Western Digital Corporation (WDC) has become the artificial intelligence (AI) storage trade everyone wishes they had bought earlier, sitting on triple digit gains over the past year with zero signs of cooling off. The data storage devices manufacturer sits right at the crossroads of the data center buildout, and that sweet spot is doing serious heavy lifting for the stock.

On April 30, the company walked into its latest earnings report, delivering strong sequential and year-over-year (YOY) revenue growth across every single end market while simultaneously expanding both gross and operating margins. Q3 fiscal year 2026 pushed gross margin clean past the 50% mark, proving that relentless innovation across a growing customer base is paying off beautifully.

More Yield, Less Trap: Sign up free to get Barchart’s daily Dividend Investor newsletter straight to your inbox.

The same confidence carried Western Digital straight into announcing a 20% bump in its quarterly cash dividend on April 30, landing shareholders at $0.15 per share, and the demand story behind that move practically tells itself.

Virtually every AI workload from training to inference to agentic and physical AI churns out data that needs a permanent and cost-efficient home on hard disk drives (HDDs), giving Western Digital a built-in growth engine that keeps institutional money flowing into the stock right where it matters most.

Now the real question is what stance the stock deserves going forward.

About Western Digital Stock

Headquartered in San Jose, California, Western Digital builds and sells data storage hardware and solutions rooted in HDD technology, catering to consumers, enterprises, and data centers alike.

Commanding a market cap of roughly $146.3 billion, its product lineup covers internal and external drives, portable storage, network attached storage (NAS) systems, and platforms, all moving through original equipment manufacturer (OEM) and channel distribution networks.

And if that weren't enough to keep the engineers busy, the company is pouring resources into quantum error correction to make next-generation computing far more dependable.

