinet price-eps-surprise | Fabrinet Quote

Let us see how things have shaped up for the upcoming announcement.

Key Factors to Note Ahead of FN’s Q3 Results

Sluggish growth in the automotive end-market is expected to have hurt Fabrinet’s top-line growth in the third quarter of fiscal 2026. The company has expected revenues to grow sequentially in telecom, datacom and high-performance computing (HPC). Unfavorable forex is expected to hurt FN’s results.

Fabrinet’s fiscal Q3 results are expected to have been driven by continued strong growth in non-optical communications, led by HPC, as customer demand scales and automated production capacity expands further. The company’s HPC segment has emerged as a key driver, with revenues surging to $86 million in the second quarter of fiscal 2026 from $15 million in the prior quarter, reflecting rapid hyperscale investments in AI data centers. Management indicated that this HPC program is slightly more than halfway through its ramp and is expected to exceed $150 million in revenues over the next couple of quarters, supported by additional automated production lines.

However, automotive revenues are expected to have experienced a modest sequential decline, reflecting predictable program timing rather than weakening demand, and acting as a slight offset to overall growth. Industrial laser revenues are expected to have remained stable with steady year over year and sequential growth, supported by consistent demand conditions.

Overall, the company’s ongoing diversification beyond optical communications, with strong contributions from automotive, industrial lasers and especially high-performance computing, is expected to have remained a key factor supporting fiscal Q3 performance.

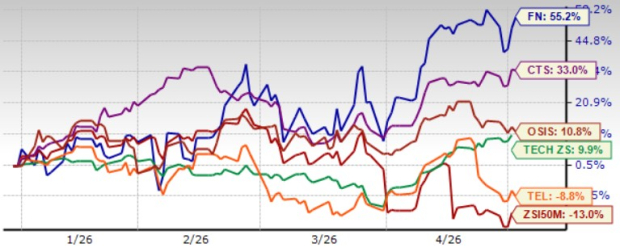

FN Shares Outperform Sector & Peers

Fabrinet shares have jumped a whopping 55.2% year to date, outperforming the Zacks Electronics Miscellaneous Components industry’s decline of 13% and the broader Zacks Computer and Technology sector’s appreciation of 9.9%. The company has outperformed peers, including TE Connectivity TEL, CTS CTS and OSI Systems OSIS in the year-to-date period. Shares of TE Connectivity have lost 8.8%, while CTS and OSI Systems have returned 33% and 10.8%, respectively, over the same time frame.

FN Stock’s Price Performance

Image Source: Zacks Investment Research

The FN stock is not so cheap, as suggested by the Value Score of F. In terms of the forward 12-month price-to-sales (P/S), FN is trading at 4.64X, higher than the industry and peers. While the industry is trading at 3.98X, TE Connectivity, CTS and OSI Systems trade at 2.98X, 2.84X, and 2.42X, respectively.

FN Stock is Trading at a Premium

Image Source: Zacks Investment Research

FN's Prospects Ride on Strong AI Demand

Fabrinet’s prospects are firmly anchored in accelerating AI-driven infrastructure demand, which is fueling strong growth across its business. Beyond HPC, AI demand is strengthening Fabrinet’s telecom and datacom businesses, particularly in data center interconnect modules, where demand remains robust and tied to AI workload expansion.

Fabrinet is expanding capacity, including its Building 10 facility and Pinehurst campus, to meet rising demand. Importantly, its HPC opportunity is not limited to a single customer, as it continues to pursue additional hyperscale clients and new AI-related technologies like co-packaged optics. These factors collectively position Fabrinet to benefit from long-term AI infrastructure spending.

Conclusion

Fabrinet’s growing AI infrastructure footprint, thanks to a strong component product portfolio, bodes well for its near-term prospects and justifies a premium valuation.

Fabrinet currently sports a Zacks Rank #1 (Strong Buy), which implies that investors should start accumulating the stock ahead of fiscal Q3 earnings. You can see the complete list of today’s Zacks #1 Rank stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. Little-known AI firms tackling the world's biggest problems may be more lucrative in the coming months and years.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

CTS Corporation (CTS): Free Stock Analysis Report

TE Connectivity Ltd. (TEL): Free Stock Analysis Report

OSI Systems, Inc. (OSIS): Free Stock Analysis Report

Fabrinet (FN): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).