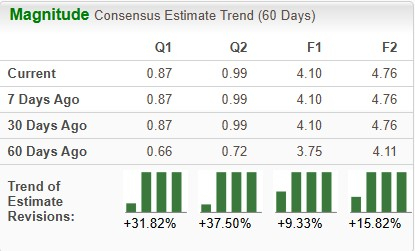

GigaCloud Technology GCT is slated to release first-quarter 2026 results on May 7, before market open. The Zacks Consensus Estimate for the to-be-reported quarter’s earnings and revenues is pegged at 87 cents per share and $344.9 million, respectively.

The earnings estimate for the to-be-reported quarter has increased 21 cents over the past 60 days. The Zacks Consensus Estimate for quarterly revenues indicates a 26.8% uptick from the year-ago quarter’s figure. The same for quarterly earnings indicates a 27.9% uptick from the year-ago quarter’s figure.

For 2026, the Zacks Consensus Estimate for GCT’s revenues is pegged at $1.51 billion, implying an expansion of 17.3% year over year. The consensus mark for 2026 EPS is pegged at $4.1, implying an increase of 14.2% on a year-over-year basis.

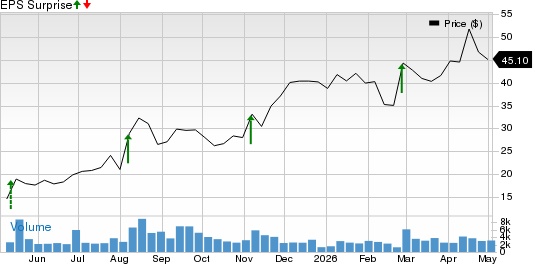

In the trailing four quarters, this company’s earnings surpassed estimates on each occasion. The average beat is 64.5%.

GigaCloud Technology Price and EPS Surprise

GigaCloud Technology Inc. price-eps-surprise | GigaCloud Technology Inc. Quote

Q1 Earnings Whispers for GCT

Our proven model does not predict an earnings beat for GCT for the March quarter. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. That is not the case here. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

GCT has an Earnings ESP of 0.00% and a Zacks Rank #1. You can see the complete list of today’s Zacks #1 Rank stocks here.

Factors Shaping GCT’s Q1 Results

GCT’s top-line performance for the first quarter of 2026 is expected to have been supported by higher segmental revenues from both services and products. The Zacks Consensus Estimate places service revenues at $120 million, reflecting 57.9% year-over-year growth, while product revenues are projected at $225 million, indicating a 26.4% increase from the same quarter last year. Strong revenue growth from international markets, particularly Europe, is also likely to have contributed to the overall top-line improvement.

Ongoing strategic optimization — integrating the product, channel and vendor resources of Noble House (acquired in 2023) with GigaCloud’s efficient and transformative marketplace — is also expected to have driven higher top-line volume during the quarter.

Moreover, the acquisition of New Classic Home Furnishings in January 2026 is anticipated to have expanded GCT’s distribution network and channel presence within the home furnishings market, helping diversify its operations beyond e-commerce and positively influencing revenues.

However, GCT’s efforts to manage rising product and service costs, while maintaining profit margins amid elevated tariffs and the tensions in the Middle East, are expected to have put pressure on its bottom line.

GCT’s Price Performance & Valuation

Shares of GigaCloud Technology have performed brilliantly over the past six months, gaining in double digits (% wise). Owing to this solid rally, shares of this company, which simplifies logistics for big and bulky merchandise, have easily outperformed the Zacks Technology Services industry’s 9.3% decline. GCT’s shares have also outperformed those of fellow industry players Dave Inc. DAVE and Symbotic SYM.

6-Month Price Comparison

From a valuation perspective, GCT is trading at a lower level compared with its industry. Based on its price-to-sales ratio, the company is trading at a forward earnings multiple of 1.07, below the industry’s 2.43. The company has a Value Score of A. GCT’s valuation is favorable compared with Dave and Symbotic as well. Dave and Symbotic currently have a Value Score of D each.

GCT’s P/S F12M vs. Industry, DAVE & SYM

How to Play GCT Pre-Q1 Earnings

Agreed that due to the nature of its operations, GigaCloud remains highly exposed to U.S.-China trade frictions and the possibility of higher tariffs. However, the company has a lot of factors working in its favor. This makes it well-positioned for continued success. The company’s strong, debt-free balance sheet, the unique business model, expansion efforts and attractive valuation are its major tailwinds.

GCT’s impressive earnings history, upbeat price performance and positive estimate revisions add to its appeal. In view of the positives, GCT appears to be a worthy buy ahead of its May 7 results.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Dave Inc. (DAVE): Free Stock Analysis Report

Symbotic Inc. (SYM): Free Stock Analysis Report

GigaCloud Technology Inc. (GCT): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).