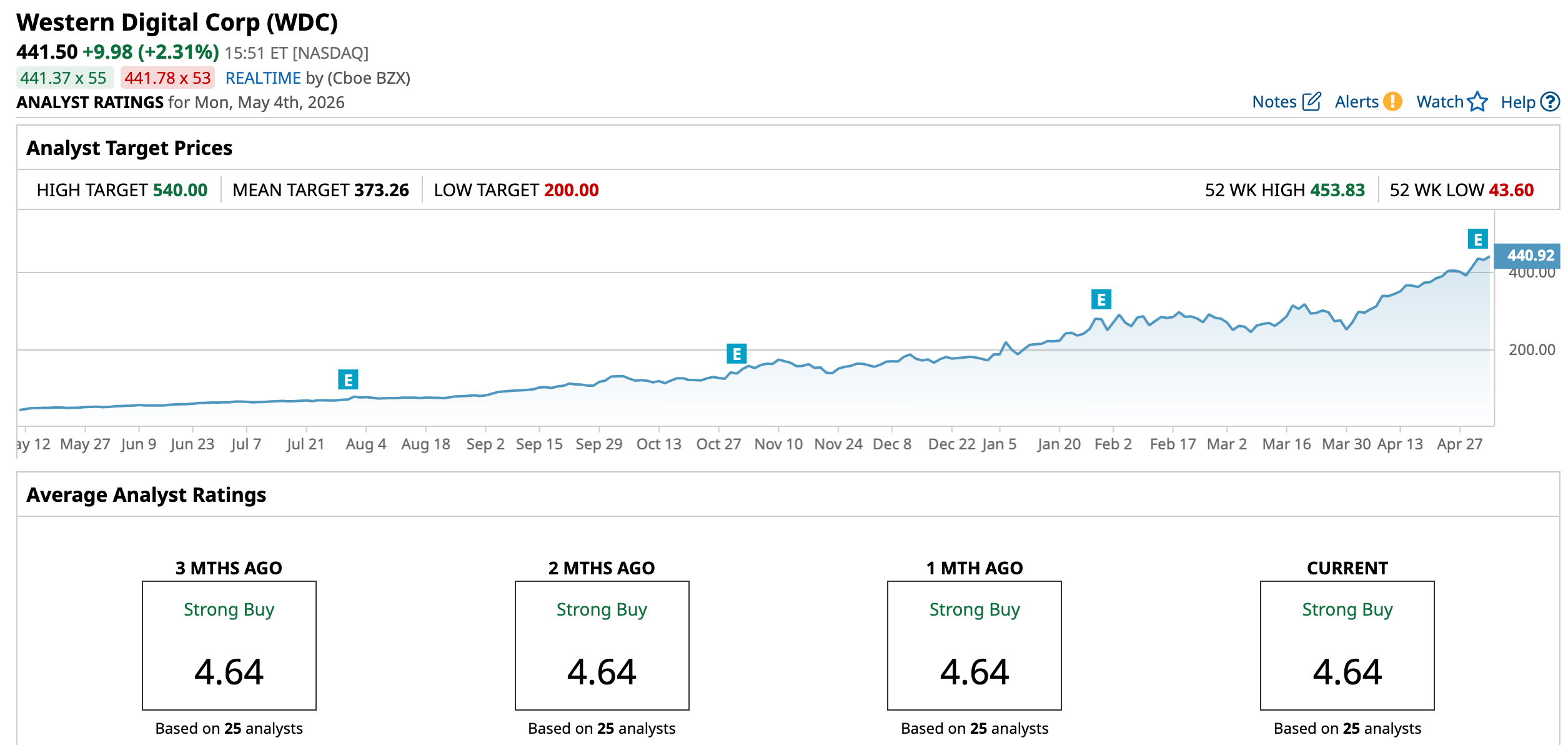

Now, the stock is where things really get cooking. Over the last 52 weeks, WDC stock has handed investors an 889.4% gain. 2026 alone kept that momentum alive, with the stock already up 156.7% year-to-date (YTD).

The last month tells an equally wild story, up 49.89%. In fact, on May 1, the stock hit a fresh 52-week high of $446.62, owing to Western Digital's blowout Q3 FY2026 earnings report, which dropped just a day earlier. Since then, the new high came on May 4 at $453.83.

www.barchart.com

www.barchart.com On the valuation front, WDC stock is currently trading at 50.45 times forward adjusted earnings and 11.38 times sales. Both figures sit well above the industry averages and the company's own five-year historical multiples, which tells you the market is paying a serious premium to own a piece of this story.

On the income front, Western Digital pays an annual dividend of $0.60 per share, translating to a yield of 0.14%. The most recent installment of $0.15 per share is scheduled to hit accounts on June 17, going to shareholders who are on the books as of June 5.

Western Digital Surpasses Q3 Earnings

On April 30, Western Digital's shares climbed 5.3% as Q3 fiscal year 2026 results cleared Wall Street's revenue and non-GAAP profit bars with room to spare. Revenue landed at $3.34 billion, a 45.5% jump YOY that beat analyst estimates of $3.26 billion. Non-GAAP EPS grew 97.1% from the year-ago value to $2.72, well ahead of the $2.39 the Street had penciled in.

Breaking the revenue down, Cloud carried the heaviest load at 89% of total revenue, pulling in $3 billion and growing 48% YOY on the back of strong demand for higher capacity nearline products and a friendlier pricing environment. Consumer chipped in 6% of revenue at $186 million, up 24% YOY, and Client added the remaining 5% at $179 million, up 31% YOY.

Non-GAAP gross margin expanded to 50.5% during the quarter, a gain of 1,040 basis points YOY, fueled by a continued mix shift toward higher-capacity drives, disciplined pricing execution, and tight cost control throughout the business.

All of that strength at the top rolled beautifully down the income statement, pushing non-GAAP operating income to $1.3 billion, a 115.9% jump YOY, with non-GAAP operating margin reaching 38.6%, up 1,260 basis points YOY.

Western Digital also did some serious heavy lifting on the balance sheet during the quarter, monetizing 5.8 million Sandisk Corporation (SNDK) shares and using the proceeds to slash debt by $3.1 billion. That left only $1.6 billion in convertible debt outstanding, and with $2 billion in cash and equivalents on hand, the company closed the quarter sitting in a net positive cash position of $450 million.

Looking ahead, management has guided fiscal 2026 Q4 revenue to $3.65 billion, plus or minus $100 million, which at the midpoint reflects 40% YOY growth. Gross margin is expected to land between 51% and 52%, and diluted EPS is projected at $3.25, plus or minus $0.15.

On the other hand, analysts are modeling Q4 fiscal year 2026 EPS at $2.51, reflecting 66.2% YOY growth and full year fiscal year 2026 earnings rising 91.6% from the prior year to $8.68. Fiscal year 2027 is anticipated to deliver yet another 57.6% surge to $13.68.

What Do Analysts Expect for Western Digital Stock?

Wall Street's finest have been sharpening their pencils on WDC stock. UBS bumped its price target to $375 from $350 and held its “Neutral” rating, while TD Cowen's Krish Sankar made a bolder move, lifting his price target all the way to $500 from $325 and standing by his “Buy” rating.

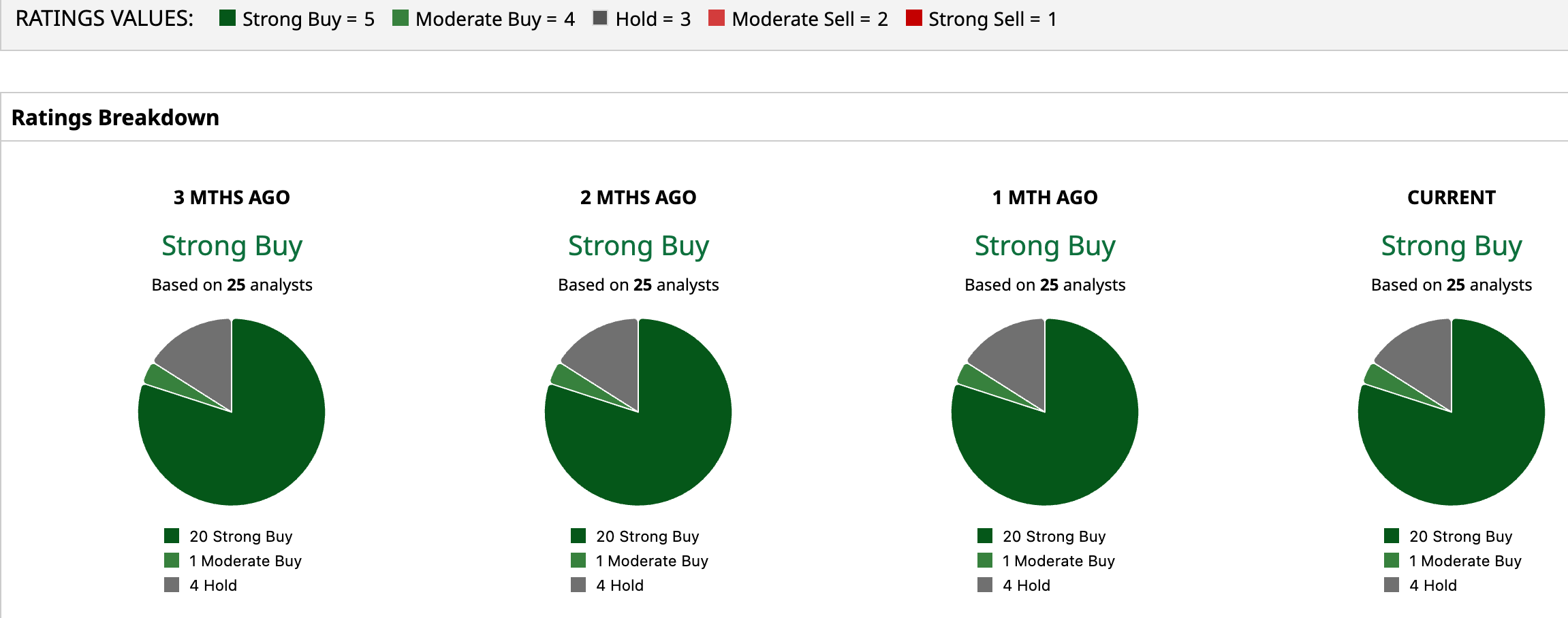

Wall Street as a whole has made up its mind on WDC stock, handing it a “Strong Buy” overall rating. Of the 25 analysts covering the stock, 20 firmly back it with a “Strong Buy,” one lands on “Moderate Buy,” and four sit on the fence with a “Hold.”

The stock has already lapped its average price target of $373.26, yet the Street-High target of $540 still leaves 22.3% upside sitting on the table from current levels. And then Cantor Fitzgerald walked in and raised the bar even further, moving its price target to $660 from $500 and maintaining an “Overweight” rating on the shares.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Dear Western Digital Stock Fans, Mark Your Calendars for June 5 CRM Stock Jumps as Salesforce Makes Clear It’s an AI Agent Company Now More AI Is Coming to iOS 27. Why That Could Make Apple Stock a Buy Here. Seagate and Western Digital Are a Hard Disk Drive Duopoly. Barchart Ranks the Storage Stocks Here.